by Vaibhav Tandon, Senior Economist, Nothern Trust

t is said that when one door closes, another one opens. China is very much hoping that this proverb continues to hold true.

One call where many forecasters (ourselves included) went wrong last year was our expectation that China’s exports would suffer under the new U.S. tariff regime. That view placed too much weight on the presumed bite of tariffs and too little on the ability of Chinese producers to adapt, redirect and reprice output to alternate destinations.

China’s exports have proven to be remarkably resilient, one of the few upsides for an otherwise ailing Chinese economy last year. Rather than compress China’s export footprint, heightened trade barriers have redirected it, both geographically and along the value chain.

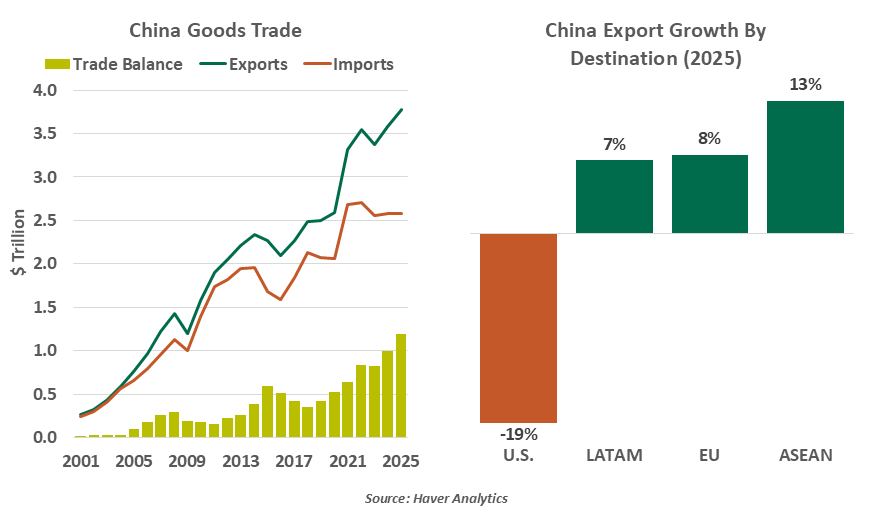

China closed the year with a record goods trade surplus of $1.2 trillion, crossing the trillion-dollar mark for the first time. Tariffs did bite in one place: shipments to the United States fell roughly 20% in 2025, but the lost ground was more than made up elsewhere. With the scale and composition of exports to the United States and Europe broadly similar, the European Union (EU) emerged an obvious alternative. For the first time, China’s trade surplus with the EU in 2025 exceeded its surplus with the United States. Exports to the Association of Southeast Asian Nations rose about 13%, to Africa 26% and by around 8% each to the EU and Latin America last year.

The composition of exports is changing as well. China’s shipments to other countries have been increasingly driven by industrial inputs and capital‑intensive goods rather than low-value consumer products. Integrated circuits and “new economy” manufacturers have been important contributors, with EV shipments alone increasing 70% over 2024.

Transshipment has been a key workaround for China. It is a central concern for Washington, which levied a 40% duty on goods deemed to be rerouted to evade American tariffs. The U.S. administration complemented that with a sharper enforcement posture, including a Trade Fraud Task Force and broad investigations focused on Southeast Asian routing hubs.

Yet the framework to restrict rerouting remains incomplete. The U.S. administration has yet to clearly define what constitutes illegal transshipment, or to specify thresholds for Chinese content that would trigger higher levies. That ambiguity complicates compliance and leaves space for continued trade rerouting.

As Chinese goods flood into alternative destinations and competitive pressures move beyond basic manufacturing, the scrutiny has widened well beyond Washington.

Tariffs changed where China exported, not whether it did.

Europe is sharpening its focus on dumping: the risk that China is selling goods at below-market prices to harm domestic producers. Brussels is considering a minimum price system for Chinese electric vehicles as an alternative to import tariffs. From July 2026, the EU will remove the €150 de minimis customs duty exemption for imported goods.

Mexico is becoming even more watchful, reflecting a mix of domestic industrial protection and alignment with U.S. trade priorities ahead of the United States-Mexico-Canada Agreement review in mid-2026. Mexico has increased its use of trade‑remedy tools. Last year, it initiated 11 antidumping investigations against Chinese goods, nearly double the number in 2023. In December 2025, Mexico approved broad tariffs of up to 50% on hundreds of products from countries without Mexican free trade agreements, with China the primary target.

Signaling awareness of the growing external scrutiny, Chinese authorities have announced the cancellation and phased elimination of tax rebates for selected products beginning in April 2026. Moves like this may ease external optics, but they do not address the core constraint: weak domestic demand.

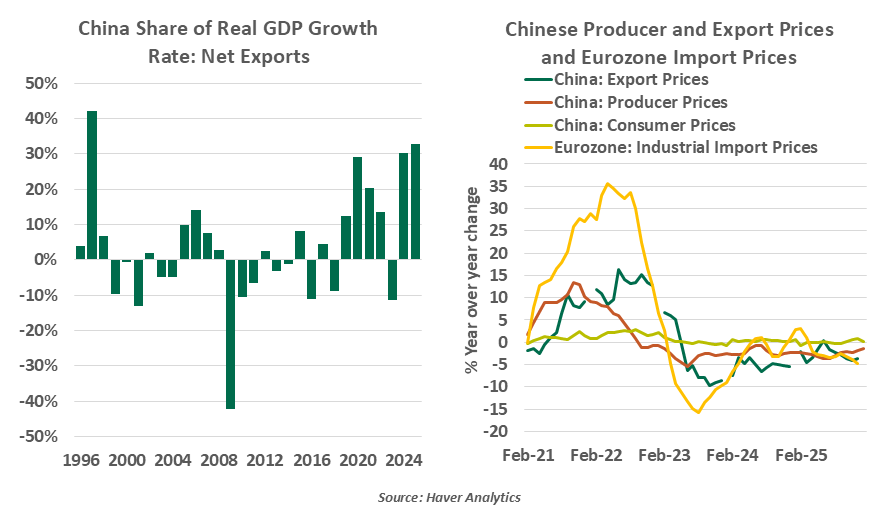

The external sector has shouldered a disproportionate share of China’s growth burden. Net exports accounted for one-third of economic growth in 2025, the highest contribution since the late 1990s. Persistent excess capacity and deflationary pressures at home have pushed firms to compete more aggressively abroad. Export and producer price deflation have been markedly deeper than consumer price deflation since 2023; China’s weak price pressures are being transmitted to other markets through external trade.

This is further reflected in shrinking profit margins of Chinese producers and a rising share of loss-making firms in manufacturing, which has doubled from 15% in 2018 to 31% last year. The result is a transmission of goods price disinflation to partners such as Europe. While lower imported inflation can benefit consumers, it can also compress domestic margins and weaken pricing power.

China can reroute exports, but it cannot reroute the mounting scrutiny.

Countries like Canada and the U.K. are seeking to diversify trade by engaging with China. That suggests there may still be legs left in China’s export streak. But greater scrutiny, combined with U.S. pressure on partners to close circumvention routes, could narrow the set of destinations willing to absorb China’s surpluses. The more that happens, the starker Beijing’s trade-off becomes: tolerate slower growth or lean harder on exports.

Tariffs altered the geography of China’s shipments, but not their volume. The question going forward is how long the rest of the world is willing to keep absorbing the resulting displacement and disinflation. The doors to continued Chinese export growth may be closing.

Copyright © Nothern Trust