by AdvisorAnalyst.com Editorial Team

Raoul Pal opens with a diagnosis most working professionals feel but few can articulate. "You earn more than your parents did, you work at least as hard, and somehow you are further behind than they were at your age," he writes. The evidence is stark: the median American can buy 89% less of the S&P 500 than in 1980, and 26% less housing. Pal's message is that this is not personal failure. "There is a force underneath this, and once you see it all in one place you can't unsee it."

That force is what Pal, drawing on twenty one years of monthly research at Global Macro Investor, calls the Everything Code, a single framework that he argues explains why savings lose value and why the gap between asset owners and wage earners keeps widening.

The Wrong Target

Pal's first move is to dismantle the conventional benchmark. Investors are taught to beat inflation, the 2 to 3% rise in the cost of a basket of goods. But inflation "only tells you about the cost of living. It tells you nothing about the cost of getting ahead." The number that decides whether wealth compounds or erodes is debasement, "the rate at which the money itself is being devalued." Pal puts that figure closer to 8% annually. A savings account paying 4% "looks like a gain but it is really a loss." Stack roughly 3% inflation on top and "the real hurdle is closer to 11% a year."

Two Engines Stalled, One Trap Remaining

The origin of that 8% lies in the arithmetic of growth. GDP growth equals population growth plus productivity growth plus debt growth. For most of modern history, the first two carried the load. No longer. "Demographics, as a driver are dead. Productivity is falling. Which leaves debt doing almost all of it." Underlying growth has fallen from about 5% to 1.8%.

The demographic problem is unfixable on any policy timeline. Roughly 4 million Americans will retire each year for the rest of the decade, while the US birth rate has sat below replacement since 2007, now near 1.6 against the 2.1 needed. "You cannot fix that by trying harder, because the workers you would need were supposed to be born twenty years ago and they simply weren't." The aging population simultaneously suppresses output per head, dragging productivity down with the workforce.

The Debt Machine and Its Timer

Pal traces the structural break to 2008. Governments absorbed enormous debt bailing out the banking system, then cut rates to zero because the system could not afford interest at normal levels. Crucially, "the government never paid anything back. They just kept rolling the debt in one big refinancing cycle." In his phrase, they "used their credit card to pay the interest on their credit card," compounding debt exponentially.

That decision put the economy on a clock. Debt refinances on a schedule, stretched borrowers break, central banks cut and inject liquidity, and the cycle resets. Historically about four years, the cycle has extended toward six as governments lengthened maturities after 2022. The implication is uncomfortable but clear: "Low interest rates are a feature, not a bug. We cannot survive without them."

Quantitative easing is the mechanism that keeps it running. Since 2009, US government debt has grown roughly $10 trillion faster than nominal GDP, and liquidity rises in lockstep to service it. When money creation outruns a barely growing economy, each unit of currency is worth less. "That is debasement."

Why Value Investing Broke

Here Pal delivers his most provocative claim for portfolio construction: "97% of the movements in the US stock market can be explained by global liquidity." Debasement lifts scarce assets, but earnings only track M2 growth, which lags balance sheet expansion. The difference shows up as multiple expansion. "P/Es are not valuations anymore but monetary indicators. You need to understand this, or you will lose money. This is why value investing no longer works."

Adjusted for debasement, most conventional assets collapse to breakeven. Gold "has preserved purchasing power beautifully. But preservation is not growth." Real estate, bonds, and diversified pensions feel like gains only because the measuring stick keeps shrinking. Only two asset classes have consistently cleared the hurdle: technology stocks and crypto, both driven by network adoption compounding on top of the debasement tailwind.

A Map, Not Just a Diagnosis

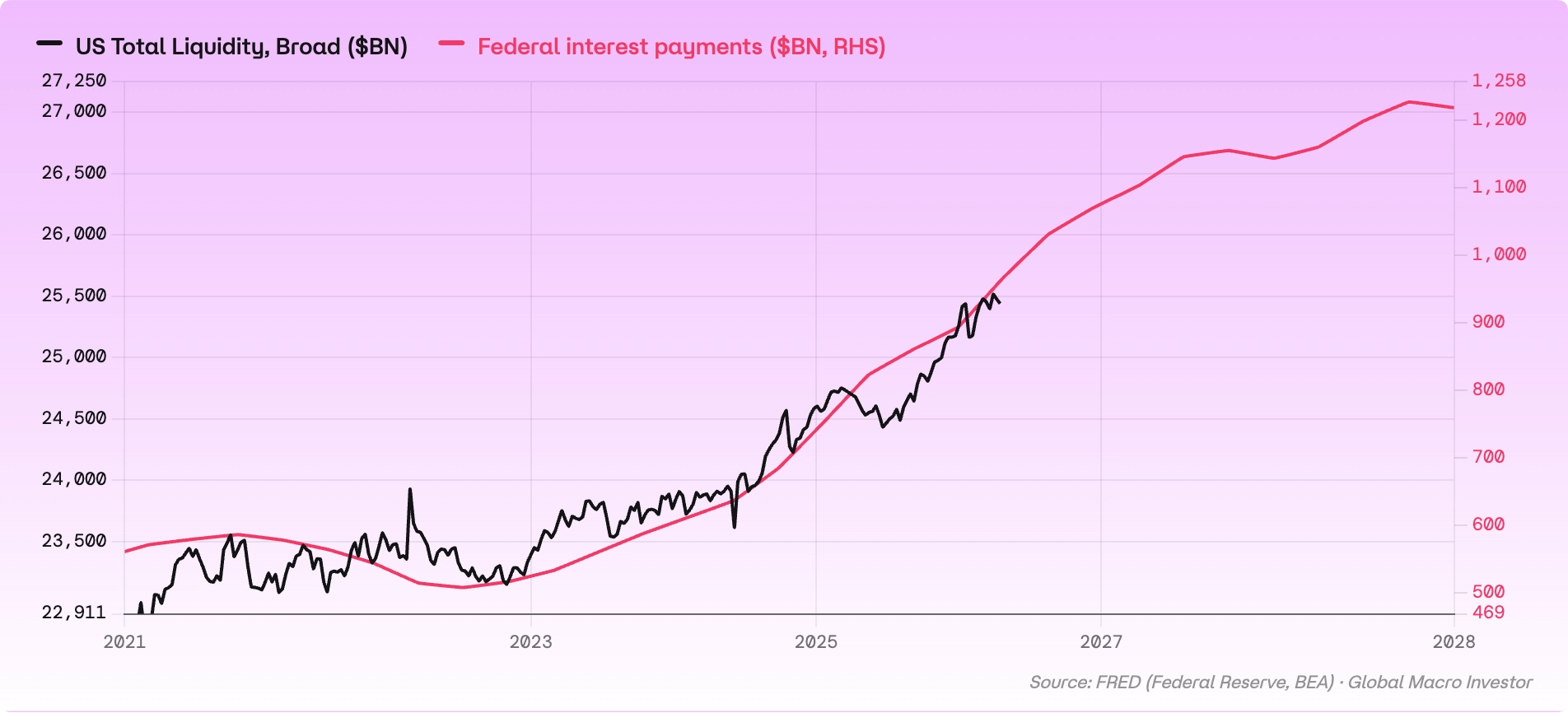

The framework's forecasting power rests on a lead-lag relationship. Interest payments on existing debt are already known, and they lead liquidity by roughly three years. Because liquidity explains most equity returns, "asset prices themselves can be forecast." Pal's projected path runs through 2028.

The endgame, he argues, is yield curve control, already trialled by Japan and used by the US after World War II, when capped rates and 5% GDP growth shrank the Fed balance sheet relative to output while equities rose 750% in a decade. The bridge to resolution is the productivity wave he calls the Exponential Age: AI, robotics, energy, and automation. "Strap in. It's going to go bananas."

Five Key Takeaways for Advisors and Investors

- Benchmark portfolios against debasement, not CPI. Pal's hurdle rate is roughly 11% annually once 8% debasement and 3% inflation are combined, which reframes what "keeping up" actually requires.

- Cash is a structurally losing position. Pal describes it as "a melting ice cube," making strategic allocation to assets that cannot be printed a core, not tactical, decision.

- Liquidity is the dominant return driver. With 97% of US equity movements explained by global liquidity, monetary conditions may matter more than fundamentals in client conversations about valuation.

- Rising P/E ratios reflect monetary conditions, not overvaluation, in Pal's framework, which challenges traditional value discipline and mean reversion assumptions.

- The debt refinancing cycle, now roughly six years, offers a forecastable rhythm, with known interest payments leading liquidity by about three years through 2028.

Footnote:

Pal, Raoul. "The Everything Code." Global Macro Investor / raoulpal.com, 7 July 2026.