“Jam-Packed June”

by Burt White, Chief Investment Officer, LPL Financial

KEY TAKEAWAYS

· June is jam-packed with major market events that may go a long way toward determining the direction of the stock market.

· These events, coupled with the age of the economic cycle and election-related uncertainty, suggest that stocks may experience an uptick in volatility next month and may give us a dip to buy.

· Look for more from us on these events in future blogs and weekly publications.

June is jam-packed with major market events. This week we take a look at these events and potential market implications, highlighted by the “Brexit” vote and the Federal Reserve (Fed) policy meeting.

Jam-packed june

There are a number of big market events coming up next month that may go a long way toward determining the direction of equity markets over the balance of the year:

· ECB policy meeting (June 2). The European Central Bank (ECB) has embarked on a massive bond buying program (quantitative easing [QE])—similar to the Fed’s programs in recent years—to help reinvigorate the region’s economy and fight deflation. A major shift in policy at the June meeting is unlikely given the central bank will not start its previously announced corporate bond buying program until June (the ECB is already buying sovereign debt; the corporate bond expansion was announced in March 2016). Markets will be looking for signs from ECB Chief Mario Draghi that the ECB is inclined to expand the program even further as needed later this year. Any additional stimulus would likely weaken the euro against the U.S. dollar. We believe the ECB will eventually loosen monetary policy even further, given the challenging intermediate-term growth outlook and persistent deflationary pressures this year. The ECB may wait until after the Brexit vote on June 23 to make any changes.

· OPEC meeting (June 2). A possible deal between OPEC and non-OPEC (i.e., Russia) producers to freeze output to support crude oil prices fell apart in April 2016 when Iran failed to go along. Iran has stated its intention to boost production back to levels before Western sanctions were put in place; Saudi Arabia insists that Iran must freeze production as well, making a compromise very unlikely. We are encouraged by recent progress toward oil supply-demand rebalancing in the U.S. and the resulting rise in prices. While our base case calls for status quo overseas, and we acknowledge OPEC’s diminished influence and fragmentation, it is possible that overseas producers surprise investors and come up with a creative way to support global oil markets.

· May Employment report (June 3). The U.S. government’s tally of the health of the labor market is released every month, so this report does not make June different from any other month. However, given the market’s intense focus on the Fed’s June policy meeting later in the month, this number will take on greater importance. Consensus estimates are calling for 200,000 net new jobs created in May, up from the lackluster 160,000 created in April. Equally as important to the Fed are wages, which rose 2.5% year over year in April of 2016. Should these data points, along with the Institute for Supply Management’s Manufacturing Index for May—due out on June 1—reflect further strengthening of the labor market, the odds of a June Fed rate hike may increase to 50% or more, after falling under 5% as recently as May 16, 2016.

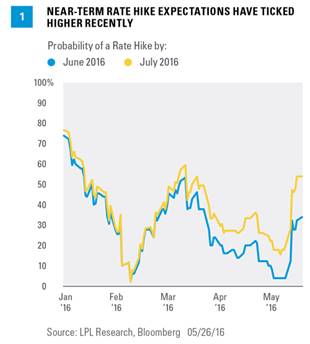

· FOMC meeting, economic forecasts, and Chair Janet Yellen press conference (June 14-15). Although stocks have historically performed well during the first year after the initial Fed rate hike of an economic cycle, investor anxiety around the timing of rate hikes has been higher this cycle, making the June meeting particularly important for markets. We believe the market may still be underestimating the probability of an early summer rate hike and a second hike by year-end. Fed fund futures are indicating a 34% probability of one rate hike by June and 54% by July (as of May 24, 2016) [Figure 1], and are pricing in just a one-in-three chance of a second hike by December, even though Fed officials have been warning markets that—election or not—two hikes are likely in 2016. We believe the next hike is more likely to come in July than June because of the June 23 Brexit vote; two hikes this year remains our base case.

· Bank of Japan monetary policy meeting (June 15-16). The Bank of Japan (BOJ), like the ECB, has embarked on a massive bond buying program, i.e., QE, to reinvigorate its economy. The central bank surprised markets at its last policy meeting on April 28, 2016, taking no action, which drove the yen sharply higher. Expectations were that the central bank would either lower interest rates further or expand its purchases of Japanese securities (or both, including additional equities purchases) to help weaken the yen and support the country’s exporters. Some have even called for the aggressive (what some would call radical) money “helicopter drop,” which is just like it sounds—where the central bank prints money and distributes it directly to its citizens. Japan’s economy averted recession during the first quarter of 2016 as its gross domestic product (GDP) expanded 0.4% (not annualized) and the yen has weakened versus the U.S. dollar since the April BOJ meeting, leaving some doubt as to whether the BOJ will take additional action in June. However, unless growth and inflation pick up in the coming months, we would expect the BOJ to increase the size of its QE program soon, potentially putting added upward pressure on the dollar.

· Brexit vote (June 23). The upcoming “Brexit” vote (a referendum on whether the U.K. will remain part of the European Union) has several implications, both political and economic. From a political perspective, the biggest implication would be the tacit support for other anti-EU movements across the continent, including political pushes for more autonomy in Spain (which has elections coming up on June 26), France, and Italy. Estimates on the economic impact of a Brexit, while highly partisan, suggest potential negative impact on GDP of between 1% and 3% due to a reduction in trade. Longer term, potential productivity declines and renegotiations of trade agreements may further impact growth. Perhaps the biggest wildcard is what would happen to London as a banking center and whether U.K.-based companies would choose to relocate. Recent polls show “remain” leading “exit” by as much as 50% to 38%, with 11% still undecided.

Seasonal weakness

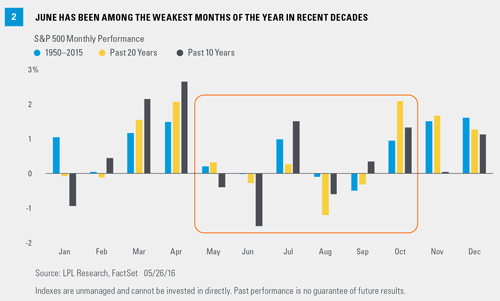

As we discussed in our Weekly Market Commentary “Is Sell in May Just a Cliché?” May through November has historically been the weakest six-month period to own stocks. Investors trying to exploit this pattern would have sold stocks on May 1 and would buy them back on October 31. How about June? Over the past 10 years, June has been one of the weakest months for stocks [Figure 2]; the month has averaged -1.5% and -0.3% losses for the S&P 500 over the past 10 and 20 years and, with a marginal average decline since 1950 (-0.03%), is the worst of all 12 months. Hardly encouraging. These seasonal patterns do not always hold, but are a reason to be a bit careful as summer rolls around.

Conclusion

June is jam-packed with potential market-moving events that may go a long way toward determining the direction of financial markets and market volatility over the balance of the year. These events, coupled with the age of the economic cycle and election-related uncertainty, suggest that stocks may experience an uptick in volatility next month and may give us a dip to buy. But volatility works in both directions, so let’s hope for some of the positive flavor. Look for more from us on these events in future blogs and weekly publications.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal, and potential liquidity of the investment in a falling market.

All investing involves risk including loss of principal.

Quantitative easing (QE) refers to the Federal Reserve’s (Fed) current and/or past programs whereby the Fed purchases a set amount of Treasury and/or mortgage-backed securities each month from banks. This inserts more money in the economy (known as easing), which is intended to encourage economic growth.

INDEX DESCRIPTIONS

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Institute for Supply Management (ISM) Index is based on surveys of more than 300 manufacturing firms by the Institute of Supply Management. The ISM Manufacturing Index monitors employment, production inventories, new orders, and supplier deliveries. A composite diffusion index is created that monitors conditions in national manufacturing based on the data from these surveys.

Copyright © LPL Financial