by Matthew Peterson, and Ryan Detrick, LPL Research

KEY TAKEAWAYS

• June brings several significant events that have the potential to be market movers.

• A rate hike is widely expected at the Fed meeting, but what the Fed says about future hikes will be very important.

• The European Central Bank (ECB) and Bank of Japan (BOJ)also have highly anticipated meetings.

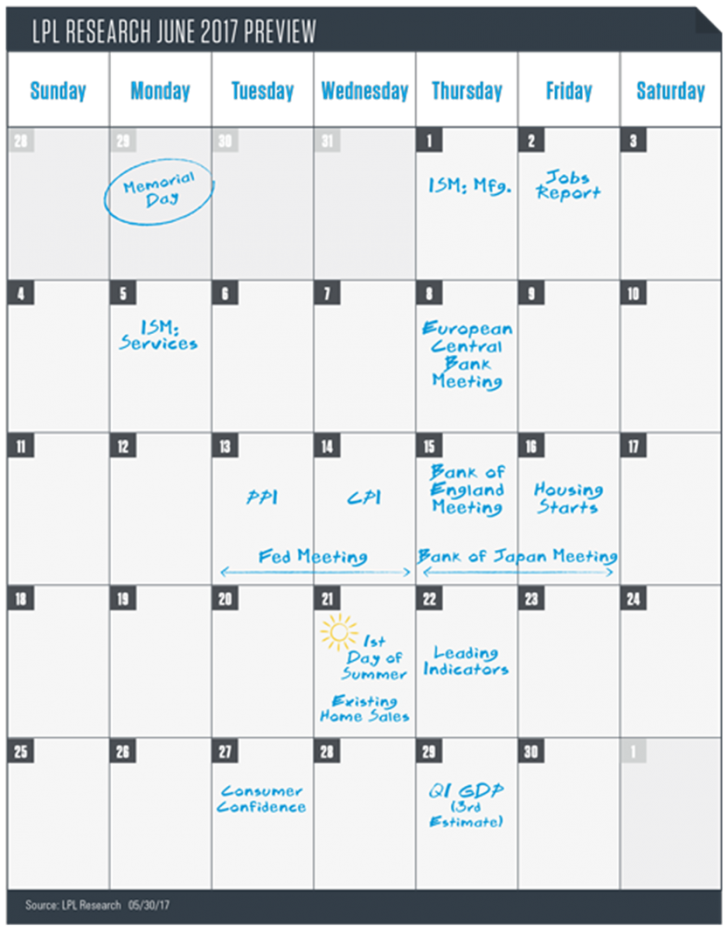

Summer will soon be here, as June 2017 brings with it longer days and summer vacations in the United States. It is also a month with three major central bank meetings. So far in 2017, the global equity rally has continued with new highs in the U.S., Europe, and emerging markets (EM). The global earnings backdrop is strong as well, supporting the moves to new highs. Not to mention 2017 has been one of the least volatile ever, with only four 1% moves for the S&P 500 Index in the first 100 trading days of the year. As we turn the page to June, it is important to stay on top of the most significant upcoming events. To help, we’ve created this guide to the June 2017 market calendar, providing an overview of the key events.

JUNE 2

EMPLOYMENT REPORT (MAY)

The U.S. economy created only 79,000 jobs in March 2017, but it bounced back with an impressive 211,000 in April, avoiding the first back-to-back sub-100,000 total since December 2010 and January 2011. One-year average job creation peaked in February 2015 at 261,000 per month and has slowed since to a still strong 186,000 [Figure 1]. Economists anticipate the trend continuing, with consensus expectations currently at 185,000 jobs created in May.

The center of gravity at the Federal Reserve (Fed) probably sees job growth as low as 100,000-125,000 per month as enough to continue to support the unemployment rate, currently at 4.4%. Wages will also be watched closely by the Fed. Average hourly earnings grew at 0.3% month over month in April and 2.5% year over year, with similar expectations for May. The labor force participation rate will receive some attention too as it has seen a small increase from the expansion low of 62.4% in September 2015, hitting 62.9% as of April 2017. A higher participation rate could help to limit wage pressures by increasing the supply of people willing to work. Wage pressures thus far have remained modest, and the Fed will be watching closely for any increase that may signal a pickup in inflation.

Last, going back to 1990, June has been the third-worst month for jobs growth (with August and December worse), so some type of seasonal weakness is a possibility. At the same time, jobs have been positive for a record 79 consecutive months, and job creation would need to slow to a sustained 25,000-50,000 per month to signal that a recession is near.

JUNE 8

ECB MEETING

The ECB meets June 8, with a lot of tension underneath a calm surface. The ECB has committed to buying 60 billion euro of bonds each month until December 2017. The ECB believes its program has been successful in aiding the economy and keeping the region from slipping into deflation. Eurozone inflation has been as high as 1.5%, still below the ECB’s 2% goal on an annual basis. However, economic growth and inflation in Germany has been running hotter than many in the country are comfortable with. Even German Chancellor Angela Merkel recently complained that ECB policy is keeping the euro too weak. In addition, the ECB is concerned that it may run out of bonds that meet its self-imposed guidelines for purchase.

Although we do not expect any change in policy at the upcoming meeting, the ECB will likely provide some guidance regarding future changes, specifically the amount of bond buying that will occur after the current program expires. The expectation is that bond buying will be reduced (a policy referred to as tapering) through the end of 2018. But with some countries, like Germany, desiring an end to monetary intervention and others (probably most notably Italy) looking to extend current policies, the ECB statement will be closely scrutinized. It will be hard, if not impossible, for it to satisfy all parties in the long run.

JUNE 13-14

FED MEETING

The Fed’s policymaking arm, the Federal Open Market Committee (FOMC), holds its fourth of eight meetings this year on June 13-14, 2017. At 2 p.m. ET on June 14, the FOMC will release its policy statement, a new set of members’ forecasts on the economy, labor market, and inflation, and a new set of “dot plots”(members’ forecasts of where they think the fed funds rate will be at the end of 2017, 2018, 2019, and in the “long run”). Fed Chair Janet Yellen will also hold the second of four post-FOMC meeting press conferences of the year at 2:30 p.m. ET on June 14. As of Friday, May 26, 2017, the market, as measured by fed funds futures, is pricing in an 88% chance of a 25 basis point (0.25%) rate hike at the June 2017 meeting.

Our view -- as expressed in Outlook 2017 -- remains that with the economy near full employment and inflation running near the Fed’s 2% target that the Fed will raise rates one to two more times in 2017 (for a total of two to three rate hikes in 2017). The minutes of the Fed’s May meeting also showed continued discussion of starting to allow maturing bonds to roll off the Fed’s balance sheet, though at a measured pace, potentially beginning later this year. Markets will be watching for more clarity on this issue from the Fed’s statement and press conference. Additionally, there is plenty of information for markets to digest between now and mid-June, which may change the odds of a hike at the June meeting. Key reports coming between now and then include consumer and producer inflation, the Institute for Supply Management’s (ISM) manufacturing and non-manufacturing indexes, employment, and retail sales. If these reports underwhelm, rate hike expectations may fall.

JUNE 15

BOJ MEETING

Like the ECB, the BOJ is still engaged in buying bonds, but it is also buying stocks, to help support the economy. Also like the ECB, the BOJ can point to progress being made on the economic front, but with growth still subpar and inflation below target, we expect the BOJ will maintain its current policy. There may be an acknowledgement of the BOJ’s growing balance sheet, but little if any real policy changes.

If both the BOJ and the ECB largely maintain the status quo, we expect it to be modestly positive for global equities. One would also think that a tightening Fed and continued loose policy in Europe and Japan would be positive for the dollar relative to the other currencies. However, the dollar has been in something of a downtrend recently. Should either the BOJ or ECB statement be more dovish than anticipated, that may be enough to bump the dollar higher, at least in the short term.

JUNE 29

THIRD ESTIMATE Q1 2017 GDP

The third estimate of first quarter 2017 gross domestic product (GDP) will be released on June 29. The second estimate was released on May 26, and saw real GDP growth revised up from 0.7% to 1.2%. The average revision (up or down) from the second estimate to the third is 0.2%, smaller than the 0.5% from the first to the second. The big story for first quarter GDP was the largest contribution from business fixed investment since the first quarter of 2012 and the fourth-best contribution of the millennium. However, weak consumer spending (slightly upgraded in the last revision) and a large negative contribution from inventory growth extended the persistent seasonal pattern of a disappointing first quarter.

The third estimate of first quarter GDP will have economists looking ahead to the initial estimate of second quarter GDP on July 28. Based on the Fed Bank of Atlanta’s NowCast model, expectations are for growth to rebound to over 3%, helped by a bounce back in inventories, which have a tendency to reverse extremes, and consumer spending, which has been a mostly steady contributor throughout the expansion. Business investment is likely to slow but is expected to make another meaningful contribution, a theme we believe will continue as the economic and policy environment becomes more supportive of businesses investing in their own future growth and productivity.

CONCLUSION

June is a month that historically has seen some volatility. Who could forget last year and the Brexit sell-off? With three major central banks set to announce new interest rate policy in the span of one week, the odds for some summertime volatility is higher than usual. After weak growth in the first quarter, all economic data will be heavily scrutinized to see if the U.S. economy might stage a second half bounce. With summertime upon us, it is important to remember to have a plan in place before these events unfold. And don’t forget your sunscreen!

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results.

Any economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal and potential illiquidity of the investment in a falling market.

The fast price swings in commodities and currencies will result in significant volatility in an investor’s holdings.

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

DEFINITIONS

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Federal Open Market Committee (FOMC) is the branch of the Federal Reserve Board that determines the direction of monetary policy. The eleven-person FOMC is composed of the seven-member board of governors, and the five Federal Reserve Bank presidents. The president of the Federal Reserve Bank of New York serves continuously, while the presidents of the other regional Federal Reserve Banks rotate their service in one-year terms.

The Fed Funds futures contract represents the average daily fed funds effective rate for a given calendar month as calculated and reported by the Federal Reserve Bank of New York. It is designed to capture the market’s need for an instrument that reflects Federal Reserve monetary policy.

Gross Domestic Product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The U.S. Institute for Supply Managers (ISM) manufacturing index is an economic indicator derived from monthly surveys of private sector companies, and is intended to show the economic health of the U.S. manufacturing sector. A PMI of more than 50 indicates expansion in the manufacturing sector, a reading below 50 indicates contraction, and a reading of 50 indicates no change.

Copyright © LPL Research