by Rick Rieder, CIO, Global Fixed Income, and Russell Brownback, Head of Global Macro, Fixed Income, BlackRock

Key takeaways

- The potential for a Fed pause presents an opportunity for investors to consider adding duration back into their portfolios

- In this market regime, we believe duration serves well as hedge and equity diversifier

- Advisors who were underweight bonds in their traditional 60/40 portfolios should consider bringing bonds back to benchmark level or an overweight

Navigating Today's Environment It's Just Math

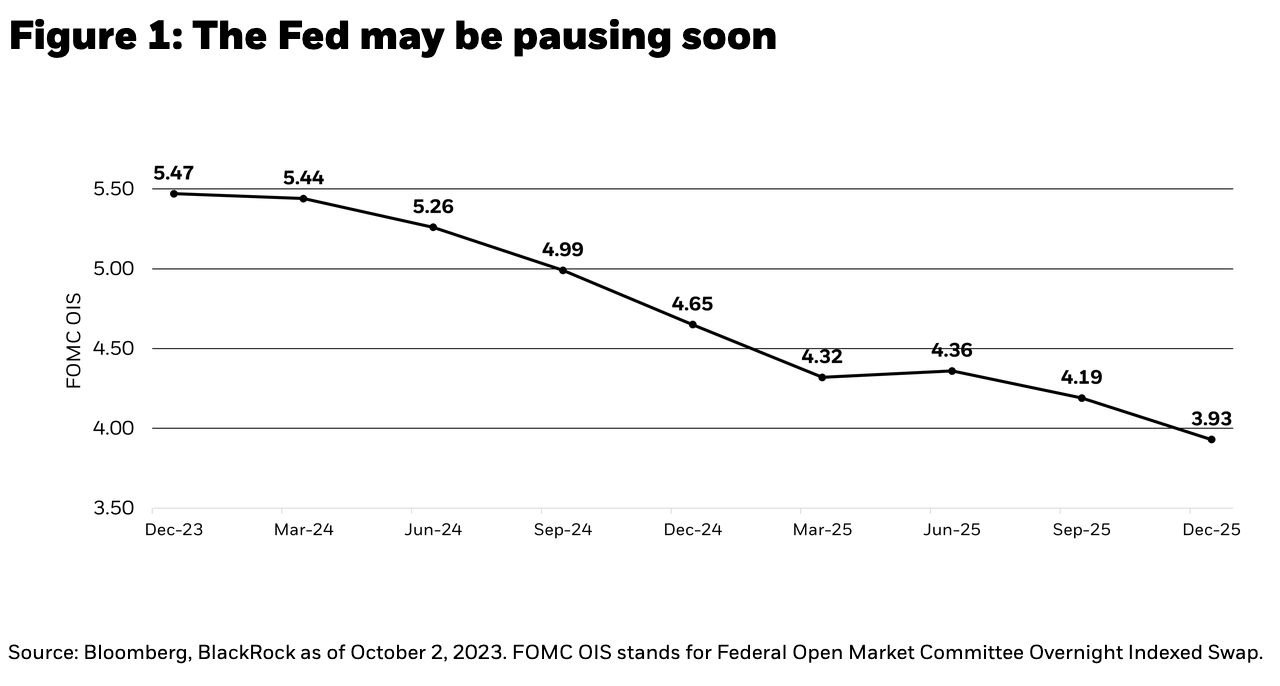

Beginning in March 2022, the Federal Reserve (Fed) raised interest rates at the fastest pace since the 1980. Financial markets are now pricing in for the central bank to be near the end of its hiking cycle (Figure 1).

With yields at current levels, bond funds can lock in longer term yields, offer price appreciation potential and overall serve as a hedge against a possible hard landing. Though elevated cash balances worked during the Fed’s hiking cycle, we believe now is an opportunity for clients to consider adding duration given the potential for a Fed pause.

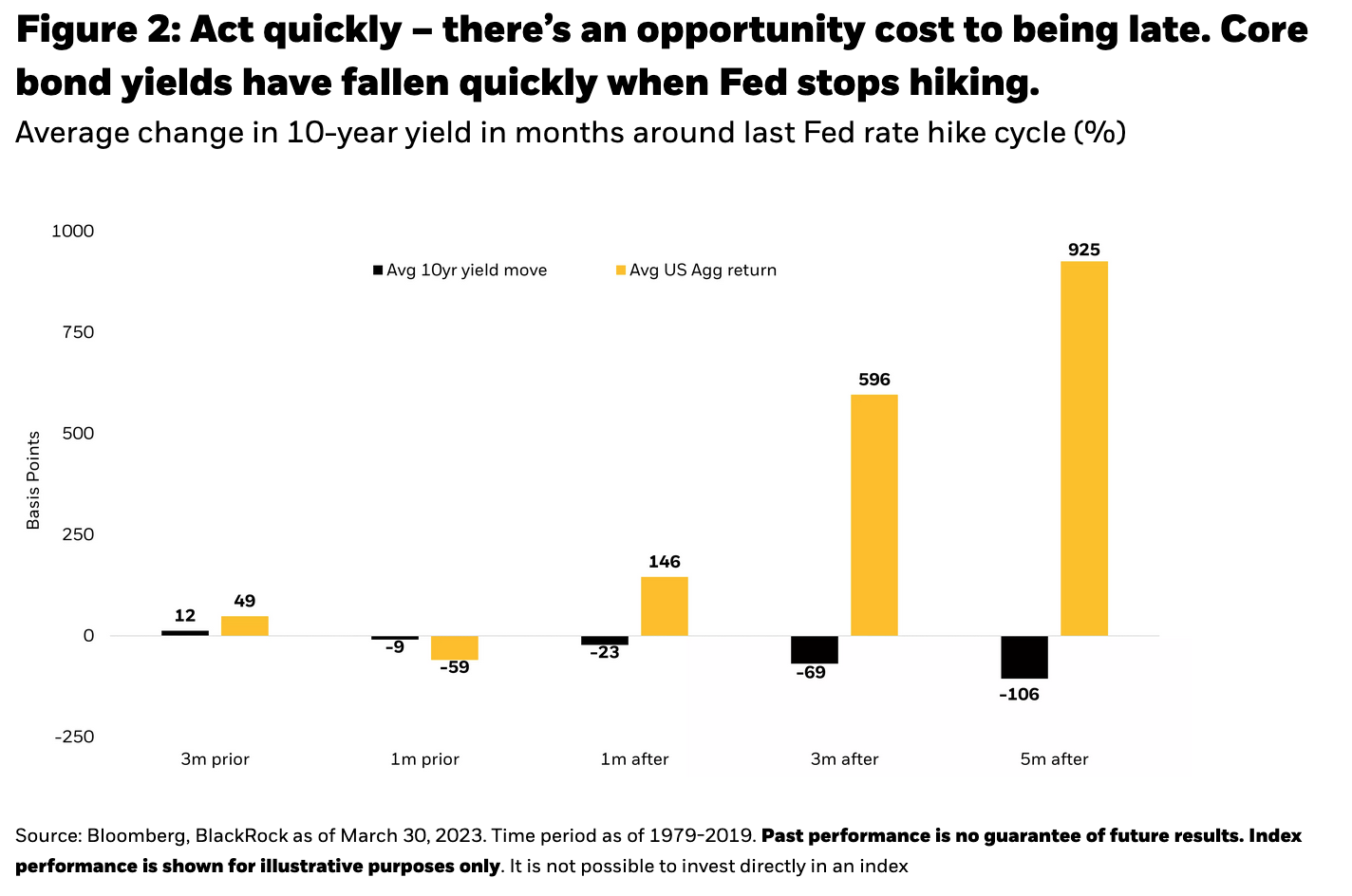

While investors are not penalized for being early to adding duration, there is a potential cost to being late (Figure 2). Historically, cash underperforms when the Fed stops hiking (Figure 3).

Duration as a Hedge

In today’s environment of slowing growth and inflation volatility, duration may offer a hedge against potential market volatility and be used as a portfolio ballast. Amidst the Fed getting close to pausing, this bodes well for core bond funds, like the BlackRock Total Return Fund and the BlackRock Core Bond Fund, that may be able to offer defense in times of market stress in the form of income. For example, during periods where the Fed is hiking interest rates, the correlation of US Treasuries to equities is positive (+27%), however when the Fed is on hold or cutting rates the correlation drops (-16%)1.

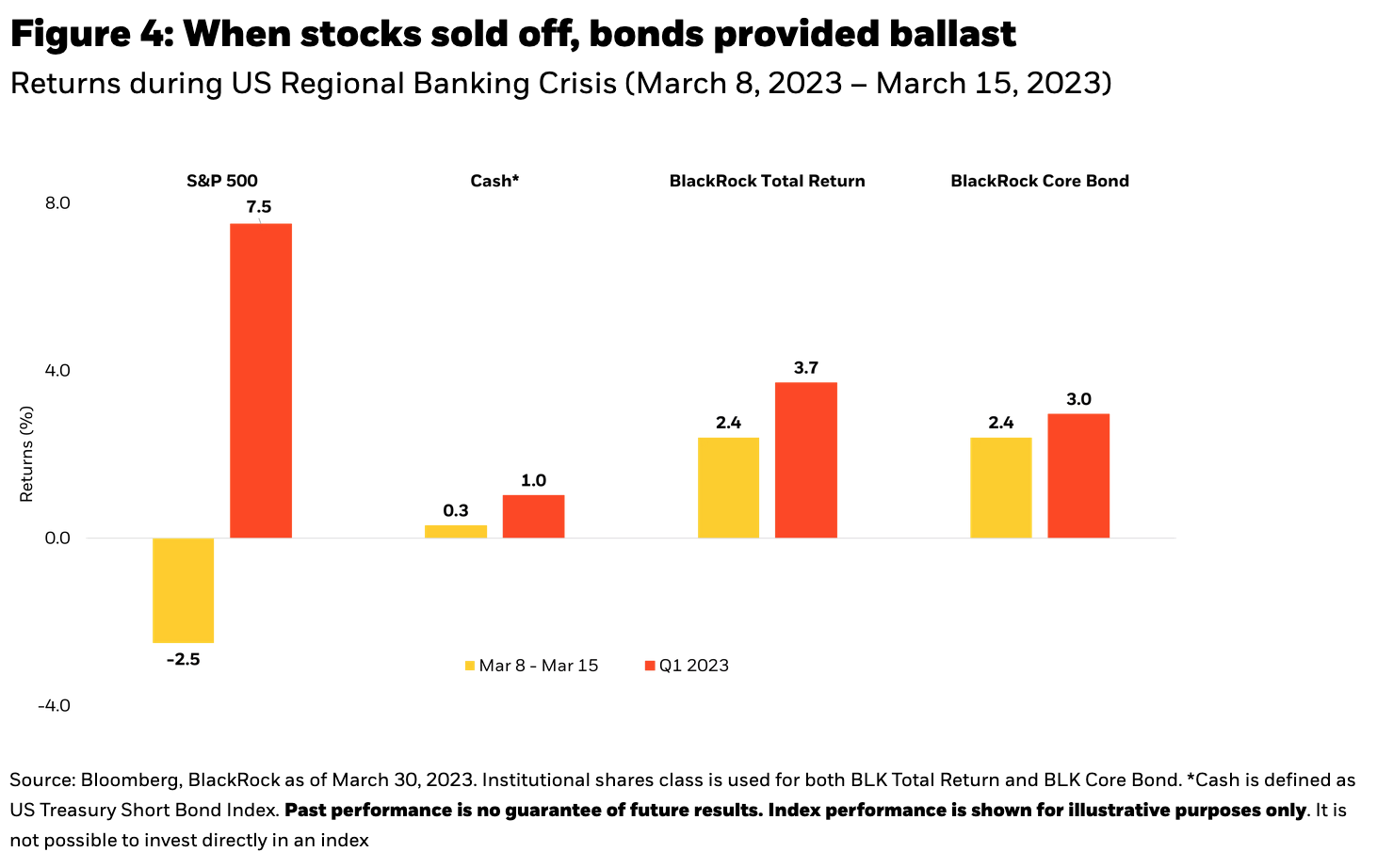

In addition, as markets were rattled by the US regional banking crisis in March of this year, Total Return and Core Bond saw positive returns as equities sold off (Figure 4).

Performance as of 9/30/2023, BlackRock Total Return Fund: 1yr: 1.10%, 3yr: -4.81%, 5yr: 0.44%, 10yr: 1.69%. BlackRock Core Bond Fund: 1yr: 1.30%, 3yr: -5.13%, 5yr: 0.27%, 10yr: 1.26%.

Case Study: Positioning the 60/40 Portfolio

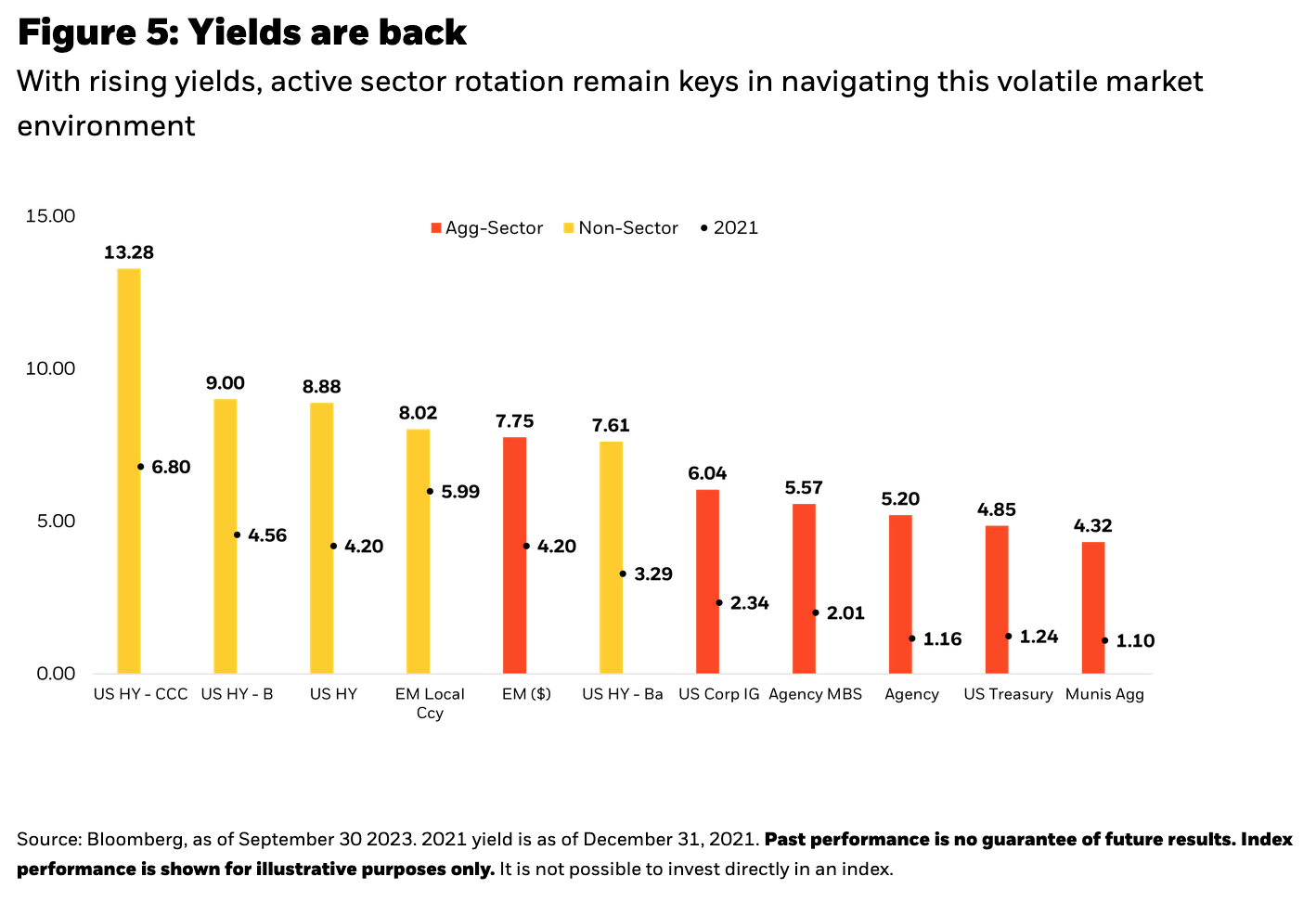

As of March 31, 2023, the average advisor’s portfolio was underweight fixed income by 7%2. In a market regime with over half of fixed income yielding over 4%, advisors should consider bringing bonds back to benchmark level or to an overweight (Figure 5). In periods of slowing growth, stocks may experience higher volatility, while high-quality bonds may offer a stable source of returns.

As of the latest rebalance in October 2023, BlackRock’s Target Allocation Hybrid 60/40 Model latest rebalance currently holds 62% and 36% of its portfolio in equities and fixed income, respectively – with the remainder being in cash. In this rebalance, the Model looked to enhance the overall quality of the portfolio and maintain its overweight to duration.

To increase equity diversification, dynamically navigate today’s bond market and source active returns, the Model continues to hold a 17% allocation to BlackRock’s Total Return Fund, making it the Model’s largest fixed income allocation (Figure 6).

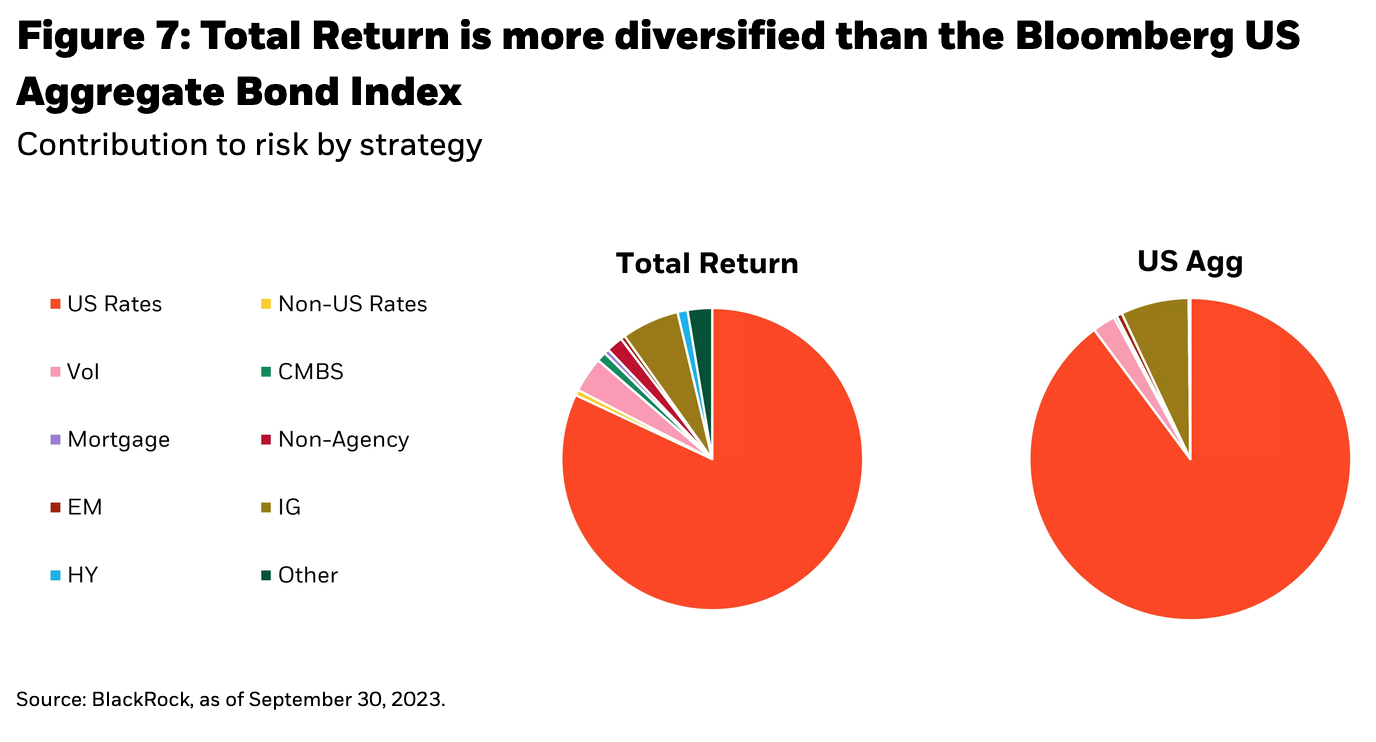

The Total Return Fund is an actively managed fixed income strategy which seeks to realize a total return exceeding that of the benchmark, Bloomberg US Aggregate Index. Given the fund's risk profile and long-term performance, Total Return Fund seeks to provide investors with core-bond defense by seeking to manage risk on the downside when markets come under pressure, while striving to provide investors with core-plus like returns by seeking to actively manage exposures for better returns over the long-term. The fund employs a diversified multi-sector approach built to navigate different market environments (Figure 7).

Summary

As the Federal Reserve nears the end of its hiking cycle, we believe now is an opportunity for investors to consider adding duration back to their portfolios. Duration may provide defense against potential market volatility and be used as a portfolio ballast during periods of slowing growth and inflation volatility. History shows that core bonds act as a diversifier when equity markets sold off.

The BlackRock Total Return Fund, employs a diversified approach with sufficient flexibility in order to navigate periods of market volatility, while providing cushion in the form of income, and broad portfolio diversification. This has resulted in generating Core Plus like returns with Core like risk. As of September 30, 2023, the fund has a Yield to Worst (YTW) of 6.47% and 30 Day SEC Yield of 4.09% / 4.07% (subsidized / unsubsidized). The Bloomberg US Aggregate Index has a YTW a of 5.38%, as of September 30, 2023.

In addition, BlackRock Core Bond provides investors with a diversified, core-bond exposure that seeks to generate attractive risk-adjusted returns that exceed the fund's benchmark, Bloomberg US Aggregate Index. The fund has a YTW of 5.93% and 30 Day SEC Yield of 4.74% / 4.60% (subsidized / unsubsidized) as of September 30, 2023.

The performance quoted represents past performance and does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when sold or redeemed, may be worth more or less than the original cost. Current performance may be lower or higher than the performance quoted. For current month-end returns visit www.blackrock.com.

Copyright © BlackRock