by John Kerschner, CFA, Global Head of Securitised Products, Portfolio Manager, Janus Henderson

Early this year, markets were predicting the Federal Reserve would deliver two rate cuts in 2026 and that rates would not rise back to current levels until 2030. Following consistently strong employment and growth data, as well as an unwelcome spike in inflation due to higher energy prices, the market now anticipates a hike later in 2026, with rates likely continuing to rise thereafter. This is just the latest chapter in the post-ZIRP economy. We think investors should adapt to the new reality and consider assets such as AAA CLOs, which possess a compelling mix of strong credit quality, floating rate income, and price stability that has performed well as the interest rate regime has shifted.

Key takeaways

- In the six years since mid-2018, fixed income investors have had to contend with a markedly less-certain interest rate environment compared to the 10 years that succeeded the Global Financial Crisis, when the federal funds rate was firmly rooted to zero and talk of shifts in monetary policy was scarce.

- This post zero-interest-rate-policy (ZIRP) environment has required investors to pay closer attention to managing their exposure to rate volatility if they are to realize the diversification and volatility-reducing benefits of their fixed income allocation. And this new rate regime is likely to persist, with a low probability that we revert to the benign ZIRP environment, in our view.

- We believe the key to successfully navigating the new regime hangs on staying up in credit quality and being cautious on taking interest rate risk. More specifically, diversifying exposure to include floating-rate CLOs, which benefit from rate hikes (in contrast to fixed-rate bonds, which fall in value when rates rise) is essential, in our view.

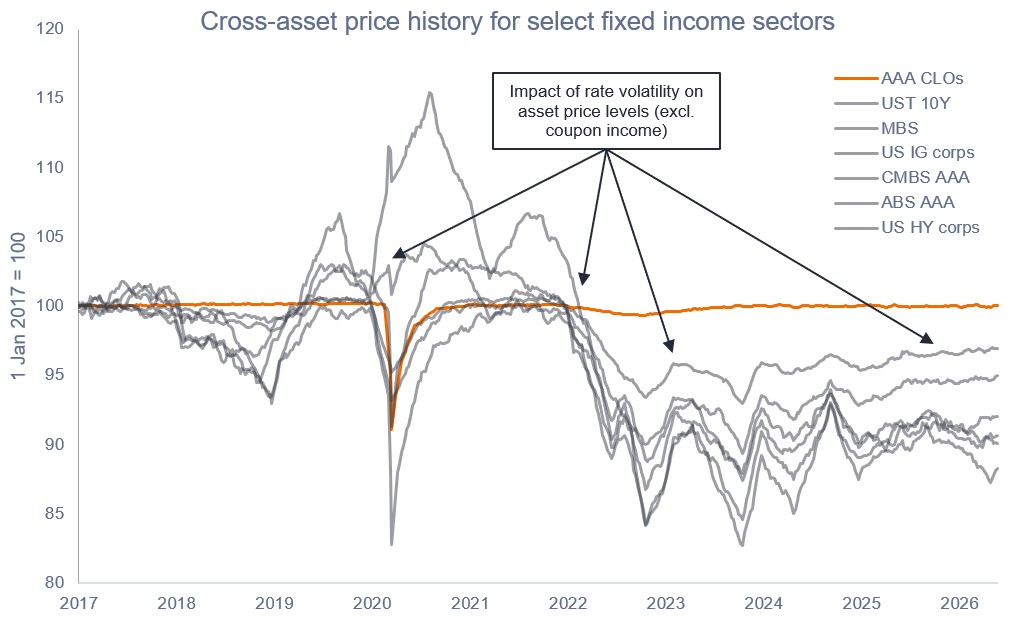

Amid significant shifts to rate expectations in 2026, most fixed income sectors have continued to exhibit price sensitivity and dispersion, yet AAA rated collateralized loan obligations (AAA CLOs) have remained tightly anchored near par.

We believe ongoing developments surrounding inflation, rates, and market volatility, coupled with geopolitical, fiscal, and monetary policy uncertainty, have highlighted how well-suited AAA CLOs are to navigating uncertain environments, as their low-duration, floating-rate structure may help provide stability and capital preservation amid persistent rate uncertainty. The chart shows cross-asset price history for select fixed income sectors and excludes the impact of coupon income.

Copyright © Janus Henderson