by Craig Basinger, Derek Benedet, Brett Gustafson & Spencer Morgan, Purpose Investments

These markets are awe-inspiring and so much fun. Any angst over the Strait of Hormuz global logistics blockage (which is still closed) has faded and been replaced with another round of AI euphoria. This bout has been more focused on memory and semiconductors, turbo-boosting many markets that carry higher weights to those industries. Q1 earnings weren’t just technology-driven, growth was widespread with most sectors pace in double digits. The global economy is pretty good with a manufacturing upswing. There is a lot of good news, but today we are taking a step back from the recent excitement to get a better look at things.

This is late cycle. We are big fans of the market cycle, with our framework of indicators and research into past cycles. And the preponderance of data points to late cycle. Let’s stack them up:

Bubblicious market performance: Few would disagree that equity market returns have gone a bit nutty, in a good way. S&P 500 having a 20% year feels like the norm now. The TSX just posted a 35% year. Global equity markets have risen about $26 trillion over the past year to $127 trillion. And of course, we can slice more narrowly to look huge returns in semiconductors, memory, or anything selling into the AI infrastructure build.

The Roundhill Memory ETF was launched on April 2, and it holds a basket of about 10 companies in the memory space, of which there is a shortage. This ETF has almost reached $10 billion in assets in ONLY 42 days. The SOX index, which tracks a basket of semiconductor companies, is up 67% during the past six weeks. Or let’s pick on Cisco, since they were around in the last tech bubble and we own this name in a few strategies. After an earnings boost from blockbuster sales to hyperscalers, stock jumped 15% last Thursday to reach an 84% rise over the past year. Great quarter but earnings growth in 2026 is up about +14% and estimates for 2027 are for another +13%. Estimates will come up but 84% price gain vs. 13% earnings gain is hard to reconcile regardless of how much of an AI bull you are.

Global market capitalization is now $164 trillion, up a solid $13 trillion so far this year as of only mid May. With big value creation in some very narrow pockets, evident in the narrow breadth of the recent advance. This is late cycle performance.

Inflation/yields/rates: What else is supposed to happen in the very late stage of the market cycle? Inflation, higher yields and higher rates. As the cycle ages, aggregate demand starts bumping up against capacity, causing inflation and yields to rise. Then, central banks are supposed to raise rates with the hopes of cooling aggregate demand and alleviating inflation pressures. Their timing is often terrible and the cycle ends.

OK, we have inflation rising again. We could blame the Strait of Hormuz blockage, certainly a big contributor, but there are many factors at play here. That soft labour market in the U.S. has been firming up. China, historically an exporter of disinflation, now has a PPI well in the positive territory. And all that spending on data centers is pushing prices way up in many categories. Have no doubt AI will enhance productivity, which will be disinflationary, but getting there is very inflationary. Meanwhile resource companies, known to be late cycle strong performers, are going great.

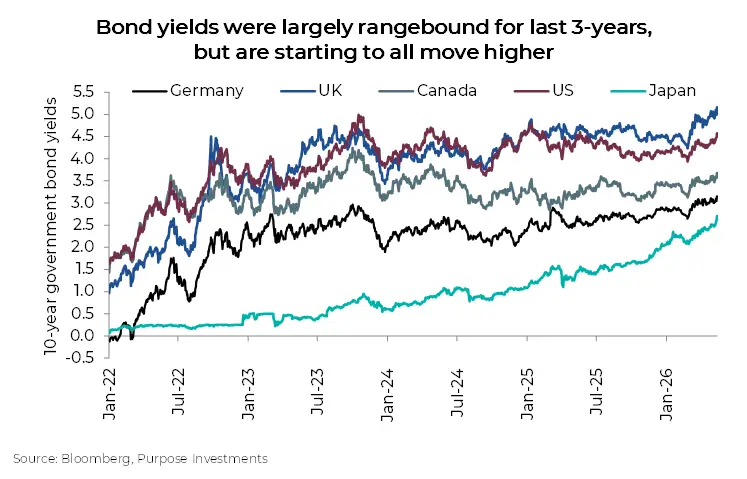

Now this is starting to lift bond yields. After yields normalized in 2022-23 (doesn’t that make it sound so much less painful that it actually was?), they have remained rangebound for the past three years. They are starting to stir. Inflation, higher inflation, large corporate bond issuances, the list of factors putting upward pressure on yields is a long one. At some point, equity markets will care about yields moving higher. Maybe we got a whiff of that last week.

Add it all up. Commodity prices up, incredible spending on AI build out, more companies/countries focusing on supply chain diversification and holding higher inventories (due to disruptions), manufacturing doing well globally, low unemployment – all pushing inflation higher and yields up.

So, where is monetary policy? Rate cuts increasingly appear off the table (duh), and they probably should already be hiking. But policy has become more about elongating cycles and less about maintaining price stability. So, the policy mistake is probably not raising rates and the continued unbridled fiscal stimulus avalanche even with economies doing fine.

A game changer: This would be AI. Every cycle has one or a few things going on late in the cycle that is changing the world in a meaningful way. The Nifty 50 in the late 1960s into early 1970s, it was new technologies and companies increasingly going global. The 1980s cycle was lifted by leveraged buyouts and deregulation, plus Japan taking over the world (economically). The 1990s of course was dot-com. The early 2000s it was China’s growth driving commodities and the explosion in housing. In the 2010s it was the rise of corporate debt and fall in yields.

AI certainly fits the bill as a technology that will change many parts of society and has a number of meaningful economic impacts. Even if it doesn’t live up to all the productivity gains or ROI expected (not our view, we said ‘if’), the infrastructure buildout itself is enough to drive the economy.

Late Cycle

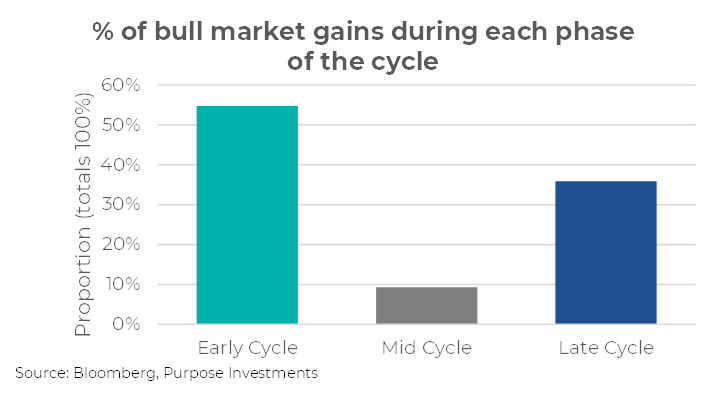

The good news, if it is late cycle there are only a few economic cracks and certainly manageable. Even higher yields, which may upset the market, as long as economic growth continues, earnings grow, AI excitement continues, markets can handle it. The dot-com cycle handled 10-year U.S. Treasury yields in the 6-7% range. The housing cycle in the early 2000s handled yields of 5%, with housing very sensitive to financing costs. Plus, the late cycle phase is also characterized by strong price gains. Not as much as the early cycle phase, coming off the previous bear market bottom, but strong returns nonetheless.

Our favourite analogy is the bull and bear have started to fight it out. This phase has bigger market swings, both up and down as the conflict continues. Spoiler alert, the bear wins with the consequential question being how long will the fight last. This is where we think we are in the cycle.

Last Dance Implications

If memory serves, the Last Dance is characterized by a longer song with slower music. The good news is the music is still playing, and the pace of the music has not slowed too much. And it is always possible there will be an encore as those policymakers remain emboldened about trying to elongate cycles, regardless of the impact on prices, income disparity or other side effects.

The trigger that marks the end of a cycle is pretty different every time. A few potential triggers that we are watching increasingly more closely include:

1) If some highfliers start to miss very high earnings expectations.

2) Rates, or more likely bond yields rising too much. Inflation would lead to this too.

3) The weight of it all. Sometimes cycles end because the winners simply become too big to support their own weight.

Or something new that is different than any past cycle.

From a portfolio perspective, you should keep in mind that over the past few years many clients have enjoyed outsized returns. Many are likely well above their financial plan flight path. Even with the music still playing, not crazy to de-risk a bit. We are still dancing but have a moderately defensive tilt. Trying not to leave the dance early, but we endeavour not to miss curfew.

— Craig Basinger at Purpose Investments.

Get the latest market insights in your inbox every week.

Copyright © Purpose Investments

Sources: Charts are sourced to Bloomberg L.P.

The content of this document is for informational purposes only and is not being provided in the context of an offering of any securities described herein, nor is it a recommendation or solicitation to buy, hold or sell any security. The information is not investment advice, nor is it tailored to the needs or circumstances of any investor. Information contained in this document is not, and under no circumstances is it to be construed as, an offering memorandum, prospectus, advertisement or public offering of securities. No securities commission or similar regulatory authority has reviewed this document, and any representation to the contrary is an offence. Information contained in this document is believed to be accurate and reliable; however, we cannot guarantee that it is complete or current at all times. The information provided is subject to change without notice.

Commissions, trailing commissions, management fees and expenses all may be associated with investment funds. Please read the prospectus before investing. If the securities are purchased or sold on a stock exchange, you may pay more or receive less than the current net asset value. Investment funds are not guaranteed; their values change frequently, and past performance may not be repeated.

Certain statements in this document are forward-looking. Forward-looking statements (“FLS”) are statements that are predictive in nature, depend on or refer to future events or conditions, or that include words such as “may,” “will,” “should,” “could,” “expect,” “anticipate,” “intend,” “plan,” “believe,” “estimate,” or other similar expressions. Statements that look forward in time or include anything other than historical information are subject to risks and uncertainties, and actual results, actions, or events could differ materially from those set forth in the FLS. FLS are not guarantees of future performance and are, by their nature, based on numerous assumptions. Although the FLS contained in this document are based upon what Purpose Investments and the portfolio manager believe to be reasonable assumptions, Purpose Investments and the portfolio manager cannot assure that actual results will be consistent with these FLS. The reader is cautioned to consider the FLS carefully and not to place undue reliance on them. Unless required by applicable law, it is not undertaken, and is specifically disclaimed, that there is any intention or obligation to update or revise FLS, whether as a result of new information, future events, or otherwise.