March 5, 2013

by Michelle Gibley, CFA, Director of International Research, Schwab Center for Financial Research

Key points

- The negative case for the eurozone is well known, with an inconclusive election in Italy just the latest event.

- However, positive developments are the untold story, and the future could improve.

- We have a positive outlook for eurozone stocks, preferring the markets of core countries such as Germany and France, and individual stocks in cyclical sectors.

Europe's economy is in recession, austerity is biting, politicians have repeatedly resisted measures to unite, and the Italian election is inconclusive—are there any reasons to invest in the eurozone? Actually, we think there are.

In spite of their many challenges, eurozone countries have begun to institute crucial reforms, their credit markets are thawing, and the Organisation for Economic Co-operation and Development (OECD) leading indicator and purchasing manager indexes suggest the eurozone economy has improved from the low hit in the fall. Corporate earnings and valuations remain relatively low, making it easier for companies to surpass investor expectations, and making stocks appear comparatively cheap. And in light of easing global uncertainty, we see fewer risks of a global slowdown harming the eurozone's nascent improvement.

All of these factors contribute to our positive view on eurozone equities as a whole. Among individual countries, we prefer the stock markets in Germany and France. Select individual stocks of companies that are in cyclical sectors or have high foreign exposure or strong brands may also be worth a look.

Europe or eurozone?

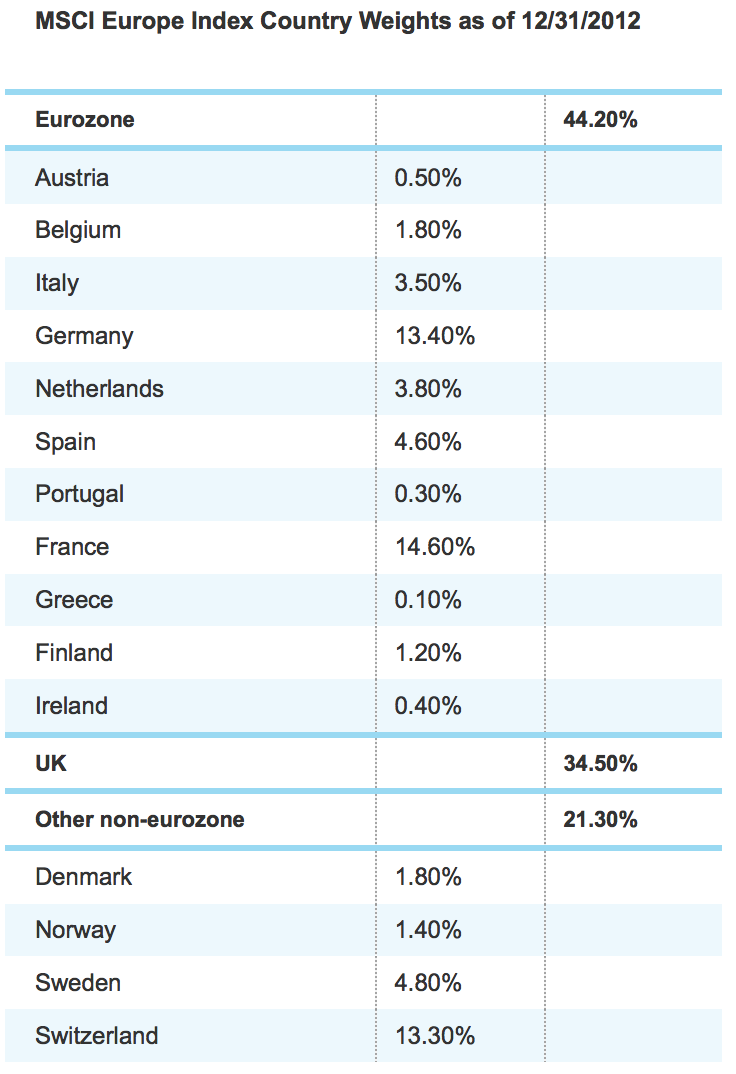

First, keep in mind that the eurozone is not the same as Europe. The eurozone is a monetary union of 17 countries using the euro as a common currency, with the European Central Bank (ECB) presiding over monetary policy. Notably, the eurozone doesn't contain Switzerland, the UK, Sweden, Norway, or the countries of Eastern Europe—they all still have their own currencies and central banks. The European Union is a larger economic and political group of 27 member states, brought together with the aim of free trade, open borders and flows of capital.

To get a sense of how the different countries of the eurozone fit together, look at the relative weightings in the MSCI Europe Index:

Why we're positive on the eurozone

Last summer, we upgraded the region to a neutral view after two turning points in the eurozone's sovereign debt crisis: European Central Bank (ECB) President Mario Draghi's vow in July 2012 to "do whatever it takes" to preserve the euro, and the introduction of a conditional bond purchase program—the Outright Monetary Transactions (OMT)—shortly thereafter. We believe the OMT has reduced the threat of bailouts by providing a credible lender of last resort—a "safety net" of sorts.

We further upgraded the region to a positive outlook in January 2013 due to several factors:

- Improved access to credit. In January, the Group of Governors and Heads of Supervision that governs global bank rules delayed and relaxed Global Basel III capital requirements for banks—a de facto easing of monetary conditions. We still believe banks need additional capital and will deleverage, but less urgently. Meanwhile, improved confidence and the search for yield have created strong demand for government, bank and corporate debt, which helps give corporations much-needed access to credit at a time when bank lending is still weak. Historically, European companies have relied more on bank lending than their American counterparts; we may be seeing the start of a shift away from bank lending and toward corporate debt issuance.

- Fiscal progress and labor reforms. Current account deficits are shrinking, according to the OECD, and the International Monetary Fund (IMF) notes that the peripheral countries may have primary budget surpluses (fiscal surplus before interest expense) in 2013. Unit labor costs are falling in Spain, Portugal and Ireland, driven either by significant wage decreases or by productivity growth resulting from job cuts. Reforms that make it easier for companies to hire and fire can improve profitability by allowing them to respond faster to changes in demand. Additionally, opening up "closed" professions to new entrants can introduce competition and reduce prices. (In a closed profession, the government only grants a limited number of licenses to entrants, such as taxi drivers or pharmacists.)

Falling costs improve competitiveness

Source: FactSet, OECD. As of February 19, 2013. Indexed to 100=Dec. 31, 2003.

- Potential for economic turnaround. The consensus estimate among Bloomberg economists is that the eurozone will transition from recession to expansion later in 2013. As long as the region's economy shows consistent (albeit modest) signs of improvement, stocks could rise—equities tend to follow trends in growth rather than the absolute level of growth. It's true that fiscal austerity will continue, but we expect that austerity measures will be less harsh in the future; deficit-reduction goals are already being extended to more realistic timeframes. Policymakers have come to the realization that harsh austerity only makes matters worse: Sharp fiscal tightening tends to increase unemployment and decrease tax revenues, leading to growing deficits—the opposite of the desired result.

Eurozone GDP could emerge from recession

Source: FactSet, Bloomberg, Eurostat. As of February 19, 2013.

- Reduced global uncertainty. Several headwinds from 2012 have been reversed in 2013: the United States avoided going fully off the "fiscal cliff"; China's economy is recovering; the eurozone is no longer in crisis; and Japan's central bank is expected to accelerate easing.

- Depressed earnings and valuations. There are still downside risks, but we feel the risk/reward profile is favorable. In addition to the potential for sales growth to accelerate, earnings have additional upside as margins have room to expand. Analysts and corporations could move from cutting earnings forecasts to raising them. For some time, eurozone stocks moved roughly in tandem with US stocks, but for the last several years they've dramatically underperformed. Eurozone stocks look poised for a catch-up rally, although we don't expect them to completely close the gap with US stocks as growth prospects are lower in the eurozone.

Eurozone stocks have underperformed recently

Source: FactSet, Standard & Poor's, MSCI. As of February 19, 2013.

Risks in the eurozone

While we have a positive outlook on the eurozone for all the reasons above, it's worth acknowledging some of the risks in the region:

- Italy's inconclusive election increases uncertainty and threatens reform progress. Markets are likely to be skittish as either another election or a coalition government is likely to result in an unstable government that is unable to last a full five-year term. The uncertainty could prompt worries about a bailout for Italy and contagion that ensnares Spain, but we view a new bailout in the near term as unlikely. Typically, high levels of bond market stress eventually force policymakers to make uncomfortable decisions to reduce deficits, and we believe Italy's politicians want to avoid a bailout that would involve oversight by outsiders.

- New crisis fighting measures are untested. No country has asked for assistance yet, so the OMT hasn't been implemented. Additionally, the ability of the European Stability Mechanism (ESM) to recapitalize banks is still uncertain.

- Bank union progress has stalled. Policymakers have yet to determine a single resolution authority to wind up failing banks or a shared safety net for all depositors in terms of deposit insurance. Progress needs to continue to maintain confidence in the eurozone banking system.

- Spain could still need a bailout. Government corruption allegations could reduce support for reforms, and the bursting of the housing bubble could create additional bank capital needs. A 40% weight in financials is a risk factor for investors in Spain's IBEX 35 Index.

- Germany's general election in September could distract Chancellor Merkel. She's likely to keep her position, but potentially with different coalition partners, and she could end up more focused on local issues—to the detriment of larger eurozone concerns.

- Euro could rise as ECB easing lags other major central banks. The euro has strengthened due to improved fundamentals, reduced uncertainty, and a decline in the ECB's balance sheet, while the pound, US dollar and the yen could remain weak on a relative basis thanks to the Bank of England, Federal Reserve and Bank of Japan's expanding balance sheets.

Eurozone stocks and the euro have moved together recently

Source: FactSet, Reuters, MSCI. As of February 19, 2013.

A rising euro could hurt exports, particularly for countries with low-value exports more exposed to competition. However, as long as the rise is modest, it's not necessarily a barrier for higher eurozone equity prices. Eurozone stocks and the euro have tended to move together in recent years, in concert with shifts in risk assessment.

Where to invest in the eurozone?

In general, we prefer the stock markets of core countries such as Germany and France, rather than the peripheral countries such as Spain and Italy. While stocks in peripheral countries could have strong rallies, they also potentially have higher downside risks as unstable governments and fiscal woes could result in market volatility.

In Germany, we see:

- Increasing business confidence.

- A large exposure to the consumer discretionary, technology, industrials, materials and energy sectors—all cyclical sectors that tend to do well when global growth reaccelerates, as we now expect.

- The possibility of rising household incomes. Chancellor Merkel recently softened her position on union demands for higher pay and increases in industry minimum wages. After more than a decade of wage restraint, rising incomes could encourage Germans to start spending.

So what are the risks? Germany would probably be asked to help weaker eurozone countries in the event of a bailout, and coming elections in the fall could reduce business and consumer confidence if the campaigning gets sufficiently negative.

In France, the outlook for the economy is a concern—but the outlook for stocks is more upbeat:

- France has many multi-national companies that are industry leaders with global presence, particularly in luxury goods, as well as access to both world-class infrastructure and cheap energy.

- While French labor laws are among the strictest in Europe, we are hopeful that reforms, such as the labor agreement reached in early 2013, are moving in the right direction, albeit very slowly. Improved labor flexibility could enhance profits.

We also like select individual stocks of companies that:

- Are cyclical and have high global exposure such as consumer discretionary, technology, industrials, materials and energy. We believe the global outlook is improving, and cyclical sectors tend to do well during this part of the business cycle. For example, while the European auto market is under pressure due to household deleveraging, declining car usage, and an average car age that is years younger than in the United States, the global auto market is recovering and companies with strong global brands could do well.

- Produce luxury goods. These companies tend to have strong pricing power and global exposure that can mitigate weak domestic spending in the company's home market. China is both a risk and opportunity, as the new government is cracking down on expensive gifts, but a growing middle class is spending on luxury. An additional positive is that the North American market may be recovering, reaccelerating at the end of 2012.

The sovereign debt crisis in Europe was dramatic and painful, and the region continues to face challenging economic conditions. However, we believe the eurozone is better positioned for growth in the future due to a variety of fiscal and labor reforms and an improved global outlook. Stocks appear attractively priced, and have opportunities to rise amid an improving global economic climate. All these factors contribute to our newly positive view on Europe.

Copyright © Schwab.com