by Kathrin Forrest, Equity Investment Director, Capital Group

KEY TAKEAWAYS

- Canadian equities have delivered impressive returns, but gains have been heavily concentrated in the materials, financials and energy sectors.

- Supportive fundamentals such as firm commodity prices and global demand could continue to drive earnings in the energy and materials sectors.

- Concentration risk remains high. Adding global exposure to sectors historically underrepresented in Canada can make for more resilient portfolios.

Canadian equities have delivered a quietly impressive run over the past three years, notching double-digit results in 2023, 2024 and 2025, primarily supported by strength in the materials, financials and energy sectors.

“This leadership is not surprising to Canadian investors, with our market heavily tilted toward commodity and banking companies,” says equity investment director Kathrin Forrest.

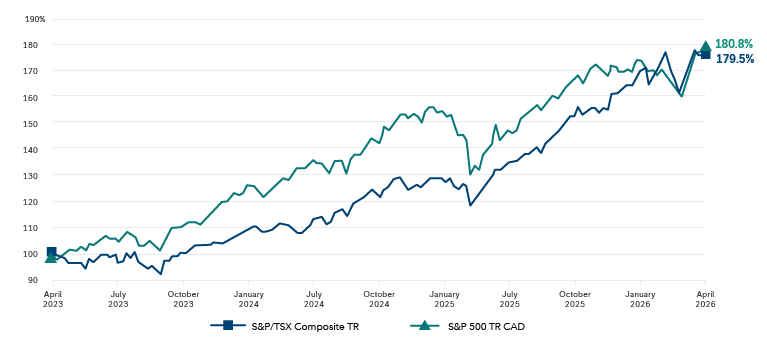

What may be surprising is the fact that Canadian equities have kept pace with U.S. equities over the past three years, from April 30, 2023, to April 30, 2026, with the S&P/TSX Composite Index notching cumulative gains of 179.5% compared to the S&P 500 Index’s 180.8% advance.

Canada holding its own

S&P/TSX Composite Index vs. S&P 500 Index

Three-year results April 30, 2023 — April 30, 2026

Sources: Capital Group, S&P Global.

Materials sector companies ranging from base metals to gold producers have been standouts, benefiting from firm commodity pricing and tight supply conditions. Financials have also meaningfully contributed, reinforcing the Canadian market’s resilience even amid economic and trade uncertainty, while the energy sector has helped drive significant gains and cash flow across Canadian producers.

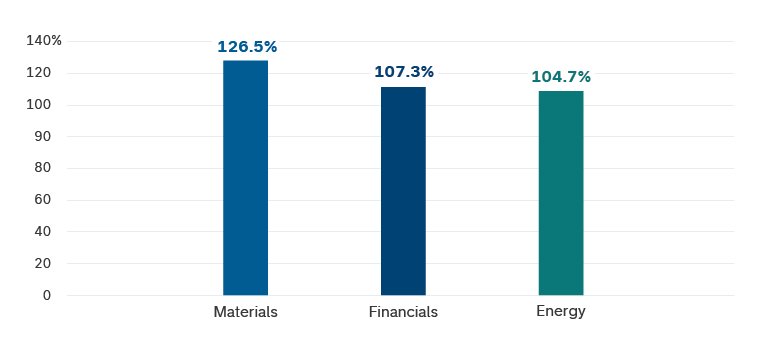

Leaders of the pack

Materials, financials and energy sector performances

Three-year results April 30, 2023 — April 30, 2026

Sources: Capital Group, S&P Global. Sector information reflects the S&P/TSX Composite Index.

According to Forrest, parts of this rally may still have room to run. The outlook for the physical economy remains constructive, with energy demand tied to global growth and industrial activity, while supply constraints across commodities continue to support pricing. This backdrop could sustain earnings strength in both energy and materials.

“Investors should, however, be mindful of concentration risk as it creates vulnerability,” says Forrest.

A more balanced approach consists of complementing Canadian holdings with companies outside Canada in sectors such as information technology and healthcare, which have been historically underrepresented in the Canadian market. This can help enhance diversification and improve risk-adjusted outcomes by reducing reliance on a narrow set of drivers at home.

“Canada’s rally may continue, but the most durable domestic portfolios are likely those that combine some of the country’s best in class companies with broader global opportunities,” says Forrest.

Kathrin Forrest is an equity investment director at Capital Group. She has 21 years of industry experience and has been with Capital Group for four years (as of 12/31/25). She holds a master's degree in economics from Wayne State University and holds the Chartered Financial Analyst® designation.

Copyright © Capital Group