by Vaibhav Tandon, Senior Economist, Northern Trust

The Middle East war has entered a fragile ceasefire, offering tentative relief to energy and financial markets. Oil prices have eased and volatility has subsided, feeding hopes that the worst disruptions may be passing.

Yet even if peace were declared tomorrow, the global supply chain would not snap back to normal. Disruptions will linger for months, long after the headlines fade.

Oil extraction in the Middle East could resume relatively quickly, but shipping flows would be uneven and constrained. Tankers have moved out of the region, and these large, slow vessels will need weeks to navigate back. Higher insurance costs are set to linger.

Disruptions will linger beyond reopening.

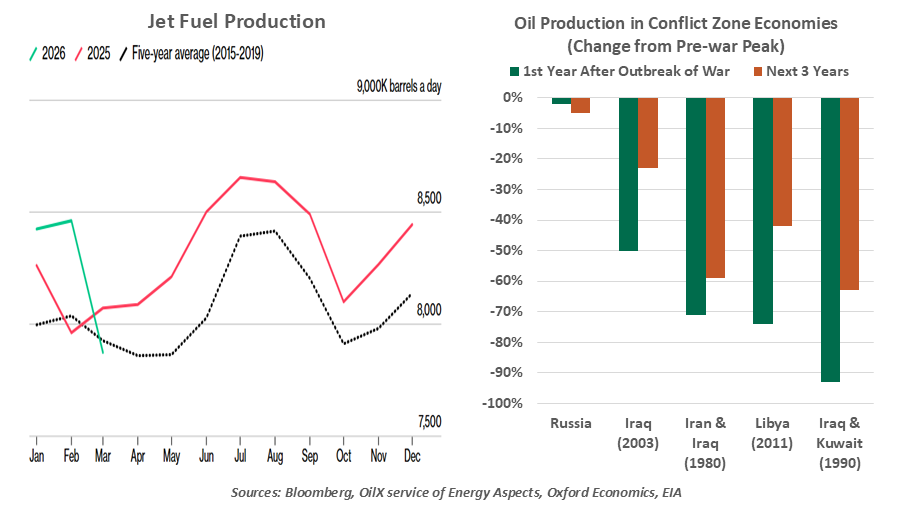

Downstream fuel markets will adjust far more slowly. Damage done to refineries for jet fuel will limit production; using alternative facilities is difficult because of strict specifications. In periods of scarcity, jet fuel is routinely deprioritized in favor of gasoline or diesel. With refinery repair timelines extending well beyond the normalization of shipping, aviation fuel supply and pricing are likely to remain dislocated.

Natural gas markets face similar headwinds. Damage to infrastructure in one of the world’s largest producing regions implies a recovery path to full production that is measured in years, not months.

The stress may not stop with energy. Disruptions to fertilizer shipments, stemming from constrained gas supply or persistent shipping bottlenecks, risk lingering spillovers into agriculture. Even short‑lived interruptions can reduce crop yields, create shortages and push up food prices. And as we have noted here, emerging shortages in critical inputs such as helium could strain industrial value chains.

Past conflicts point to a familiar pattern. In war-torn regions, crude production has often collapsed by close to 60% in the first year, with recovery stretching over several years and leaving a medium‑term shortfall of roughly 40%. The economic fallout extends well beyond the fighting, with Oxford Economics finding that over one‑fifth of an energy‑driven inflation surge typically persists up to three years.

The lesson is clear: reopening chokepoints restores flow, not balance. Markets may stabilize quickly, but the real economy adjusts far more slowly.

Copyright © Northern Trust