by Darrell Spence, et al., Economist, Capital Group

KEY TAKEAWAYS

- AI and the Iran war are pulling the global economy in opposite directions.

- Wars have pushed oil prices higher, but stocks typically recovered quickly.

- Employment data may drive the Fed’s interest rate policy.

- U.S. midterm elections could bring more volatility and muted returns.

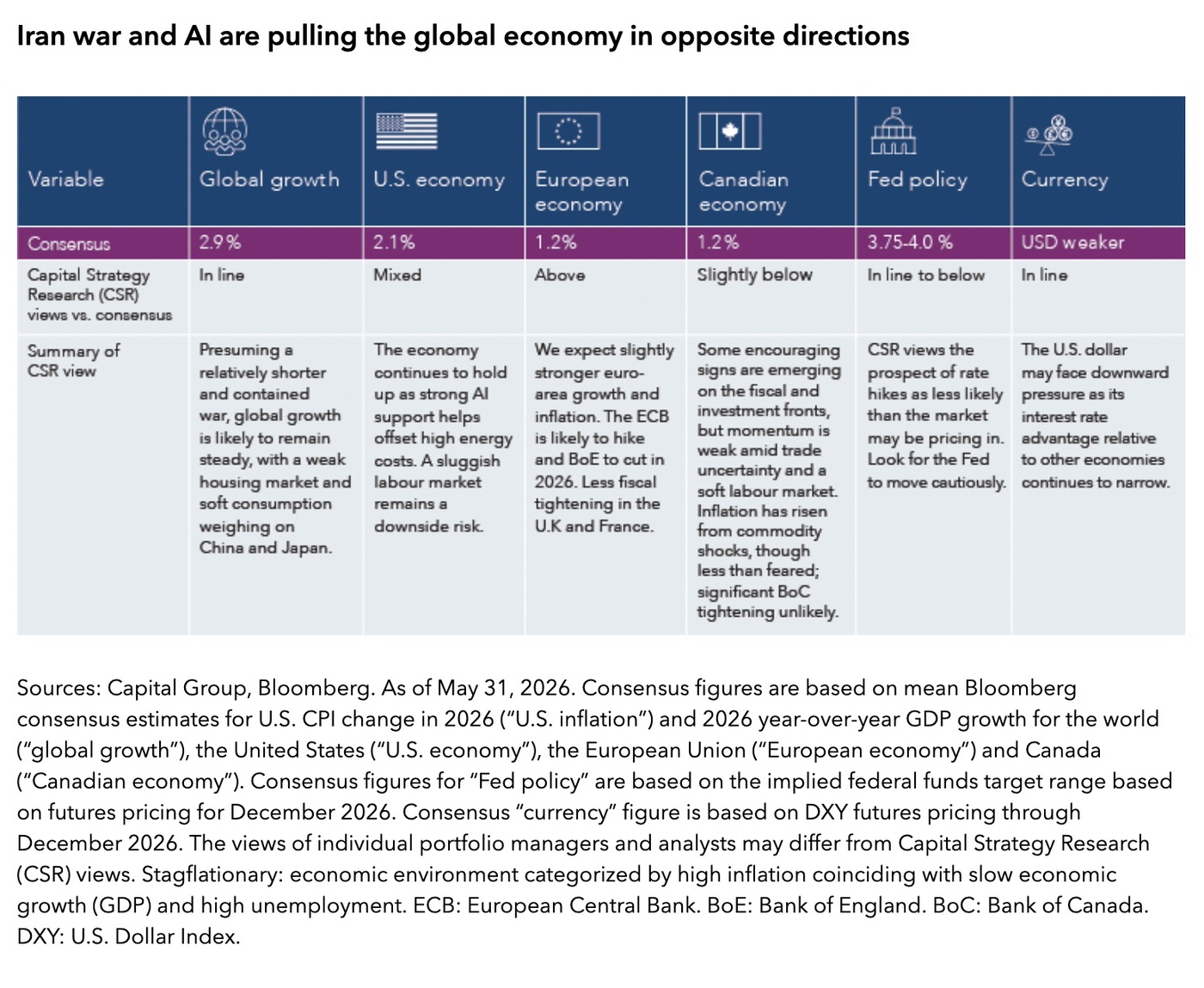

Global economic growth is coming under pressure due to the Iran war, rising oil prices and ongoing trade disputes, but one powerful engine is more than making up for it: AI-related investment spending.

The artificial intelligence boom is so massive that even if activity in all other sectors contracted, overall economic growth could remain in positive territory, especially in the United States, says Capital Group economist Darrell Spence.

“I remain on the cautious side when it comes to the outlook for U.S. growth,” Spence explains, “but it is still possible that GDP could be significantly higher than expected — in the range of 2.5% or more. That’s how much the AI arms race is contributing to overall economic growth.”

For the U.S. and the rest of the world, much depends on the duration and severity of the Iran war, mounting inflationary pressures, weakening consumer fundamentals, and whether the AI boom marches on or fizzles out.

“There is a tug of war between these global economic forces, and it could be a while before a clear winner emerges,” Spence adds. In the meantime, economic growth driven solely by one sub-sector of the economy may not necessarily be healthy growth.

Elsewhere, Europe is facing a stagflationary shock before year-end, as higher energy prices weigh on activity, according to Capital Group economist Beth Beckett. “I do expect a much smaller shock than we saw in 2022, thanks in part to stronger manufacturing activity and looser fiscal policy in Germany.” Higher defence spending in Europe has already provided a significant boost to the region’s aerospace and defence companies, and that is expected to continue as geopolitical conflicts increasingly shape the global landscape.

In Canada, CUSMA negotiations look like they may get messy, which should keep uncertainty high and deter capex/hiring in trade-sensitive sectors, according to Canada economist Tryggvi Gundmundsson. “Although there’s still debate as to whether the economy is officially in recession after the second-quarter GDP print, there is little doubt Canada is struggling to grow amid U.S. trade tensions,” he says.

In Asia, look for a weak housing market and slowing global trade to weigh on China’s economy while Japan remains sluggish as the conflict in the Middle East impairs export activity. Both countries are dealing with an energy crunch due to the Iran war. As long as the Strait of Hormuz remains closed or partially blocked, restricted oil supplies could further constrain economic growth, particularly once strategic reserves are depleted. Prior to the war, China was by far the largest buyer of Iranian oil.

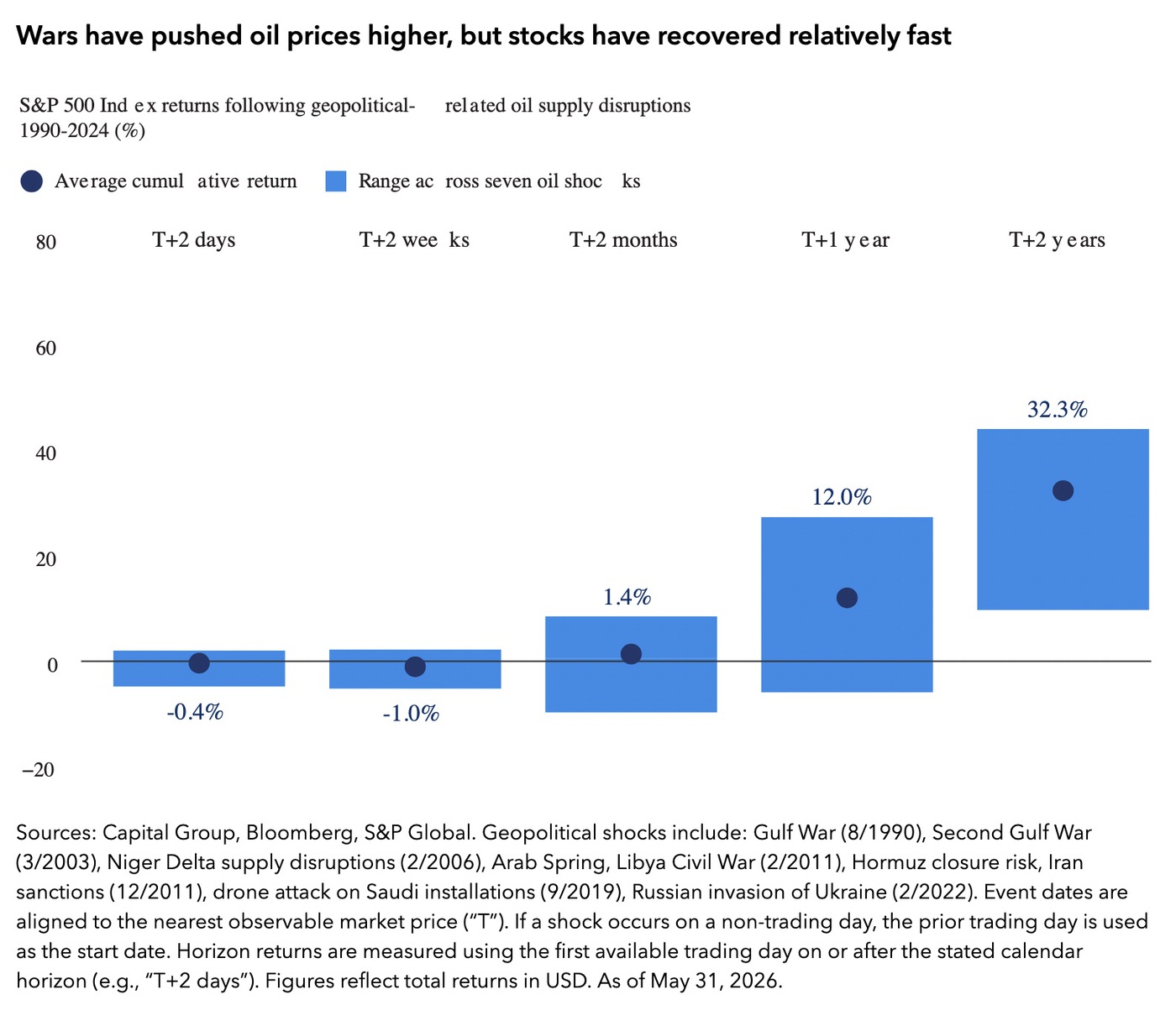

Oil shock is a risk, but we’ve been here before

The Iran war is a stark reminder that the world still runs on oil. When supply is threatened, the impact of higher oil prices spreads quickly to businesses, consumers and global markets.

About one-fifth of the world’s oil supply moves through the Strait of Hormuz, off the coast of Iran, so any disruption there is almost immediately reflected in fuel prices. Even in the United States, the world’s largest oil producer, the price of gasoline at the pump has jumped nearly 53% since the war started.

“There are very real economic risks, and the costs will only compound as the war drags on,” says equity portfolio manager Paul Benjamin. “A persistent conflict could trigger weaker equities, a stronger U.S. dollar and widening credit spreads.”

The good news is, over the past two decades, stock markets have generally bounced back from geopolitical shocks because they haven’t resulted in prolonged physical supply outages. Across seven oil supply shocks, from the First Gulf War in the 1990s to Russia’s invasion of Ukraine in 2022, U.S. equities fell by an average of 1% two weeks following the disruption, then rose 1.4% a month later, 12% a year later and 32.3% over the next two years. It’s a helpful reminder that markets are forward-looking and may already be anticipating a resolution to the present crisis.Interest rate outlook is murky at best

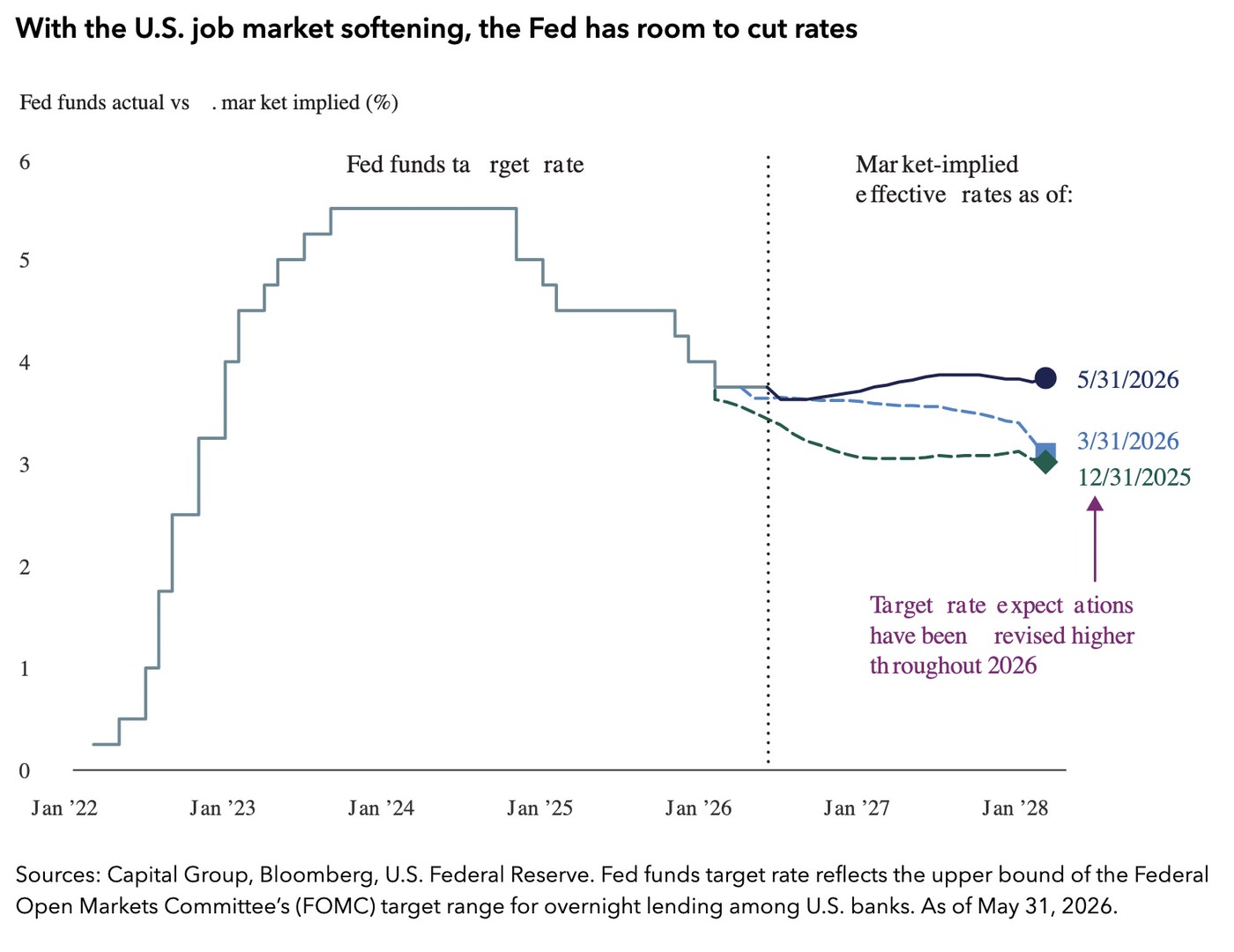

Interest rate outlook is murky at best

With key U.S. Federal Reserve (Fed) meetings on June 16 and 17, all eyes are on new Fed Chair Kevin Warsh for clues about the future direction of interest rates. President Trump has already weighed in, recently telling NBC’s Meet the Press, “There’s no reason to raise interest rates.” That comment followed a strong U.S. jobs report, which has fuelled speculation of a Fed rate hike before the end of the year.

Indeed, U.S. employment data may hold the key to the Fed’s next move, even as war-driven inflation intensifies. Fed officials have indicated in recent months that supporting the labour market may have to take precedence over the fight against inflation.

Inflation has moved sharply higher. The U.S. Consumer Price Index climbed 4.2% in May, the largest jump since April 2023. The increase was primarily driven by higher energy costs, which rose 23.5% compared to a year ago.

Labour markets are weaker than they were a few years ago, but remain steady overall, notes Capital Group fixed income manager Chitrang Purani. “The war is keeping inflation above the Fed’s 2% target and may weigh on non-AI business investment as well as consumer demand. That combination increases the risk of a more pronounced slowdown in growth.”

Purani believes policymakers will remain patient. “The labour market has been stable, with slower job growth offset by slower labour force expansion, but if this balance were to shift toward a rising U.S. unemployment rate the Fed will likely look past near-term inflation risks.”

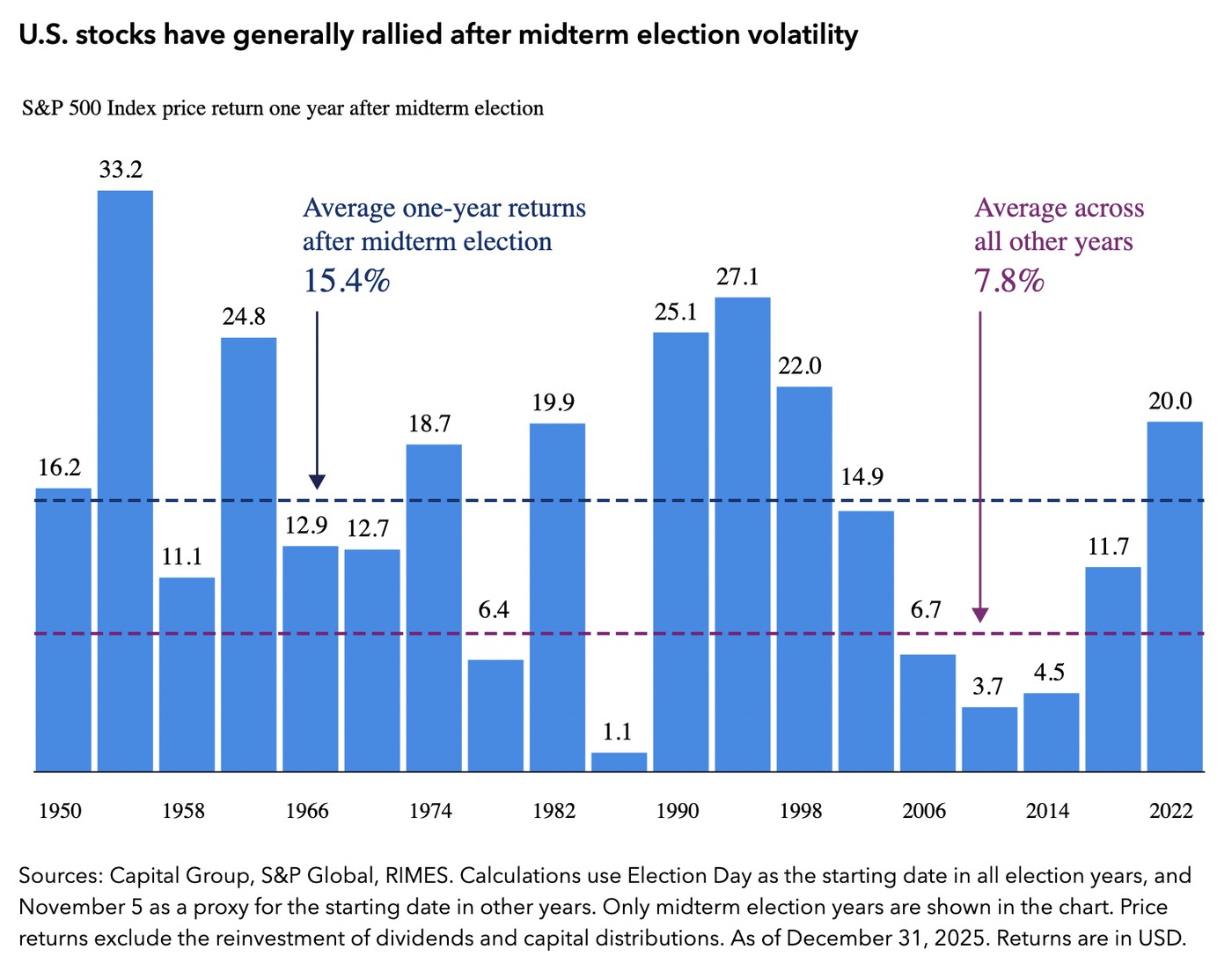

U.S. midterm elections: Volatility, then stocks have rallied

With everything else happening in the world, investors may not be focused on the U.S. midterm elections yet. But this pivotal contest is just a few months away, and it could have a noticeable effect on the stock market, if history is any guide.

To gauge the impact, Capital Group examined more than 90 years of S&P 500 Index data, and it turns out that stocks do exhibit some unique characteristics during midterm years. Market volatility tends to rise, returns tend to be muted and, once the outcome is known, stocks tend to rally.

So far the competing forces of rising corporate earnings, the Iran war and a powerful rally in AI stocks are driving market activity, but that could change as investors turn their attention to what is likely to be a rancorous election season.

The silver lining is that returns have tended to be strong during the full year following midterm elections, averaging 15.4% in U.S. dollar terms since 1950. Still, for long-term investors, these short-term moves don’t normally mean much. “There may be bumps in the road,” says Chris Buchbinder, portfolio manager for Capital Group U.S. Equity FundTM (Canada), “and investors should brace for short-term volatility, but I don’t expect election results to be a huge driver of investment outcomes one way or the other.”

Plus, at this point, it’s just too close to call.

“We all know that, historically speaking, the party in power tends to face setbacks in the midterms, and so history favours the Democrats,” says Capital Group political economist Matt Miller. “But remember, we are still far from election day. Five months is a lifetime in politics. I think we will see an enormous amount of energy and well-funded advertising campaigns that I think could make this election closer than folks expect. It might just give Republicans a chance to eke out what today would be considered a surprise win.”

*****

Darrell R. Spence is an economist with 33 years of investment industry experience (as of 12/31/2025). He holds a bachelor’s degree in economics from Occidental College. He also holds the Chartered Financial Analyst® designation and is a member of the National Association for Business Economics.

Beth Beckett is an economist with six years of investment industry experience (as of 12/31/2025). She holds a master's in economic history from the London School of Economics and Political Science and a bachelor’s in economics from Durham University.

Paul Benjamin is an equity portfolio manager with 20 years of investment industry experience (as of 12/31/2025). He holds an MBA from Stanford and a bachelor’s degree in finance and religion from Northwestern College.

Chitrang Purani is a fixed income portfolio manager with 22 years of investment industry experience (as of 12/31/2025). He holds an MBA from the University of Chicago and a bachelor's degree in finance from Northern Illinois University. He also holds the Chartered Financial Analyst® designation.

Christopher Buchbinder is an equity portfolio manager with 30 years of investment industry experience (as of 12/31/2025). He holds a bachelor’s degree in economics and international relations from Brown University.

Matt Miller is a political economist with 35 years of experience and has been with Capital for 10 years (as of 12/31/2025). He holds a law degree from Columbia and a bachelor's degree in economics from Brown University.

Tryggvi Gudmundsson is an economist with 17 years of investment industry experience (as of 12/31/2025). He holds a PhD from the London School of Economics and Political Science, and master’s and bachelor’s degrees in economics from the University of Iceland.

Copyright © Capital Group