by George Smith, Portfolio Strategist, LPL Research

"Sell in May and go away" is an old market adage, popularized by the Stock Trader's Almanac,revealing the best six months of the year for stocks (they used the Dow Index) occurred from November through April. It suggested investors should sell in May and wait until November to buy back into the markets. We explore if the seasonality data still supports this strategy and other clues seasonality could give us about markets for the remainder of 2024.

April seems set to break a streak of five positive months for stocks, as measured by the S&P 500, that stretched from November through March. Based on seasonality, this year’s negative April was a disappointment as April has been one of the stronger months over all time periods studied, ranking as the second-best month for stocks since 1950 (November has been the strongest). April’s negative return would only be the fourth for the month in the last 20 years, and only the second in the last 10 years (the other came in 2022).

Analyzing May’s seasonals, it has historically been one of the weaker months. Returns have been marginally positive (0.2%) on average over all years since 1950, and over the past 10 years the average has improved slightly to 0.7%. Over the past five years, May returns have been negative (-0.2%) and rank 10th for average returns, with only February and September worse, perhaps giving some credence to the “Sell in May” part of the phrase at least.

After a Disappointing April, May Seasonals Are Also Weak

S&P 500 Index Average Monthly Returns (1950–2024)

Source: LPL Research, FactSet, Bloomberg 04/29/24 (1950–current)

Disclosures: All indexes are unmanaged and cannot be invested in directly. Past performance is no guarantee of future results.

The modern design of the S&P 500 Index was first launched in 1957. Performance before then incorporates the performance of its predecessor index, the S&P 90.

When considering seasonals over longer time frames that align with the “go away” period, the May–October six-month period is indeed the weakest of all such periods since 1950, as well as over the last five and 20 years. Over the past 10 years, it ranks seventh. July and October have been historically stronger months during this six-month window, but it is dragged down by September, which ranks dead last of all months over all the periods studied. September has a long term average return of -0.7%, while returns have been fairly flat in May, June, and August. Even so, unless investors can seek superior returns in other asset classes, being out of the equity market may not have been the best strategy, with stocks still delivering positive six-month returns, on average, over all the May–October periods studied (1.8% since 1950, and closer to 4.4% over both the past five and 10 years).

Sell in May? May–October, the Weakest Six-Month Return Window Since 1950

S&P 500 Index Average Six-Month Returns (1950–2024)

Source: LPL Research, FactSet, Bloomberg 04/29/24 (1950–current)

Disclosures: All indexes are unmanaged and cannot be invested in directly. Past performance is no guarantee of future results.

The modern design of the S&P 500 Index was first launched in 1957. Performance before then incorporates the performance of its predecessor index, the S&P 90.

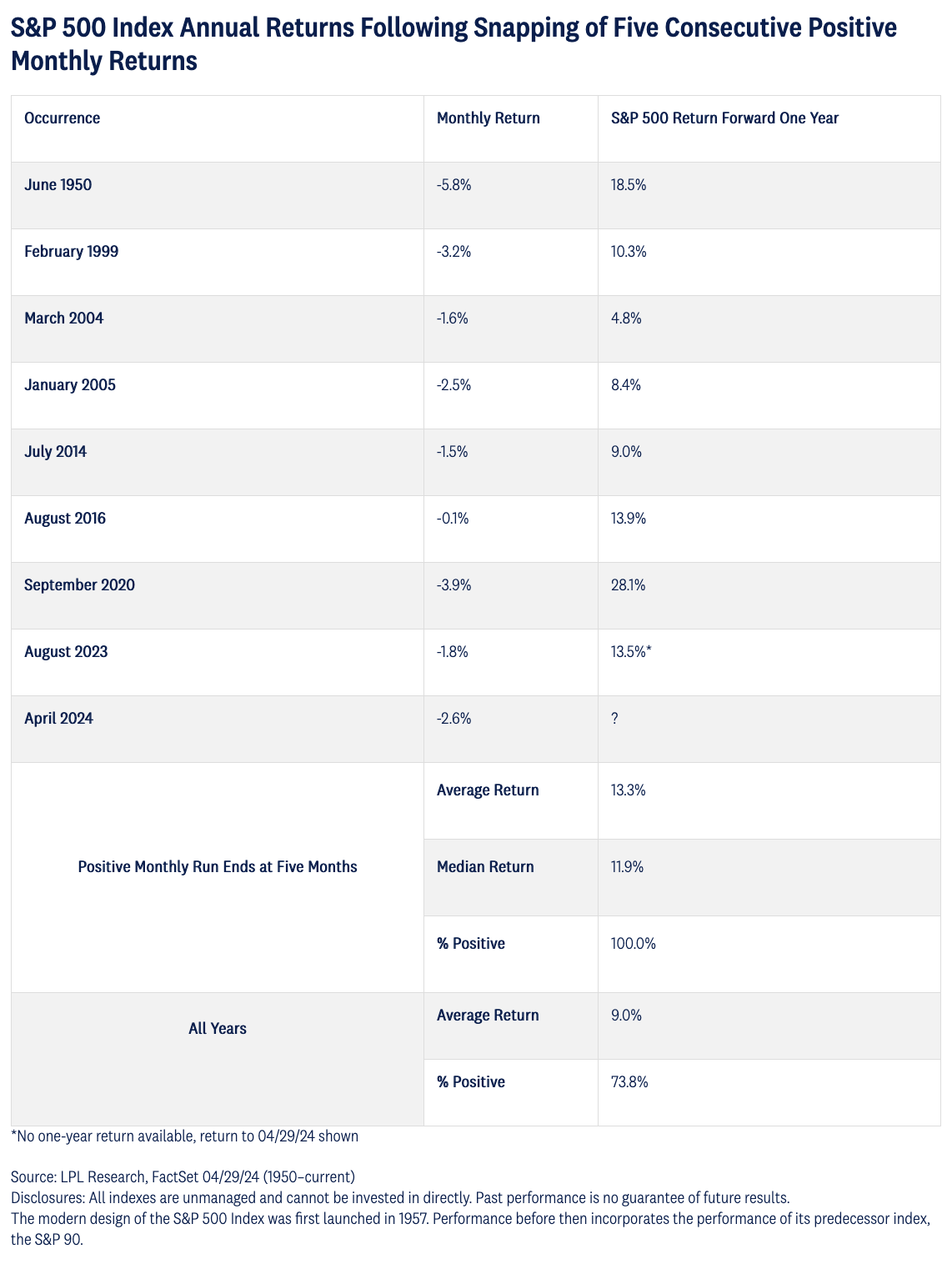

Should investors be concerned about April snapping a five-month winning streak for stocks? Analyzing all periods since 1950, this is the ninth time this has occurred. Three of the nine times have been in the post-COVID-19 period and all but one has occurred from 1999 onward. This may not be a concern for equity investors, as the S&P 500 return one year after the end of the month that snapped the five-month winning streak has been positive every time, with an average return of 13.3%, considerably higher than the average 9% gain over all rolling one-year periods. A potential explanation for this phenomenon is that it shows pullbacks help work off overbought conditions, before stocks continue moving higher over the following year. Interestingly, when the positive streak snapped is six months or longer, the average return a year later is weaker at 9.2%, with only 72% positive (of 22 occurrences).

Is Snapping a Five-Month Positive Run Actually Good for Stocks?

Summary and Current Positioning

“Sell in May and go away” has historically held true to the degree that it starts a six-month period with the weakest performance for stocks relative to the rest of the year. But as an investment strategy, without a suitable substitute investment, it would fail on average as overall returns for the May–October period have been positive. As such, we do not recommend selling this May, with LPL Research’s Strategic and Tactical Asset Allocation Committee (STAAC) maintaining a neutral tactical outlook on equities. The STAAC sees the risk-reward trade-off between equities and fixed income as roughly balanced given the economic and earnings backdrop. The potential for a soft landing for the U.S. economy and growing earnings help offset still-elevated stock valuations. There has been a recent negative shift in sentiment, but we typically view this through a somewhat contrarian lens, and do not believe this marks the end of the bull market. We believe resilient breadth metrics, cyclical sector leadership, little, if any, sign of panic in credit or volatility gauges, economic resiliency, and longer-term momentum may signal further strength ahead.

Copyright © LPL Research