by Russ Koesterich, CFA, JD, Portfolio Manager, BlackRock

Key Takeaways

- Equities advanced in April, but hedges remain few and far between, as traditional risk mitigants like bonds and gold continue to show a correlation with stocks.

- In the meantime, energy prices surged earlier in the conflict as the stock market declined, and while paring some gains in April, energy names have more recently been keeping up with the broader market.

- It’s important to keep in mind that while energy stocks are currently providing investors with much-needed diversification, the market will likely shift when recession fears start to emerge.

Investors have learned to look past the ongoing war in Iran and surge in energy prices. Stocks have not only recovered but have marked new highs.

In my last post, I suggested that stocks could get past a temporary conflict based on the strength of the economy, U.S. energy independence and the diminishing wallet-share dedicated to energy. I still believe equities can continue to advance, but with markets 12% above the March lows, it’s worth spending a moment on how to hedge gains. In this case, the obvious candidate is probably the right one: own more energy stocks.

Bonds & Gold: No Protection

Before discussing what is working, it is worth highlighting what isn’t. Two traditional portfolio hedges, bonds and gold, are having a tough time. Since the start of the conflict, real 10-year yields, derived from the TIPS market, have risen approximately 0.25%. Not only have yields risen, but on a day-to-day basis, bonds are increasingly moving with stocks. Since the start of the war, the S&P 500 and long duration bonds have had a 0.45 correlation. Rather than mitigating risk, owning bonds has compounded it as investors increasingly worry about the pass-through impact of higher oil to broader inflation.

Gold has performed even worse. Prices have dropped roughly -13%, with the stock/gold correlation rising to approximately 0.50. Here the relationship is a little less intuitive. While gold is often thought of as a hedge against geopolitical uncertainty, as an asset with no cash flow it is also highly sensitive to interest rates, particularly real rates. With rates rising and gold having previously enjoyed a historic run, rising more than 50% from late August through the end of February, investors have been selling gold to de-risk portfolios.

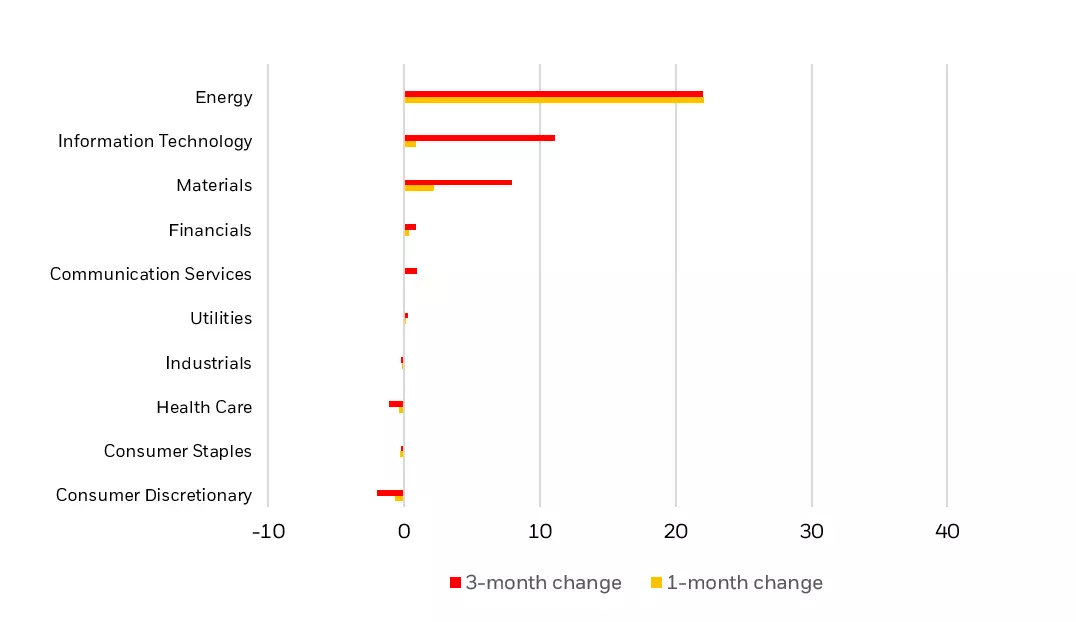

Oil earnings surging

While traditional hedges have not worked, energy stocks have held up much better. From the start of the conflict to the April ‘ceasefire’, the energy sector gained roughly 7.5%, versus around a -4% decline for the broader market. While energy stocks surrendered much of their gains in April, more recently they have been keeping up with the equity rebound. The reason: a surge in earning momentum (see Chart 1). With oil prices higher for longer, earnings momentum is likely to continue.

Shift when recession fears start to emerge

There is one important caveat to adding energy stocks. If the blockade and supply interruption lasts long enough, concern will shift from inflation to recession. At that time, energy stocks, which benefit from a strong economy and demand for oil, may start to underperform and market dynamics will likely shift to bonds being the better hedge. But in the near term, and assuming no quick resolution to the conflict, energy stocks are likely to prove the rare diversifying asset.

Copyright © BlackRock