Clarity from the phase-one trade deal with China and United Kingdom election results could help shift stock market performance drivers more toward investing fundamentals in 2020. We expect stocks to appreciate in line with earnings growth next year, which justifies benchmark-like equity allocations in our view.

CLARITY ON TRADE AND BUSINESS INVESTMENT

In 2019, expanding valuations drove gains for stocks; in 2020, we expect earnings to do the heavy lifting. Better clarity on trade may help drive increased business spending and more productivity, which we think will lead to stronger earnings growth in 2020. We are encouraged by the additional clarity companies now have as a result of the trade pact reached with China December 13.

In 2019, expanding valuations drove gains for stocks; in 2020, we expect earnings to do the heavy lifting. Better clarity on trade may help drive increased business spending and more productivity, which we think will lead to stronger earnings growth in 2020. We are encouraged by the additional clarity companies now have as a result of the trade pact reached with China December 13.

We expect prospects for better earnings growth in 2020 to help support stocks at current valuations, as noted in our 2020 Outlook publication released earlier this month. Our 2020 year-end fair value target range for the S&P 500 Index is 3,250–3,300, which we base on a trailing price-to-earnings ratio (P/E) of 18.75 multiplied by our 2020 S&P 500 earnings per share forecast of $175. We believe mild inflation and still-low interest rates support these valuations, but we are not factoring in any expansion in stock valuations next year. Stocks are already near the low end of a range that we would consider fair value based on our 2020 earnings forecast. As a result, we would not consider adding equities to allocations already in line with appropriate benchmarks.

EARNINGS ARE KEY TO ADDITIONAL UPSIDE IN 2020

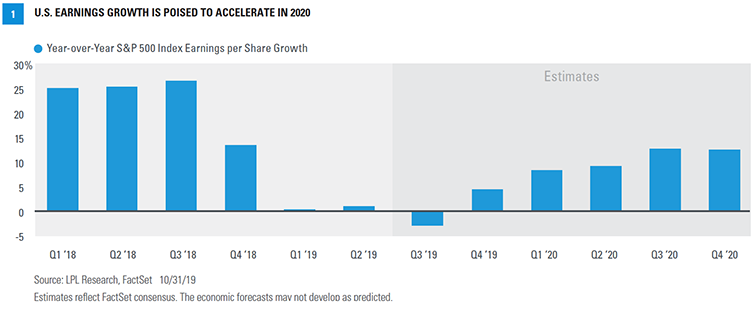

Corporate earnings growth has slowed considerably in 2019, as shown in [FIGURE 1]. The impact of the 2018 tax cuts created a difficult year-over-year comparison, global economic growth slowed, and tariffs and trade uncertainty weighed.

In 2020, we believe a pickup in earnings growth will be the biggest key to potentially pushing stocks beyond our fair value range, which is now only 3–4% away from December 20’s closing price. Aided by the recent trade truce with China, U.S. economic growth in 2020 may exceed our 1.75% forecast. Assuming the U.S.-China trade truce holds, we would anticipate better economic growth and stronger revenue and earnings growth for corporate America.

Improved clarity on trade makes forecasting economic growth and earnings for 2020 a bit easier, but the geopolitical environment still presents challenges. China trade tensions could flare up again as the countries work on a tougher “phase two” deal covering more contentious issues. The United Kingdom’s exit from the European Union (Brexit) may not be smooth, despite the convincing election win for Boris Johnson’s Conservative Party.

Our earnings estimate for 2020, which represents a mid-single-digit increase from our 2019 estimate, had already assumed some progress on trade. If we see a pickup in capital spending and improved productivity as a result of reduced tariff barriers and less trade uncertainty, we could potentially see some upside to that $175 number.

EQUITY ASSET ALLOCATION

Geographically, the United States and emerging markets still stand out to us as relatively more attractive investment opportunities than developed international markets, based in large part on relatively stronger outlooks for economic growth and corporate profits.

Emerging Markets. Earnings for the MSCI Emerging Markets Index are expected to rebound solidly in 2020, with the consensus estimate (FactSet) calling for a 14% increase. That pace is nearly triple the forecast for Japan (5%) and ahead of Europe (9%) and the United States (10%). A possible double-digit increase in emerging markets’ earnings could be attractive to global investors, which may be a more likely scenario following the China trade deal. Disappointing earnings growth in these regions in recent years remains a concern, but we still believe a modest allocation to emerging markets equity makes sense in appropriate strategies. We are encouraged by the recent uptick in emerging markets’ earnings estimates and evidence of stabilizing global economic growth.

Developed International. Our concerns about global policies, economic growth, and interest rates drive our cautious outlook for developed international equities. Despite relatively attractive valuations, we see a number of challenges in developed markets that leads us to maintain our tactical underweight to the asset class. With the impact of any further monetary policy support likely to be muted, a coordinated move toward pro-growth fiscal policy would be needed for us to become more bullish on these regions. As a result, we would recommend that tactical investors consider focusing the majority of their equities allocations here at home.

Equity Positioning. Within U.S. equities allocations, we recommend a balance of the growth and value styles, with an emphasis on large cap stocks over their small cap counterparts as the business cycle moves into its latter stages.

We continue to prefer cyclical sectors as the U.S. economic expansion continues, and technology still leads this bull market. We expect industrials to benefit from a potential pickup in capital spending due to ebbing trade tensions. The challenging interest-rate environment prevents us from a more positive view of the financials sector for now, though we are encouraged by the recent steepening (un-inversion) of the yield curve, as long-term U.S. Treasury yields have risen faster than short-term Treasury yields in recent months. Finally, we are watching the healthcare sector for a potential upgrade due to the possibility that sector valuations reflect an overly pessimistic post-election policy environment.

Read previous editions of Weekly Market Commentary on lpl.com at News & Media.

OUTLOOK 2020

For more investment insights, read our newly released Outlook 2020: Bringing Markets Into Focus.

WEEKLY MARKET PERFORMANCE REPORT

Please see our new Weekly Market Performance report with insights on major asset classes.

John Lynch, Chief Investment Strategist, LPL Financial

Jeffrey Buchbinder, CFA, Equity Strategist, LPL Financial

______________________________________________________________________________________________

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results.

The economic forecasts set forth in this material may not develop as predicted.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk in all market environments.

International debt securities involve special additional risks. These risks include, but are not limited to, currency risk, geopolitical and regulatory risk, and risk associated with varying settlement standards. These risks are often heightened for investments in emerging markets.

Because of their narrow focus, sector investing will be subject to greater volatility than investing more broadly across many sectors and companies.

All indexes are unmanaged and cannot be invested into directly. Unmanaged index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investment.

All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

DEFINITIONS

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio.

Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability. Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio.

This research material has been prepared by LPL Financial LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL is not an affiliate of and makes no representation with respect to such entity.

If your advisor is located at a bank or credit union, please note that the bank/credit union is not registered as a broker-dealer or investment advisor. Registered representatives of LPL may also be employees of the bank/credit union. These products and services are being offered through LPL or its affiliates, which are separate entities from, and not affiliates of, the bank/credit union. Securities and insurance offered through LPL or its affiliates are: