by Carl R. Tannenbaum, Chief Economist, Northern Trust

Geopolitical stress is economically costly.

I heard quite a commotion from my family room last weekend. My daughter was perched on the couch, and the noise was coming from her laptop. When I asked what she was doing, she said she was watching a movie with her boyfriend…who was 800 miles away. We’ve come a long way since Saturday night trips to the cinema.

The film they were enjoying was Everything, Everywhere, All At Once, the winner of last year’s Academy Award for best picture. It can be hard to follow, as the main characters careen between the real world and an odd metaverse. But the sudden shifts of scenery and situational stress effectively illustrate the challenges of daily life. Well produced, and brilliantly acted: four stars from this reviewer.

The movie and its title have particular resonance in the present day. The lengthy list of current geopolitical risks has us trying to deal with everything, everywhere, all at once. How did we get to this point, and how can we best deal with the uncertainty?

Twenty years ago, our current circumstances would have been difficult to foresee. Expanded global commerce seemed to be delivering on its promise: standards of living were rising, poverty was falling and markets were bullish. The connection between economic and diplomatic cooperation was strong, and the world was at relative peace.

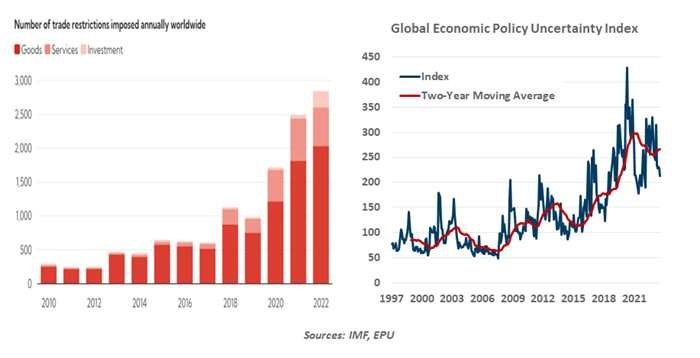

The 2008 financial crisis was a watershed moment. It illustrated the downside of international linkages, and produced a lasting setback to economic growth. The slow recovery that followed gave momentum to anti-trade rhetoric and populist politicians. Tariffs, quotas and other anti-competitive measures advanced; merchandise trade as a percentage of global output retreated.

The pandemic served as an accelerant to economic fragmentation. Supply chain frictions led countries to look for alternative sources at home (or close to home). The use of sanctions to punish bad actors became a consideration for the geography of investments and operations.

Coincident with the reversal in international commerce has been a rise in geopolitical friction. Measures of global stress have been rising for more than a decade. Antipathy between global powers has deepened, and conflicts between countries have become more common.

International organizations charged with preserving the global order have been weakened. The World Trade Organization is currently unable to adjudicate trade disputes between nations because its stakeholders can’t agree on appointments to its appellate body. In the absence of binding arbitration, countries have been more aggressive with protectionist measures, which invite retaliatory action from the other side.

The International Monetary Fund (IMF) is struggling with an increasing case load and challenges sustaining the resources it requires. Rising interest rates, limited export opportunities and the impacts of climate change threaten to land more countries on the IMF’s watch list in the years ahead; the full support of its sponsors will be required to avoid meltdowns. Deep budget deficits and needs on home fronts may make that support difficult to secure.

Advancing polarization within and across countries has provided open space for rogue actors. According to the Uppsala Conflict Data Program, the number of state-based armed aggressions is at an 80 year high. Wars in Ukraine and Gaza are the most prominent examples, but there are a host of more minor skirmishes ongoing.

A fraying global economic order has made conflict more likely

The humanitarian costs have been immense: the United Nations estimates that there are more than 100 million displaced persons in the world today. As they seek shelter, border crises are becoming more frequent, adding to political friction in destination states. Aid organizations have their hands full.

Each of today’s conflicts has idiosyncratic root causes. The Middle East has alternated between simmering and boiling over for decades, amid the heat of sectarian differences. But the fraying of the global economic order has created conditions which make outbreaks more likely.

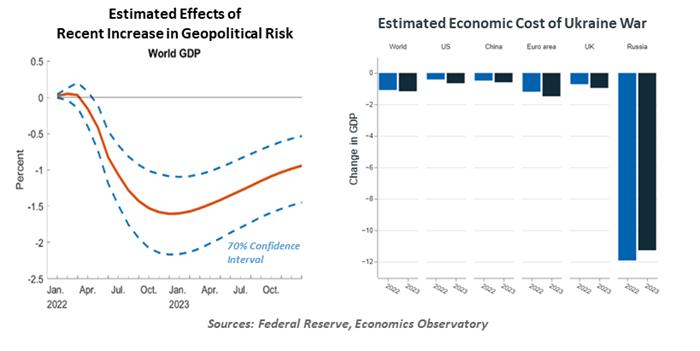

Geopolitical stress is economically costly. The uncertainty surrounding global risks raises costs of capital, and may delay productive investments. Risk aversion can affect spending behavior, market performance and the flow of financing. Operational design becomes sub-optimal as logisticians seek to avoid potential hot spots.

When these stresses become kinetic, the costs are even higher. War disrupts output and transit channels; it results in losses of human capital; and it impairs demand. Product shortages can cause increases in inflation and restrictive policy from central banks. While the consequences are most significant for the combatants, the effects are felt far from the front lines.

Assessing threats is very difficult. There are several geopolitical risk indicators (GRIs) which are based on the tone of news stories. They are interesting to follow, but they do not have a consistent track record of being leading signals. As an example, GRIs looked reasonably benign prior to Russia’s invasion of Ukraine in 2022, spiking only after the fighting had begun.

Keeping a watch list of possible threats is also common. But 9/11, COVID-19 and the war in Gaza were not at the top of anyone’s watch list before they occurred. Enumerating tail risks is an interesting exercise, but it is impossible for firms or investors to insulate themselves against any eventuality. Risk is endemic in almost all situations; some of it simply has to be accepted.

That said, being prepared for eventualities can reduce their costs should they ever manifest. Scenario analysis, which can reveal vulnerabilities, is an essential practice. Maintaining playbooks and investing in resilience become more important in volatile times.

Peace and prosperity are inextricably intertwined. We do not have the option of escaping to an alternative metaverse; we need to work on making our world a more settled place. If we fail, the human and financial costs will be tough to bear.

Always better to prepare, not predict

Copyright © Northern Trust