by Russ Koesterich, CFA, JD, Portfolio Manager, BlackRock

Key Takeaways

- While Russ acknowledges that the ongoing conflict in the Middle East has contributed near-term volatility, he also notes that these rising tensions are occurring against the backdrop of a solid U.S. economy.

- As tensions escalate overseas, it’s important to note that U.S. consumers are less sensitive to gasoline prices than they were 40 years ago and, as a country, the U.S. has shifted from a net importer of crude to a net exporter.

- Although both the intensity and length of the conflict remain uncertain, Russ maintains a baseline assumption of economic resilience, rather than recession or a bear market.

Stock markets, at least in the U.S., were already facing several challenges: an abrupt rotation out of technology, lingering inflation concerns and unresolved tariff uncertainty. Now add to the list a new war in the Middle East and an oil shock.

While the length and the extent of the conflict will determine the magnitude and duration of the oil shock, along with market volatility, there are four reasons to be optimistic: a so far manageable rise in the price of oil, shifts in U.S. spending, rising domestic production and economic momentum.

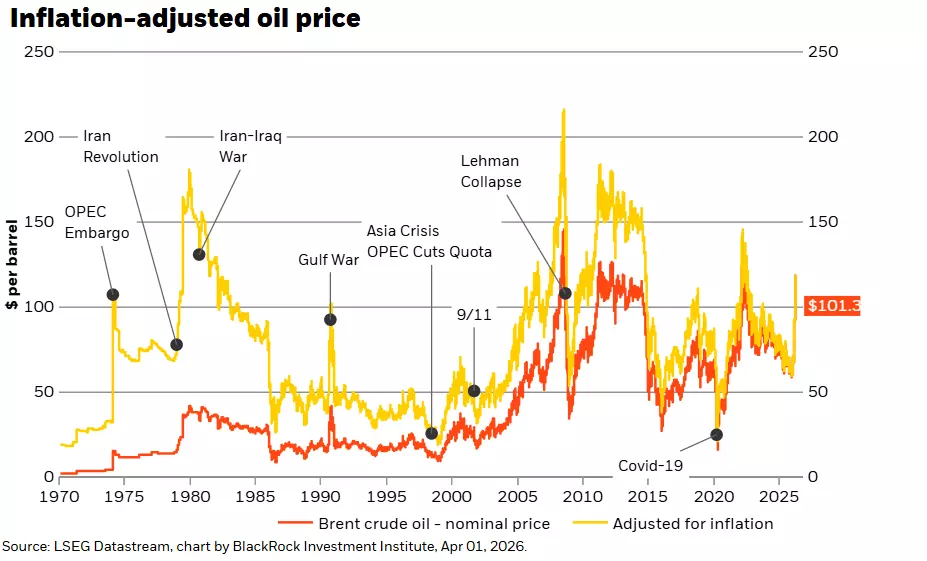

Going into the war, oil was well supplied. The average price of the U.S. benchmark West Texas Intermediate (WTI) was around $60/barrel in early January. While oil has risen significantly, it remains well below the levels reached in previous oil shocks, particularly when you adjust for inflation (see Chart 1).

Another factor favoring resilience: as a country, we spend less on energy. According to the Energy Information Administration (IEA), consumers spend less than 2% of disposable income on gasoline, the lowest share since 2005. Lower energy spending is consistent with the long-term trend. U.S. spending on gasoline and other energy has declined from around 6% in the early 1980's to less than 3% today.

When we do consume oil, much more is domestically produced. Domestic oil production is approximately 13.7m/bpd, near the recent peak of nearly 13.9m. Rising product has also translated into energy independence. United States net exports have swung from a deficit of roughly 9m/bpd in 2010 to a net export of roughly 3m/bpd last year.

Finally, oil shocks are most disruptive when occurring against a backdrop of a weak economy or one in which inflation is rising and financial conditions are tightening. Today we have a more stable economic backdrop. Manufacturing is recovering, capital spending is surging, the labor market appears to be stabilizing, productivity accelerating and consumption is still healthy. And while the Fed is on pause, financial conditions remain accommodative.

Does higher oil give tech a bid?

Should oil prices rise further on the back of a more intense and/or prolonged conflict, the economy and markets are certainly vulnerable.

Interestingly, while current events may not lead to a significant sell-off, they have the potential to instigate yet another shift in the investment narrative. While higher oil is unlikely to derail the economy, it may dampen it and slow what might otherwise be above trend growth. This may already be influencing investor preferences. Since the invasion, large cap growth has been performing better, at least on a relative basis, a development consistent with more muted economic expectations.