by Chris Hogbin, Head—Equities, AllianceBernstein

Stock markets fell in the first quarter as Russia’s invasion of Ukraine destabilized the growth outlook, amplified concerns about rising interest rates and unleashed geopolitical risks. While the conflict has created many uncertainties, we believe the impact of persistent inflation will be the dominant influence for equity investors through the remainder of 2022 and beyond.

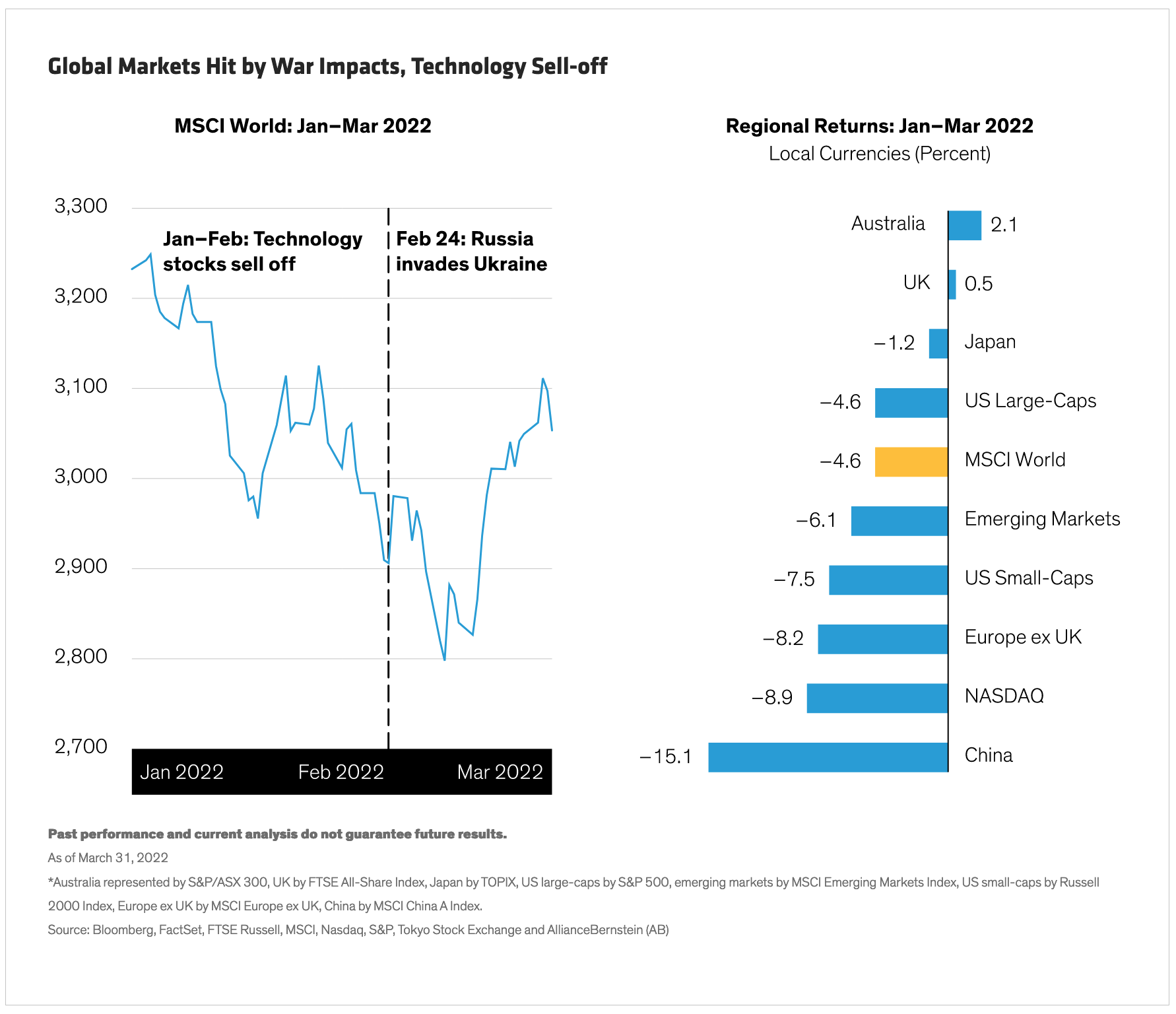

Seven straight quarters of gains for global stocks came to an abrupt end in early 2022. The MSCI World Index fell by 4.6% in local currency terms (Display), but recovered all its losses since the invasion by quarter-end. Markets in Australia, the UK and Japan held up relatively well, while Europe, emerging markets and China underperformed.

Market declines weren’t only driven by the war. Early in the quarter, expensive technology shares sold off, particularly in the US, as these stocks are more vulnerable to rising interest rates. Investors also worried that tightening monetary policy could jeopardize the world’s recovery from the pandemic. And Chinese stocks were extremely volatile on concerns about regulation of internet giants, property market default risk and a COVID-19 outbreak.

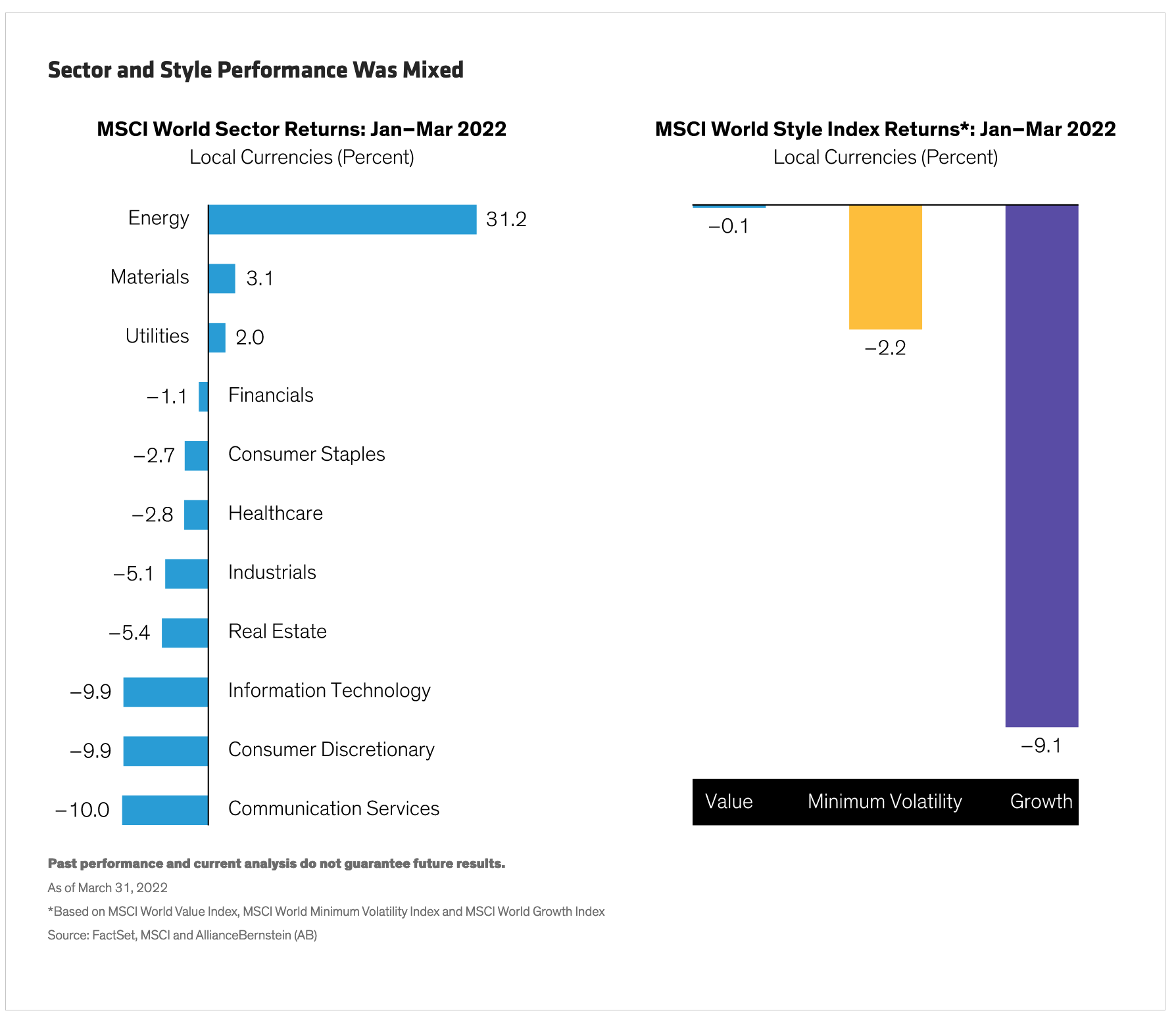

Sector performance was mixed (Display, below left). Energy stocks surged while tech and consumer-discretionary shares tumbled. Defensive sectors such as utilities and healthcare were relatively resilient. Value stocks, which tend to benefit from rising interest rates, outperformed growth stocks by a wide margin (Display, below right).

Putting Volatility in Perspective

Putting Volatility in Perspective

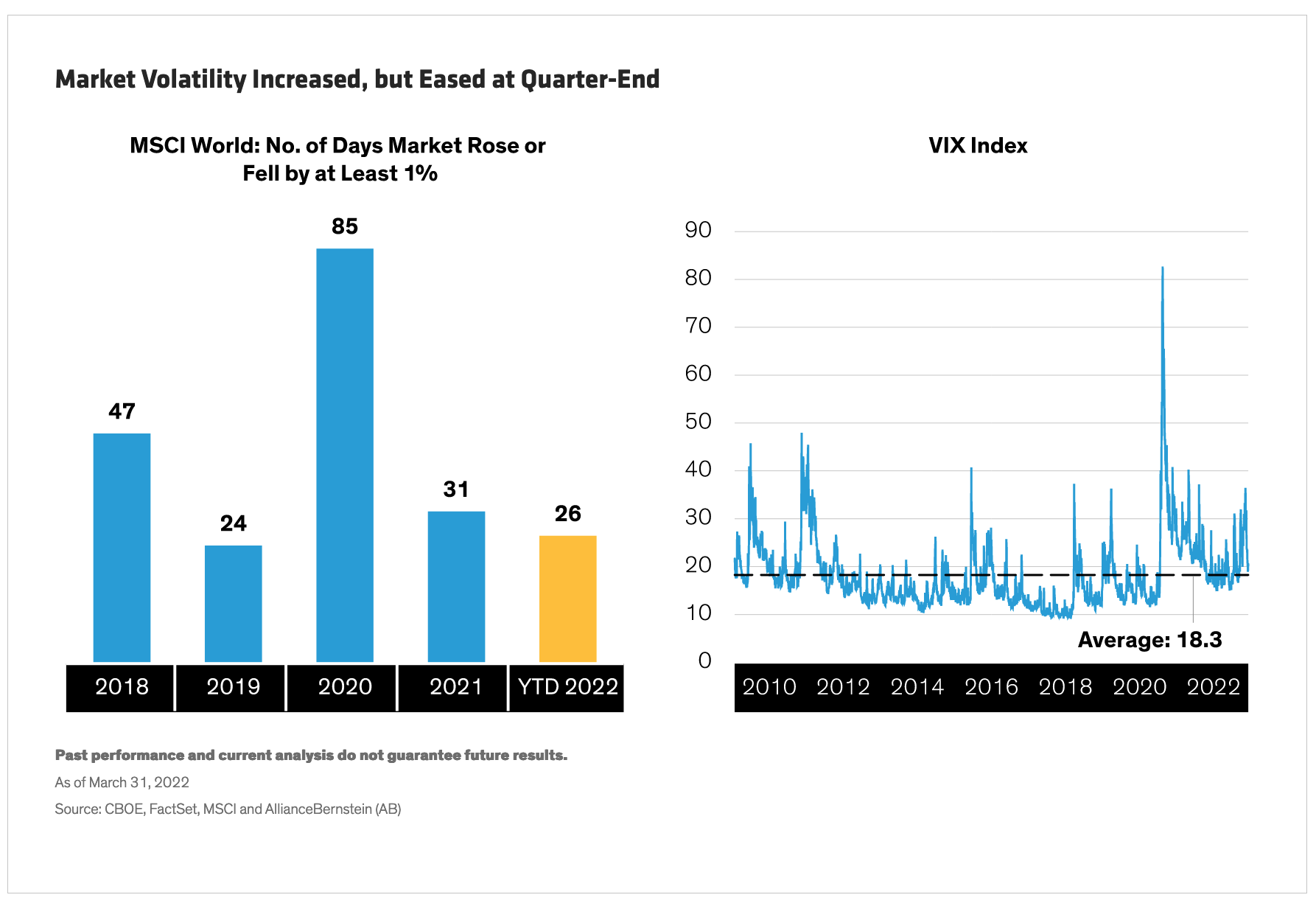

Volatility surged, then eased. The MSCI World rose or fell by at least 1% on 26 trading days during the first quarter (Display, below left). Still, even as the VIX index of US equity market volatility jumped, it didn’t come close to levels seen during the pandemic sell-off in early 2020 (Display, below right). In a surprisingly fast change of sentiment, the VIX fell back toward its long-term average by quarter-end, suggesting that investor anxiety diminished significantly.

Since the February 24 invasion, volatility has been driven by three factors. First, risk aversion rose as investors were shocked by Europe’s first major war since World War II and the spiraling humanitarian tragedy. As civilian casualties increased and more than 4 million refugees fled Ukraine, fears mounted of a direct military conflict between Russia and NATO countries—and the terrifying prospect of a nuclear exchange.

Since the February 24 invasion, volatility has been driven by three factors. First, risk aversion rose as investors were shocked by Europe’s first major war since World War II and the spiraling humanitarian tragedy. As civilian casualties increased and more than 4 million refugees fled Ukraine, fears mounted of a direct military conflict between Russia and NATO countries—and the terrifying prospect of a nuclear exchange.

Second, severe sanctions on Russia led to the removal of Russian stocks from MSCI indices, wiping out holdings for some investors, particularly in emerging-market portfolios. Third, the conflict manifested itself in markets via disruptions to Russian and Ukrainian exports of commodities such as oil, gas and wheat. This fueled inflationary forces that threatened to tip economies into recession, or worse, stagflation—a painful combination of a growth stagnation and rising prices. Supply-chain concerns emanating from China’s COVID-19 situation augmented these risks.

Inflation Will Be Sticky

Inflationary forces were already brewing at the beginning of 2022. In recent years, the deflationary forces of globalization have been under pressure. Populist trends, from Brexit in the UK to the US-China trade war, prompted countries and companies to rethink global supply chains. Then, the pandemic led to widespread supply disruptions and central banks implemented historically loose monetary policies.

The Russia-Ukraine war has exacerbated these pressures. Even if some war-related disruptions are resolved, countries and companies are seeking new ways to source essential inputs, from oil and gas to auto components, microchips and food ingredients. Localizing sources of supply will keep prices higher because it means companies aren’t necessarily producing raw materials and components in the most cost-effective locations. And demand for more local staff is likely to continue pushing up wages, especially as employees are leaving their jobs in record numbers, in what has become known as the Great Resignation. Now it’s clear that inflation will be sticky.

Consumer price inflation in the US reached an annualized rate of 7.9% in February, a 40-year high. Eurozone inflation jumped to 5.8% in February, while UK inflation surged to a 30-year record of 6.2%. Even in Japan, which has battled deflationary pressures for years, consumer price inflation might approach the central bank’s target of 2% this year.

Supply Shock Creates New Challenges

Since inflation today is being driven by a supply shock, the challenges are very different than inflationary bouts in the recent past. Central banks have a monumental task. In the US, the Fed began raising interest rates in the first quarter and has shifted to a more hawkish stance. The European Central Bank has also moved to tighten monetary policy, but the region faces greater risks to growth because consumers are in a much weaker position. Given the complex forces fueling inflation, central banks must be very flexible to ensure their policy actions don’t undermine growth.

Managing inflation while maintaining growth will be very tricky. Today’s inflation is pervasive, infecting many products and industries across the globe. Its myriad sources go well beyond traditional shortages to include geopolitical frictions, a retreat from globalization and changing preferences of the workforce. New sources and supply chains need to be established, and the traditional approach of raising interest rates to stifle demand may be less effective.

Even if inflation cools, we believe it’s likely to remain higher than we’ve been accustomed to for many years. In this new world, we believe equity investors must apply a strategic view of inflationary trends to fundamental analysis. That involves understanding the relationship between inflation, earnings and returns, figuring out the micro impacts on industries and companies, and developing investing criteria according to different portfolio philosophies and processes.

From Earnings Growth to Profitability Squeeze

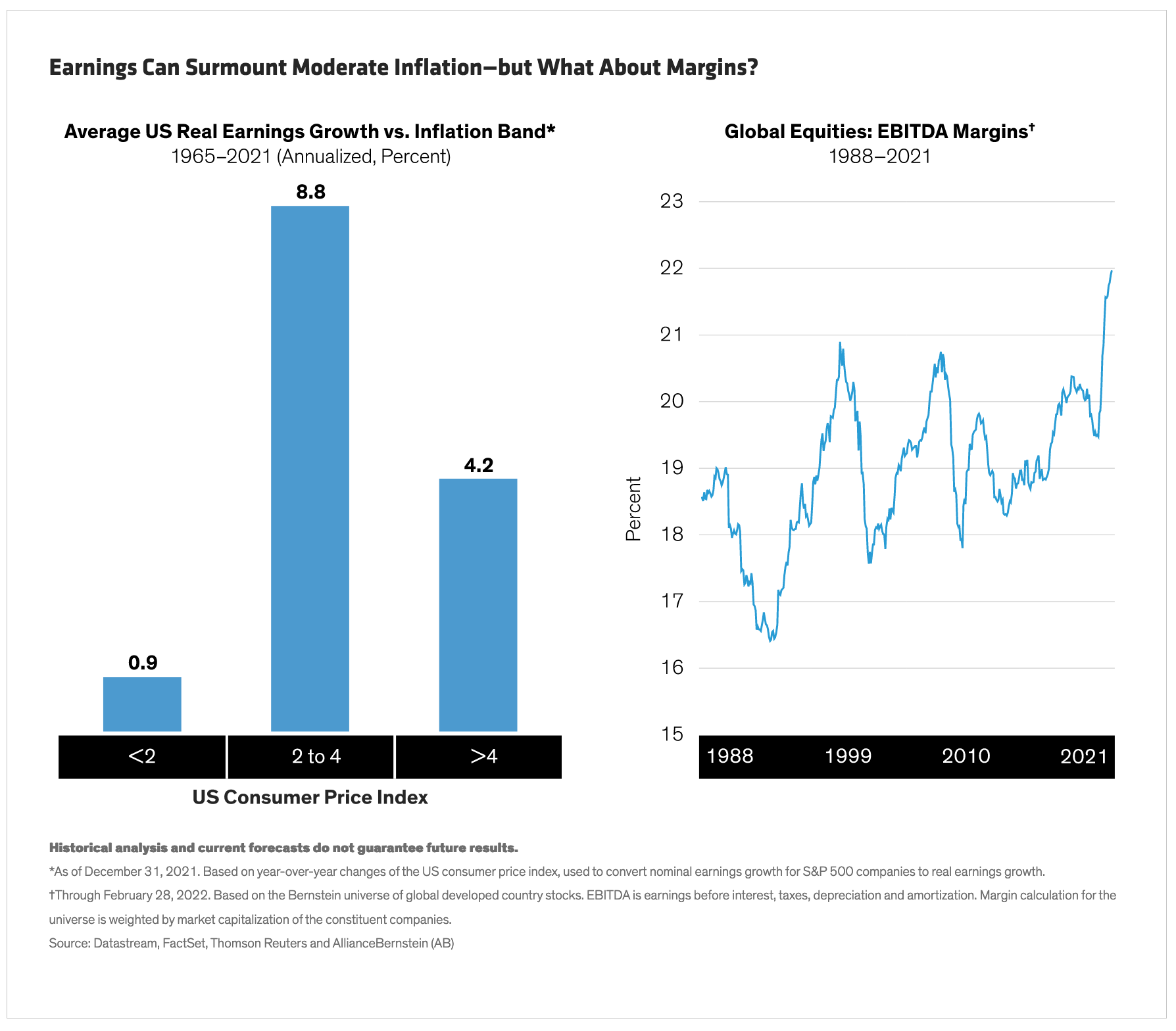

Higher prices add hurdles for companies. While inflation often boosts revenues, a company’s nominal profits must grow fast to stay ahead of rising costs. At moderate inflation levels, earnings tend to outpace prices. Our research shows when inflation was between 2% and 4% per year, US companies delivered real earnings growth of about 8.8% per year since 1965. We’ve observed similar trends for global companies over a shorter time span.

But can companies maintain earnings growth in the environment we’re facing? Measures of profitability point to the challenges. Today, global net income margins are extremely high (Display), implying that profitability is ripe for a reversal. The combination of high margins, slowing growth and input cost pressure will squeeze profitability for many companies, in our view. Equity investors must find companies that can maintain margins should these conditions persist.

We believe this will be a key differentiator of long-term equity return potential in the new inflationary world. Our research also indicates that the dispersion of returns tends to be wider during periods of higher inflation. A wider dispersion usually provides active managers with attractive opportunities to find companies with better return potential.

To do so, investors must identify the microeconomic impacts of inflation that affect business outlooks, cash-flow potential and future returns. Across industries and markets, two key questions can help frame the analysis.

How are input costs evolving? Many companies that are meeting revenue expectations are facing earnings downgrades because of rising costs. Those that can substitute cheaper input sources will have an advantage in maintaining margins as prices rise. Companies capable of restructuring manufacturing processes and supply chains will also be better placed to preserve profitability.

Does the company have pricing power? Pricing power is always an important indicator of a quality business, but even more when inflation runs high. Look for conservative companies that don’t make sharp shifts in guidance. Consistency of recent profit margins is another good sign of pricing power. Companies with long-term secular catalysts for their business, such as environmental efforts or technological adoption, are also better equipped to push prices higher without sacrificing demand.

Quality Features for Evolving Risks

These questions can guide active portfolio managers to the right companies for the new regime. Since most of the asset-management industry’s quantitative models were developed after the high inflation of the 1970s, they’re designed for a deflationary regime and might not provide reliable indicators for the future. And because the effects of inflation on companies are complex, we believe comprehensive fundamental analysis that emphasizes high-quality features is essential to find companies that will endure tougher conditions.

Growth portfolios, for example, should be wary of companies that still look overvalued after the recent sell-off, while targeting those with sustainable growth drivers that can withstand a tougher macroeconomic environment. Value stocks historically have performed better when interest rates rose. However, we believe companies with higher-quality cash flows and balance sheets, and clear catalysts for recovery, are preferable to the cheapest names with inferior fundamentals.

As the new quarter begins, the mood in markets has calmed somewhat. But risks abound, from a Russian debt default to China’s growth to the global economy’s fragility. While the market has stabilized after the initial war shock, be prepared for more volatility as fallout from the conflict ripples through the global trade system. With a disciplined approach to company fundamentals that puts inflationary threats and opportunities front and center, we believe investors can gain confidence in positioning for the complex times ahead.

The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.

Copyright © AllianceBernstein