by Jeff Buchbinder, Chief Equity Strategist, LPL Research

Additional content provided by John Lohse, CFA, AVP, Research.

July’s Consumer Price Index (CPI) report showed headline year-over-year inflation remained steady at 2.7%, below the anticipated level of 2.8%. Core inflation, which excludes more volatile food and energy prices, rose to 3.1% from a prior 2.9%, indicating underlying price pressures. The “Inflation Path” chart highlights the unchanged year-over-year print in headline CPI, and uptick in core CPI. We anticipate additional upward pressure on inflation in the coming months as the effects of recent tariffs become more evident in the data.

Inflation Path

Source: LPL Research, Bureau of Labor Statistics, Bureau of Economic Analysis 08/12/25

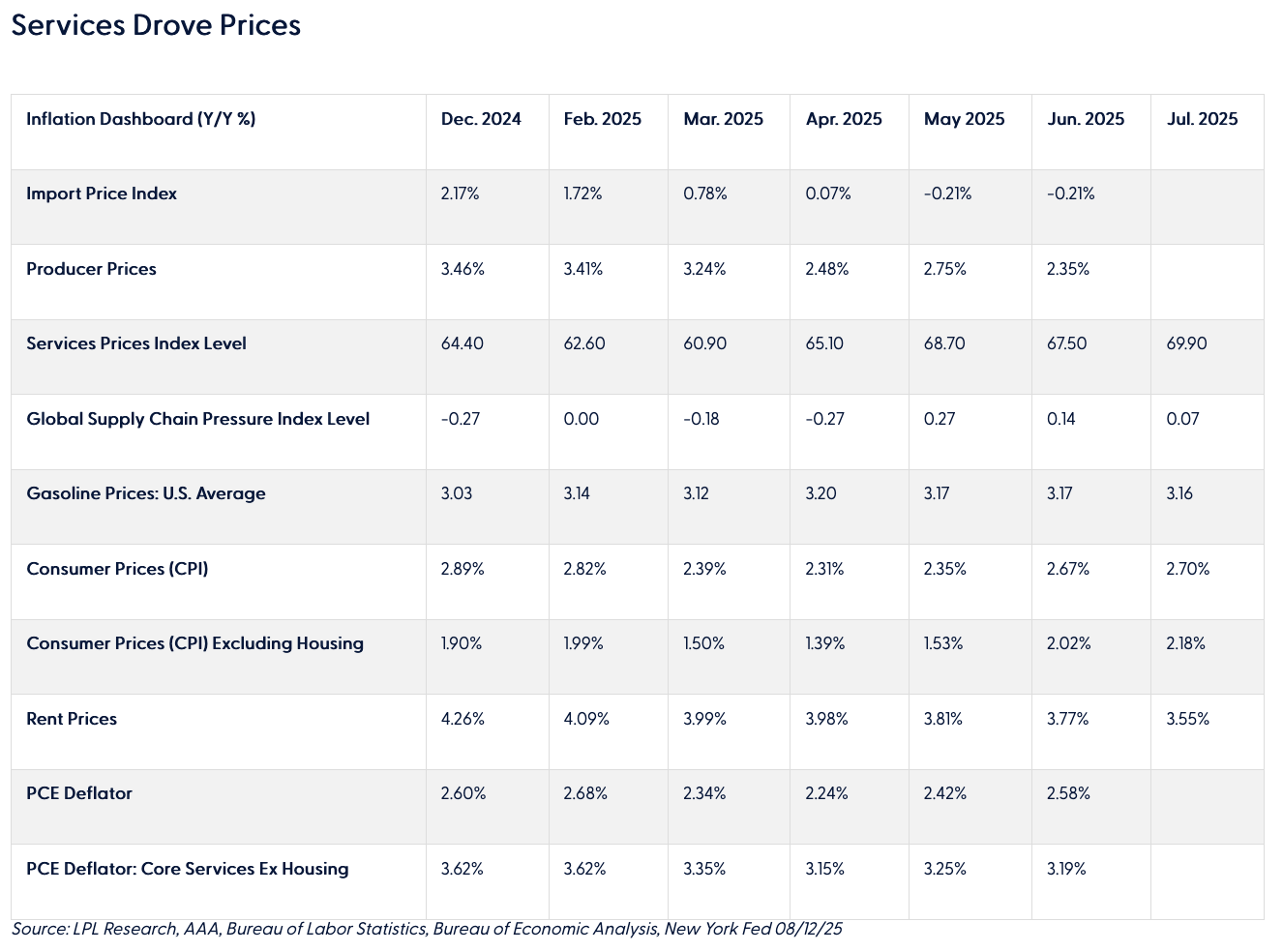

Peeling Back the Onion

Shelter costs, categorized under core services in CPI, increased by 0.2% in July and were the main contributor to the monthly rise in inflation. Medical care services, another core services component, have reached their highest level since late 2022, largely driven by rising costs for dental care and other healthcare professionals. The “Services Drove Prices” table highlights the expansion of service-level costs. On the goods side, used vehicles rose, breaking a four-month trend of outright declining prices. However, food prices experienced a slight moderation in the month-over-month increase, while energy declined.

Takeaways

The latest CPI report presented a less-than-fearsome inflation track, reinforcing expectations for a Federal Reserve (Fed) rate cut at its September meeting. This data, combined with revised employment figures showing slower job growth and rising unemployment, points to a cooling economic environment. These indicators align with the Fed’s dual mandate and suggest that further monetary tightening may no longer be necessary. In response to the CPI release, Fed Funds futures markets have now priced in a near certain 99% likelihood of a 25-basis point rate cut in September, reflecting growing confidence that the Fed has the economic justification to ease monetary policy.

Conclusion

LPL Research’s tactical asset allocation has maintained a neutral weight to equities and fixed income. On the fixed income side, yields declined across the short and intermediate parts of the curve post the CPI release, strengthening our comfort with a benchmark weight allocation.

In our recent blog, “Five Reasons to Give Small Caps Forethought”, we wrote about the ongoing quandary of small cap equities, while noting that easing of interest rates, and thus moderating borrowing costs, could provide a near-term jolt to the asset class. Following the CPI numbers on Tuesday, the Russell 2000 Index posted a 3% daily return, more than doubling the return of large cap counterpart indexes. Currently, over a tactical time frame of up to one year, we maintain a neutral weight to small cap growth and an underweight to small cap value, as potential economic weakness can prove to be a headwind. For shorter-term traders in search of someplace else to go beyond the Magnificent Seven-heavy large caps, this latest small cap bounce could have a bit more juice left.

Overall, we don’t expect a complete dissipation of inflation pressure. Our expectation is tariff impacts will increasingly show up in the data in the months ahead. We will be closely monitoring the final bearer of those costs to determine how much margin compression companies allow and how much of those additional costs are passed along to consumers. For now, we believe the Fed has what it needs — a softening labor market and only modest inflation surprises — to support the first rate cut of the year.

Copyright © LPL Research

*****

Important Disclosures

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk.

Indexes are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

This material was prepared by LPL Financial, LLC. All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

Asset Class Disclosures –

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

Bonds are subject to market and interest rate risk if sold prior to maturity.

Municipal bonds are subject and market and interest rate risk and potentially capital gains tax if sold prior to maturity. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply.

Preferred stock dividends are paid at the discretion of the issuing company. Preferred stocks are subject to interest rate and credit risk. They may be subject to a call features.

Alternative investments may not be suitable for all investors and involve special risks such as leveraging the investment, potential adverse market forces, regulatory changes and potentially illiquidity. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

Mortgage backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

High yield/junk bonds (grade BB or below) are below investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

Precious metal investing involves greater fluctuation and potential for losses.

The fast price swings of commodities will result in significant volatility in an investor's holdings.

This research material has been prepared by LPL Financial LLC.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Deposits or Obligations | Not Bank/Credit Union Guaranteed | May Lose Value

For Public Use – Tracking: #783297