by William Smead, Smead Capital Management

Since the low in January of 2016, oil prices have rebounded to a recent price around $54. What is Smead Capital Management’s position on oil prices and investments in oil-related securities? What does history say about the price of oil and its long-term trends? Do non-economic oil market participants tell you what you need to know about the future of oil prices?

Long History

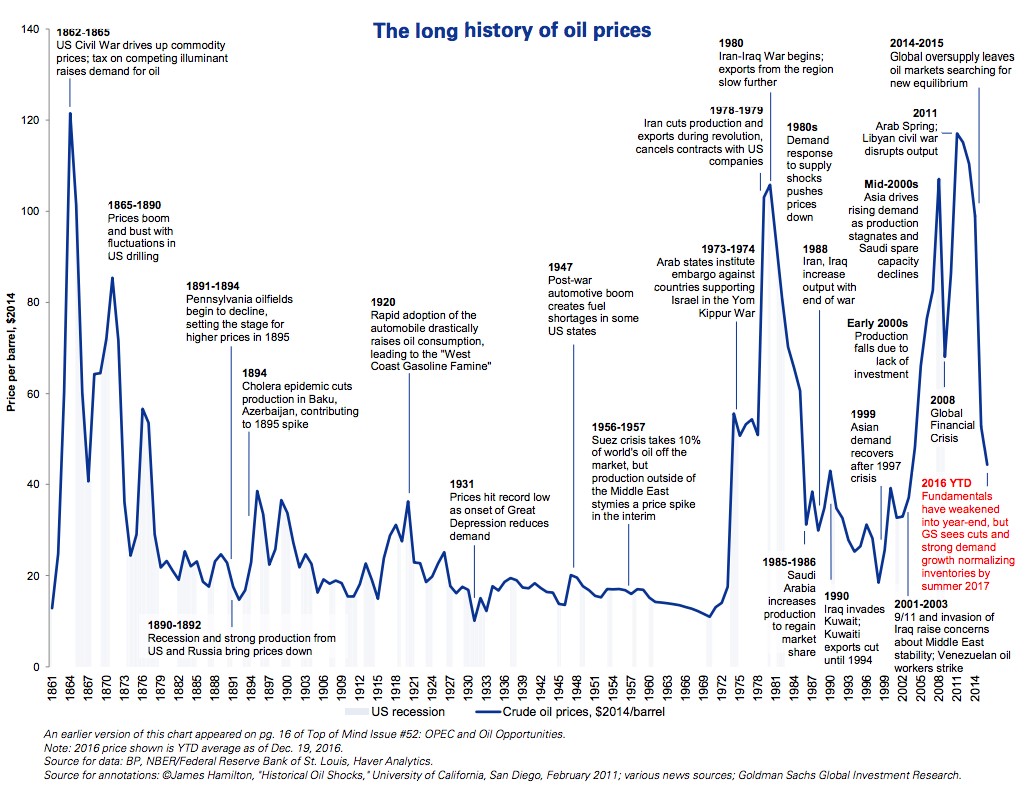

As you can see from the following chart — in which the price per barrel has been adjusted to reflect the USD in 2014 terms — oil has a storied history of boom and bust cycles.1 Oil peaked during the Civil War due to supply shortages and then was pummeled off and on for 27 years by new oil discoveries. A spike in 1894 for a supply disruption in Azerbaijan and the rapid adoption of the automobile by 1929 kept the prices up to $40. These episodes came between long stretches where prices went back and forth around $20 per barrel. In affect, oil was in a bear market off and on until 1972.

Oil peaked in 1981 around $110 per barrel and bottomed at $20 in 1999. In the spring of 2011, oil nearly exceeded the all-time high price near $120 per barrel. Therefore, we believe this bounce to $54 per barrel is very much a dead-cat bounce or bear market rally from a historical standpoint.

Non-Economic Investors

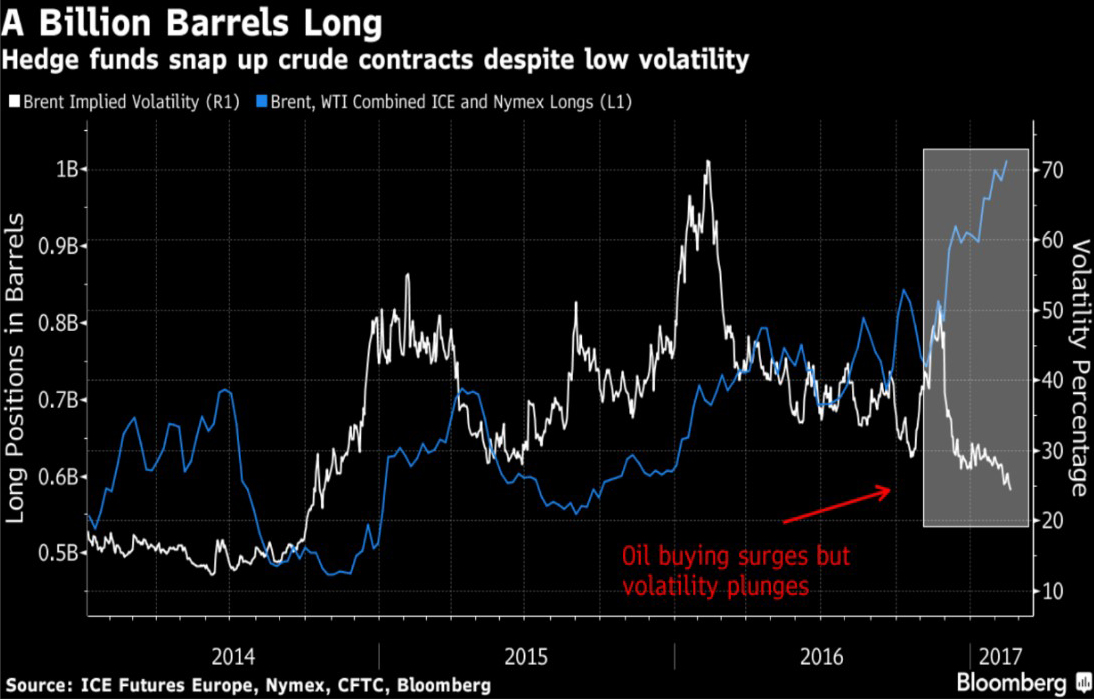

The chart below compares the volatility of oil prices with the volume of long oil contracts held by hedge funds on the commodity futures exchanges.2 It shows that hedge funds were optimistic in 2014 when oil was near $115 and again in early 2015. In the last few months, their enthusiasm has exploded to record highs on the move to $54 per barrel. This is a classic example of a crowded trade, where you start with almost no one believing in higher prices and you end up with almost everyone believing.

When a market has been abused by declining prices as much as oil did from 2014’s high to January 2016’s low, it usually takes years to regain a high level of enthusiasm. Think of how negative the experts were on U.S. stocks from 2009 to as recently as right before the 2016 November election. Think of how notorious those who were negative about the U.S. became during that era. This “wall of worry” has carried stock prices from 676 to around 2,363 on the S&P 500 Index as we write this missive in February of 2017.

These charts don’t guarantee anything; nor do they give any short-run clues about where oil prices are going. They do seem to argue that this is a bear-market rally and that history tends to drive prices to around $20 per barrel in 2014 dollar terms. The oil business is cyclical and not that far away from a boom which caused Canadian tar sands and American fracking companies to create unusual wealth in a short period of time.

Lastly, when oil prices did hit a temporary low in early 2016, private equity companies were anxious to provide capital to the over-leveraged oil producers. These zombie companies have been kept alive and maintain hope of getting back to $80 per barrel. If that happens we’d tip our caps to them. However, we think it is more likely that oil is currently peaking around $54 per barrel, and that oil investments will be available to contrarians like us at lower oil prices and at much better terms.

Warm Regards,

William Smead

1Source: Business Insider

2Source: Bloomberg

The information contained in this missive represents Smead Capital Management’s opinions, and should not be construed as personalized or individualized investment advice and are subject to change. Past performance is no guarantee of future results. Bill Smead, CIO and CEO, wrote this article. It should not be assumed that investing in any securities mentioned above will or will not be profitable. Portfolio composition is subject to change at any time and references to specific securities, industries and sectors in this letter are not recommendations to purchase or sell any particular security. Current and future portfolio holdings are subject to risk. In preparing this document, SCM has relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources. A list of all recommendations made by Smead Capital Management within the past twelve-month period is available upon request.

© 2017 Smead Capital Management, Inc. All rights reserved.

This Missive and others are available at www.smeadcap.com.