by Steve Watson, Equity Portfolio Manager, Capital Group

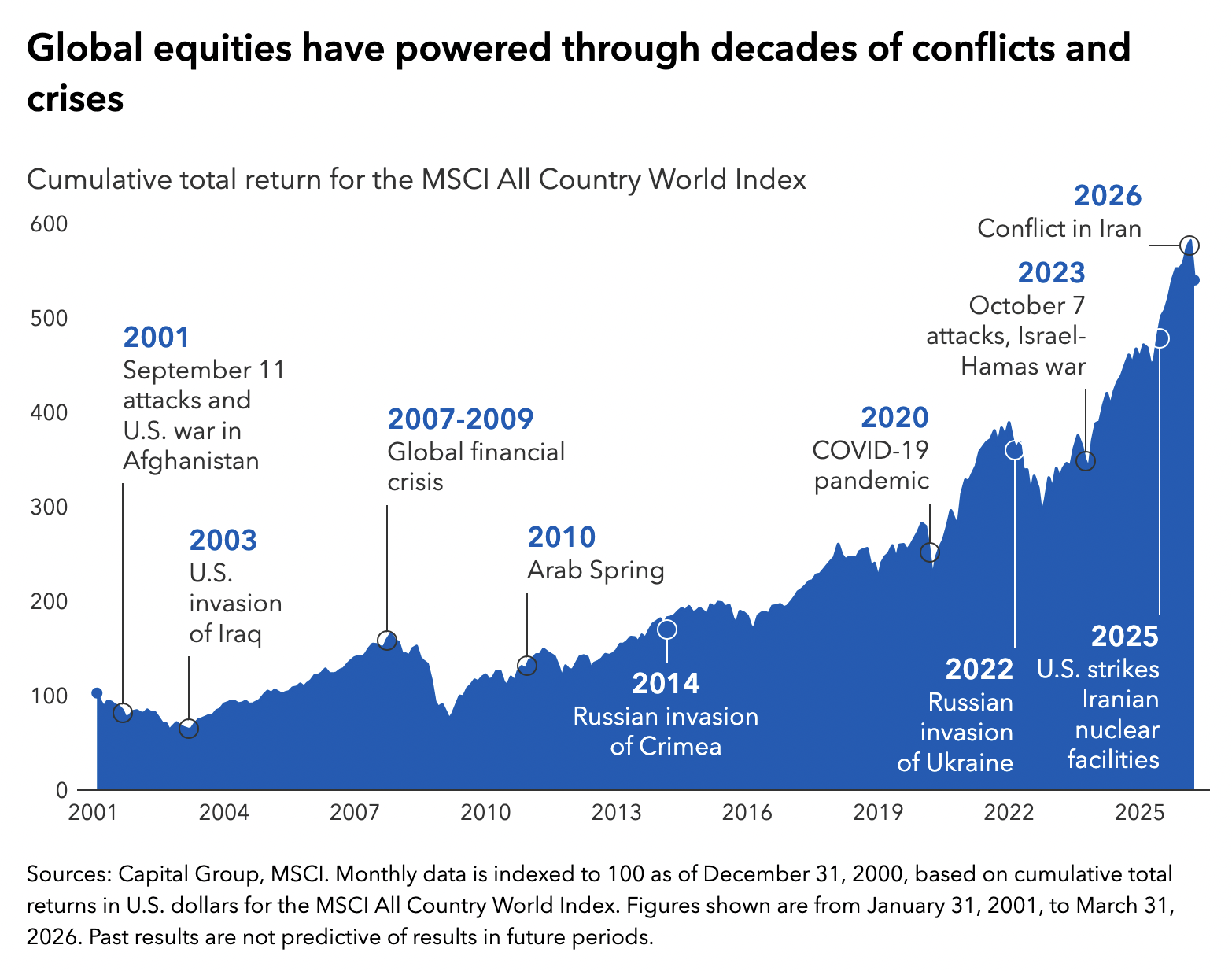

Investors are climbing a high wall of worries in 2026. With wars in the Middle East and Ukraine, messy trade disputes in the world’s major economic regions, growing fears over the impact of artificial intelligence, and deep political divisions in the United States and elsewhere, it can be difficult to remove emotions from practical investment decisions.

The war in Iran is the latest example. Each day brings a new distressing headline about a fragile ceasefire, elevated oil prices and the threat of renewed military action. The world looks terrible right now. It often looks terrible. But at times like these, I always try to remember that difficult times can also bring compelling investment opportunities for patient, long-term investors.

I’ve been in this business now for nearly 40 years, and I have counted the number of market disruptions I’ve experienced. It’s about 25, which means there has been a major event in the market, on average, every 18 months during my career. So I’m not saying be happy about bad times; I’m saying remember what they represent. Remember that they can present opportunities as share prices go on sale. And, perhaps most importantly, remember that a better day is coming.

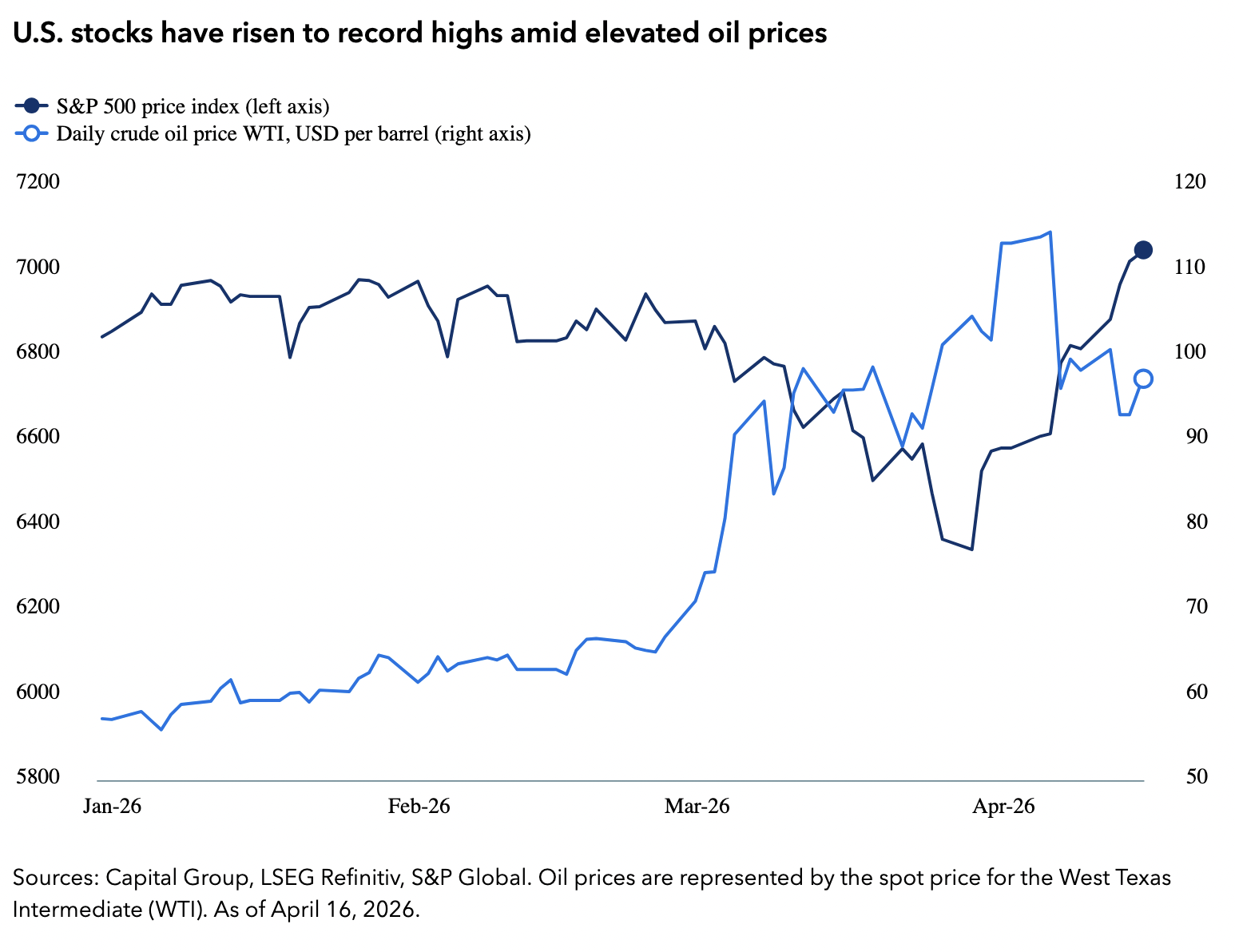

It may sound surprising given all the drama in the world, but I am cautiously optimistic about the outlook for global equities. There's a lot of negative news. There's a lot of stock market volatility. So I feel more cautious today than I did a year ago. But if the Iran conflict can be resolved soon, I think oil prices will start to trend back down. That means interest rates may also trend down. I think that will be a plus for global economic growth and for returns from global stocks. Of course, everyone hopes for a speedy end to this conflict. That is my hope. But it is also my expectation.

That expectation also appears to be reflected in U.S. stocks. Despite sharply higher oil prices since the Iran war began, the S&P 500 Index hit a new record high last week. Things could change, but for the time being, the stock market is anticipating a swift end to the hostilities. We are seeing the same message in oil futures, which are now indicating that prices should fall toward US$73 a barrel by the end of the year, roughly where they were before the U.S. and Israel attacked Iran on February 28.

Investing after the war ends

As we anxiously await the outcome of peace negotiations, I am looking ahead to the investment opportunities that may emerge as the world moves on from this conflict. In my view, international and emerging market stocks were highly attractive before the Iran war interrupted a rally in non-U.S. markets, and I think they are still attractive today. The biggest reason for that is a valuation advantage.

Even after a strong rally among non-U.S. stocks in 2025, stocks in the rest of the world are still trading at a sizable price-to-earnings discount relative to the S&P 500. Emerging markets are trading at a roughly 40% discount. So, in my view, there are real bargains outside the U.S. today, and often they can be found among companies that are world leaders in their industries. They just happen to be domiciled in other countries. They include companies like U.K.-based drug giant AstraZeneca; China-based Tencent, the largest gaming company in the world; and Taiwan Semiconductor Manufacturing Company, the world’s leading computer chip maker.

Much earlier in my career, leadership shifted back and forth between U.S. and non-U.S. stocks. It was like a game of ping-pong. I think there is a strong chance that we are headed back to that type of investment environment, where U.S. stocks lead for a while, but international and emerging market stocks also have their time to shine.

Energy sector on the rise

I am also constructive on the energy sector, which has been out of favour with investors for many years. Yes, oil companies such as ExxonMobil, Royal Dutch Shell and TotalEnergies have benefited from higher oil prices during the Iran conflict, but I find the sector attractive on a long-term basis as well.

Setting aside near-term moves in oil prices, the industry has changed its spots in recent years. There is less focus on finding new oil fields to drill and more emphasis on being thoughtful about the balance sheet, strategic about capital expenditures and serious about dividends. I am not likely to walk away from the oil industry after this conflict is over because it offers some positive attributes for long-term shareholders, not the least of which have been generous dividend payments.

I am also sifting through the artificial intelligence wreckage for companies that may have been unfairly hit by fears that easy-to-use AI applications will impair their business. Those include large software companies, such as Germany’s SAP, and companies in the online travel space, including China’s Trip.com and Spain’s Amadeus IT Group. These companies are AI enablers, in my view, not "AI roadkill"

Volatility is your friend

All the investment themes I have discussed thus far have gone through bouts of volatility, unloved by investors for one reason or another. It comes with the territory, especially if you are the type of investor, like me, who prioritizes valuations and doesn’t mind waiting for an investment to come back into favour at some point down the road. Trouble and uncertainty are fertile hunting grounds for these opportunities.

And uncertainty is always just around the corner. We may imagine a past characterized by low volatility, and great certainty, but I think if that's how you remember the past, you're probably misremembering.

Steve Watson is an equity portfolio manager with 36 years of investment industry experience (as of 12/31/25). He has an MBA and an MA in French studies from New York University as well as a bachelor's degree from the University of Massachusetts.

Copyright © Capital Group