by Lance Roberts, Clarity Financial

I was recently watching a movie about the FBI trying to bring down a terrorist cell in the U.S. During their investigation, their evidence board became more and more cluttered with people, evidence, and locations as they attempted to track down the “cell.” At first, the clues were disparate, and they didn’t provide a clear path to the end goal. But as more clues were obtained, the bigger picture emerged eventually leading to the successful ending of the terrorist threat.

It got me to thinking about what is currently happening in the markets. As stocks rang new highs last week, there were several disparate stories that caught my attention. Individually, each story is nothing to be overly concerned about, and are regularly dismissed by investors. However, when you begin linking these stories, a picture is beginning to emerge that suggests investors may be ignoring the evidence at their own peril.

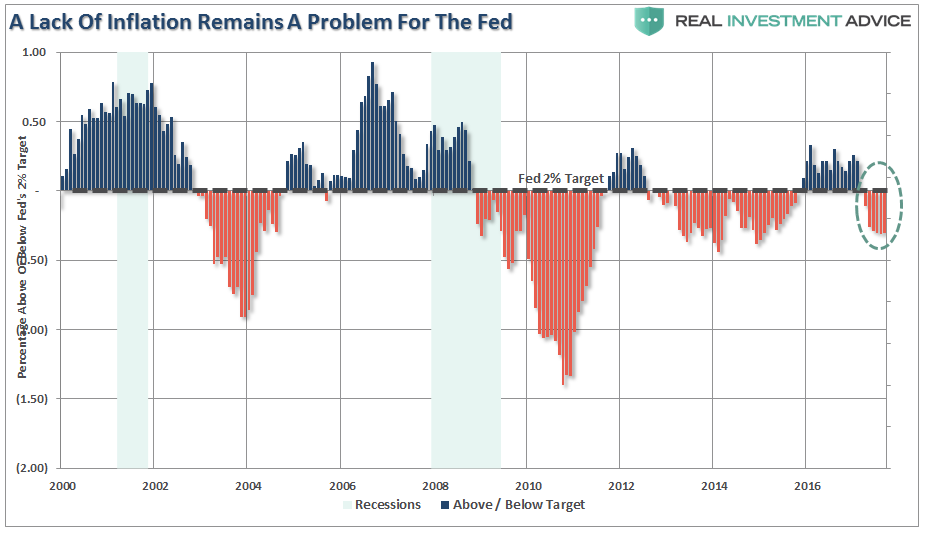

Story 1: CPI Remains Weak

Despite three hurricanes and wildfires over the last couple of months, core CPI (ex-aircraft) failed to register much inflationary pressure. One would have expected given the surge in demand for goods and services needed to rebuild destroyed communities.

However, despite the Fed’s hopes for a surge in inflationary pressures to justify further hikes in interest rates, inflationary pressures have been on the decline for the last several months.

Story 2: Real Wage Growth Slumps Along With Employment

Of course, the lack of inflation leads through to a decline in inflation-adjusted wages. While the chart below only goes back to 2008, wage growth has been non-existent since 1998. (For more detail read this.)

But as I discussed previously, even those wage numbers are skewed by the top 20% of income earners versus the bottom 80% which continue to see wages decline.

Story 3: Auto Originations Crash

As Wells Fargo announced this past week, the decline in auto loan originations continued tumbling 47% Y/Y to only $4.3 billion, the lowest print since the bank started disclosing this item back in 2013.

The problem is that it is not just Wells having this problem, but all banks. As shown in the chart below the number of banks reporting strong auto loan demand has been in decline for quite some time.

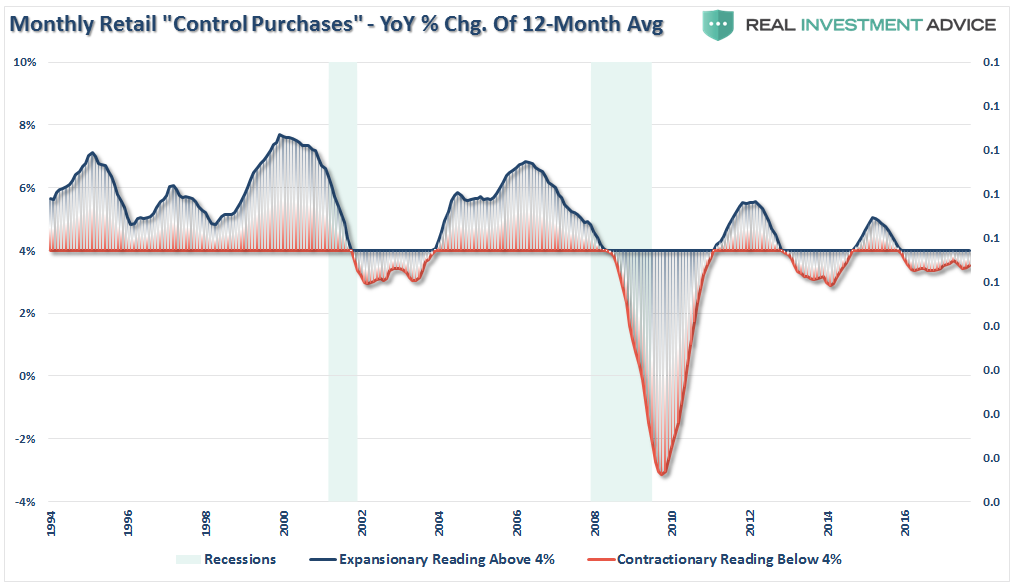

Story 4: Retail Sales Continue To Lag

It isn’t just auto either. Retail sales account for roughly 40% of personal consumption expenditures which makes up 70% of the economy. With wages stagnant, and the real cost of living on the rise, it is not surprising that with roughly 80% of Americans living paycheck-to-paycheck that retail sales continue to wane.

The chart below is the annual percent change in the 12-month average of “control purchases.” These are the items that consumers buy with regularity and shows why retail struggles aren’t just related to the “Amazon effect.”

Story 5: Pay-Tv Customers Decline

While “cutting the cord” may be a “thing,” this is much more a story about consumers being faced with a choice between making their mortgage payment or paying for cable. With budgets strained, consumers are actively seeking choices where they can get access to programming at much cheaper costs. From Bloomberg last week:

“Barring a major fourth-quarter comeback, 2017 is on course to be the worst year for conventional pay-TV subscriber losses in history, surpassing last year’s 1.7 million, according to Bloomberg Intelligence. That figure doesn’t include online services like DirecTV Now. Even including those digital plans, the five biggest TV providers are projected to have lost 469,000 customers in the third quarter.”

At least all the “low budget” films are getting a shot at a whole new audience. So sit back, grab some popcorn and take in “Galaxina” or “Cannibal Women From The Avocado Jungle.”

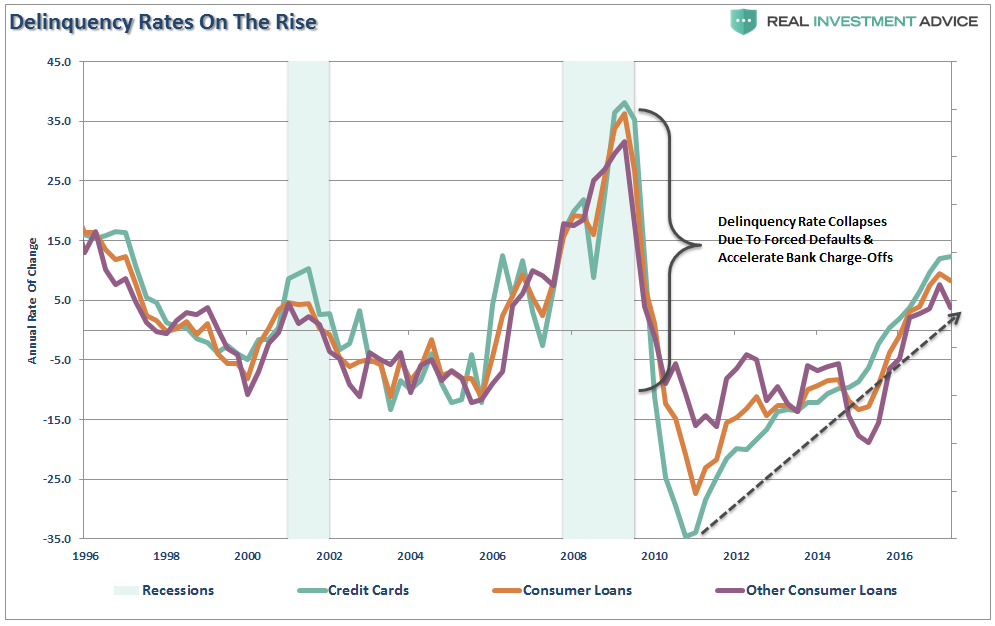

Story 6: Banks Ramp Up Loan Loss Reserves

In another interesting note this week, Citi, JP Morgan and BofA all boosted their “loan loss reserves” by the most in 4-years. Banks don’t boost reserves unless there is a rising risk of defaults on the horizon. From Zerohedge:

“Four months ago, when looking at the latest S&P/Experian data, we first reported that credit card defaults had surged the most since June 2013, a troubling development which ran fully counter to the narrative that the economy was recovering and the US consumer’s balance sheet was improving.

The troubling deterioration prompted Moody’s to pen its own report titled ‘Spike in Charge-off Rates Indicates a Slide in Underwriting Standards’ and as Moody’s analyst Warren Kornfelf wrote, the steep increase in credit card charge-off rates in 1Q’17 and 4Q’16 was the largest since 2009, and indicates that ‘strong underwriting standards in place since the financial crisis have deteriorated, potentially rapidly.'”

Of course, the following chart might just suggest why they are doing that.

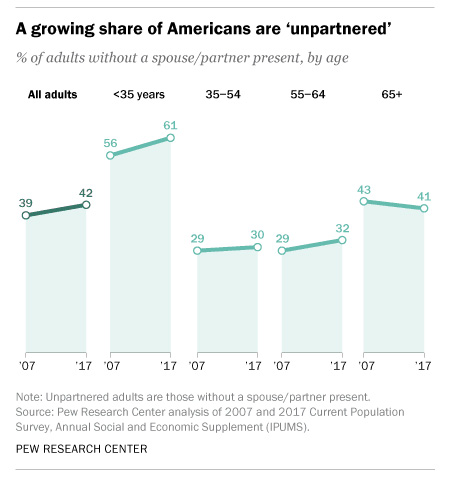

Story 7: Millennials Are Delaying Marriage Because Men Aren’t Earning Enough

As reported by The Hill this past week, more Americans are living alone today has risen sharply.

“The number of Americans living with a spouse or partner has fallen notably in the last decade, driven in part by decisions to delay marriage in the wake of a recession that hit new entrants into the workforce especially hard.

Forty-two percent of Americans live without a spouse or partner, up from 39 percent in 2007, according to the Pew Research Center’s analysis of U.S. Census Bureau figures. For those under the age of 35 years old, 61 percent live without a spouse or partner, up 5 percentage points from a decade ago.”

With more multi-generational families living together, the aging of the baby-boomer generation and a significant fall-off in birth rates, the huge demographic headwind is gaining momentum. The economic ramifications, as well as for the financial markets, is going to be extremely problematic. (Read this.)

Tying It All Together

As more clues become available, the risk to the financial markets becomes clearer.

All of these stories have a common thread – the consumer. While stocks continue to ratchet to all-time highs on expectations of tax cuts and reforms leading to stronger economic growth, the stories here all suggest something much more telling is happening beneath the surface.

Yes, household net worth has recently reached historically high levels. However, The majority of the increase over the last several years has come from increasing real estate values and the rise in various stock-market linked financial assets like corporate equities, mutual and pension funds.

But, once again, the headlines are deceiving even if we just slightly scratch the surface. Given the breakdown of wealth across America we once again find that virtually all of the net worth, and the associated increase thereof, has only benefited a handful of the wealthiest Americans.

As the Federal Reserve just recently reported, while the mainstream media continues to tout that the economy is on the mend, real (inflation-adjusted) median net worth suggests this is not the case overall. As stated, the recovery in net worth has been heavily skewed to the top 10% of income earners.

Of course, this explains why the largest number of the population over the age of 65 is still employed as they simply can’t afford to retire. The multi-generational households are on the rise, not by choice but by necessity. These are long-term headwinds that suggest economic growth will remain weak, and the rise in delinquencies, slow-down in auto demand, and weak retail sales all suggest consumers may have reached the limits of the debt-driven consumption cycle for now.

In other words, individuals are ratcheting up debt, not to buy more stuff, but just to maintain their current “standard of living.”

The disconnect between the stock market and real economic growth can certainly continue for now. Exuberance and confidence are at the highest levels on record, but the underlying stories are beginning to weave a tale of an economy that is very late in the current cycle.

Importantly, these are not short-term stories either. The long-term picture for the economy and the markets from the three biggest factors (Debt, Deflation, and Demographics) continues to build. These factors will continue to weigh on economic growth, and market returns, during the next generation as the massive wave a baby-boomers shift from supporters to dependents of the financial and welfare system.

As an investor, it is important to pay attention to the clues and the weight of the evidence. The success, or failure, of catching the end of the current bull market and economic cycle will have important implications to your long-term financial goals.

Copyright © Clarity Financial