by AllianceBernstein Multi-Asset Research

Global treasury bonds were highly volatile in the first half of 2022, as inflation and interest rates rose sharply and bond markets tumbled along with stocks. Alongside this, we saw correlations between treasuries and equities increase, which meant that the diversification benefit of duration exposure declined. Given these dynamics, we felt it made sense then to reduce duration exposure within multi-asset strategies in favor of other diversifying building blocks.

Much has changed since then. Markets have priced in aggressively tighter US central bank policy, including the 75-basis-point Fed hike in late July. Moreover, treasury yields—though still close to their 12-year highs—have dipped in recent weeks, which we think reflects investors’ expectations of moderating inflation, and possibly an economic slowdown. Most major economies are now in contraction mode, according to the Organization for Economic Cooperation and Development, and new signs suggest that inflation is easing in key areas like commodities, energy and durable goods.

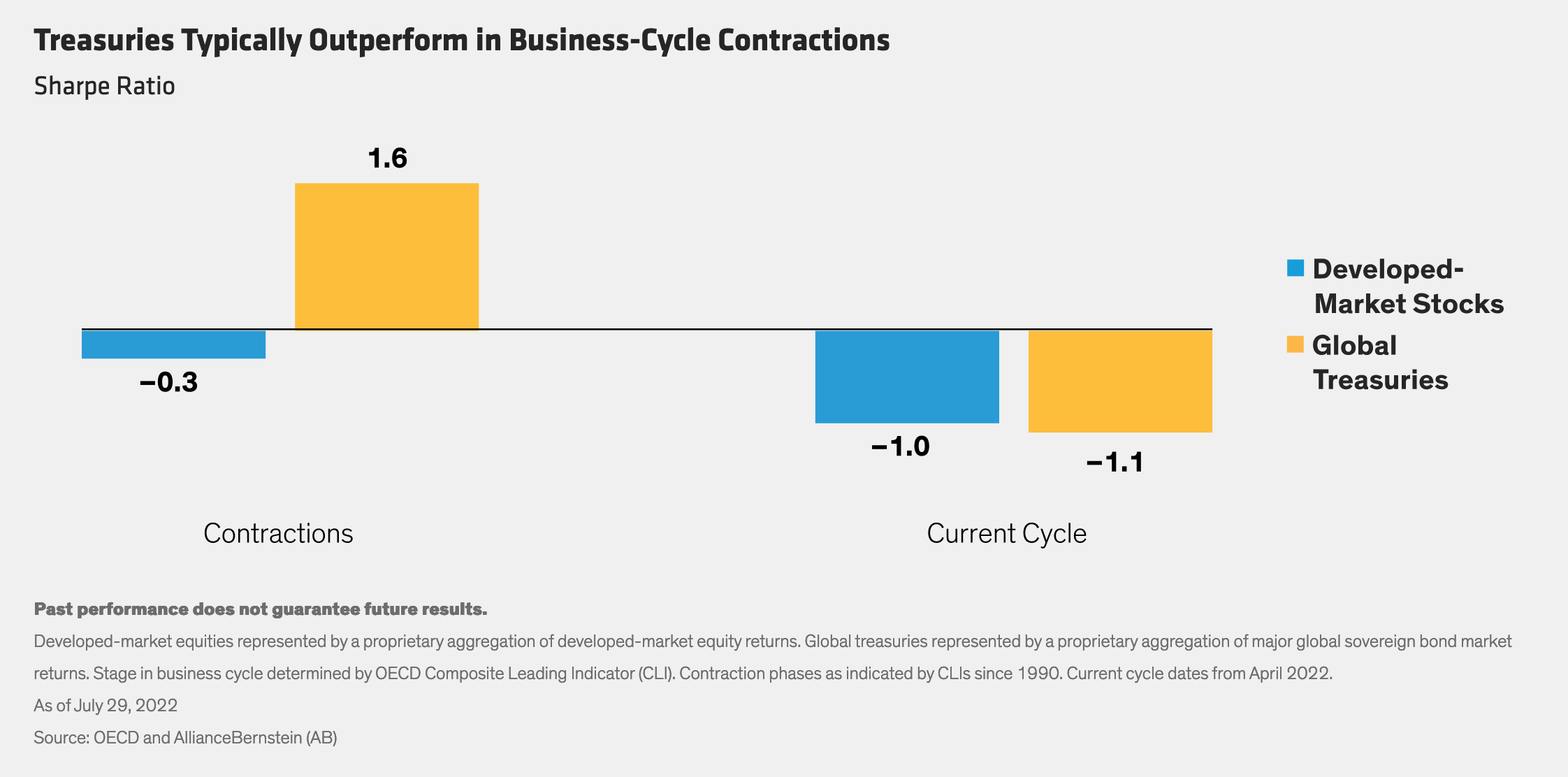

In this environment, we see less downside risk for global government bonds—and both higher income and diversification potential. In fact, government bonds have historically produced a better risk/reward balance than developed-market equities when economies have sputtered, and inflation had typically subsided, based on business-cycle contractions since 1990 (Display). Both assets have struggled so far in the current cycle, but the contraction is just three months along, and includes July’s equity surge. By that measure, it’s still early.

Given the potential for less volatility and better returns from global government bonds, we think it’s an opportune time to consider adding duration exposure to diversify against equity volatility. The climate has changed from just six months ago and will likely change again. Multi-asset investors must be dynamic in applying the tools likely to be most effective as conditions evolve.