by Ben Carlson, A Wealth of Common Sense

“Investing is intolerably boring and over-exacting to anyone who is entirely exempt from the gambling instinct; whilst he who has it must pay to this propensity the appropriate toll.” – John Maynard Keynes

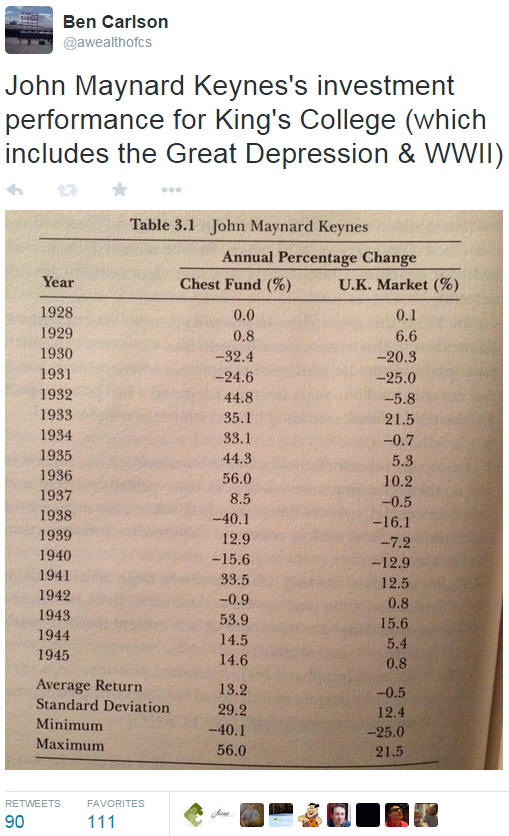

John Maynard Keynes gets plenty of attention in the world of economics based on his macroeconomic theories, but many don’t realize that Keynes was also an extraordinary investor. I tweeted out Keynes’s investment record last night:

These performance figures generated a large number of responses. The thing I found interesting is that the overwhelming majority of the comments were about the fact that Keynes’s returns were far too volatile. Many noted that there is no way investors would put up with this type of volatility or drawdowns in today’s investment world. The conclusion was that Keynes would certainly be fired if he were managing money this way today.

Before I get into some of my thoughts on these reactions, let’s take a look at Keynes’s investment philosophy, courtesy of an old Journal of Finance write-up:

1. A careful selection of a few investments having regard to their cheapness in relation to their probable actual and potential intrinsic value over a period of years ahead and in relation to alternative investments at the time;

2. A steadfast holding of these fairly large units through thick and thin, perhaps for several years, until either they have fulfilled their promise or it is evident that they were purchased on a mistake;

3. A balanced investment position, i.e., a variety of risks in spite of individual holdings being large, and if possible opposed risks.

So basically Keynes was a fundamental, focused investor, similar to Warren Buffett in that he practiced buy and hold in a select group of stock holdings. It’s also interesting to note that even with a small number of holdings he still tried to diversify his risks.

Now back to the question of whether or not Keynes would have been fired by investors today if he showed similar performance, volatility and drawdown numbers. Unfortunately, I agree with the responses from Twitter in this instance, which is a shame. This is a legendary investment record during one of the most difficult periods in history to be an investor.

But short-termism and status quo are so widely practiced in the institutionalized world of investing that it’s highly unlikely that investors would have the requisite patience to stick with someone like Keynes today. Investors would certainly chase performance after the string of good years, but very few would be able to earn the overall outperformance figures.

For most investors the goal shouldn’t necessarily be to beat the market, but to not beat themselves. And then there’s the question of actually discovering the next John Maynard Keynes. But putting all of that aside for the moment — there is an unbelievable amount of time, effort and money spent on the singular goal of beating the market. It’s the entire reason many fund managers exist. Yet the conundrum is that there are very few investors out there with the correct level of patience or discipline to see through the type of strategy that’s required to actually beat the market by a wide margin.

In a recent Think Advisor piece, Yale’s David Swensen summed this up nicely:

Active management strategies demand uninstitutional behavior from institutions, creating a paradox that few can unravel. Establishing and maintaining an unconventional investment profile requires acceptance of uncomfortably idiosyncratic portfolios, which frequently appear downright imprudent in the eyes of conventional wisdom. The most attractive investment opportunities fail to provide returns in a steady, predictable fashion.

This description fits Keynes’s investment principles perfectly. And because he ran an idiosyncratic portfolio, it’s highly likely Keynes would be fired by professional investors in today’s day and age.

Sources:

A Wiser Approach to Alternative Investing (Think Advisor)

The Warren Buffett Portfolio

Further Reading:

The Lollapalooza Effect in Active Management

Do Risk-Adjusted Returns Matter?

Further Viewing:

How Keynes Gave Up on Market Timing (Sensible Investing TV)

Subscribe to receive email updates and my monthly newsletter by clicking here.

Follow me on Twitter: @awealthofcs

Copyright © A Wealth of Common Sense