“In emerging markets, many exchanges and regulators are setting forth enhanced standards, often aimed at bolstering shareholder protections and corporate disclosure requirements.”

by Kathlyn Collins, ESG Analyst, Matthews Asia

Investors often think of emerging markets as taking cues from their developed counterparts—for example, by aiming to boost consumption and to achieve productivity gains. It may come as a surprise that some emerging economies have made an earlier start in adopting environmental, social and governance (ESG) conventions than many of their developed market counterparts. Among the significant ESG developments in emerging markets are the promotion of stronger ESG and corporate governance frameworks by exchanges and regulators. Their progress is particularly timely, given investors' increasing focus on ESG: Signatories to the United Nations-supported Principles for Responsible Investing grew at an annual rate of more than 20% in 2019.1 In addition, 103 stock exchanges worldwide now participate in the Sustainable Stock Exchanges Initiative, representing over US $88 quadrillion in assets.2

Regulators and Exchanges Encourage Stronger Corporate Governance

In emerging markets, many exchanges and regulators are setting forth enhanced standards, often aimed at bolstering shareholder protections and corporate disclosure requirements. In some cases companies must adopt the standards in order to be listed on the exchange or segment. The results benefit many different stakeholders. Investors benefit from improving access to ESG information and potentially better business performance over the long term. Benefits also accrue to participating companies by way of improved overall corporate accountability and risk management, as well as the possibility of attracting new capital. Exchanges gain increased competitiveness and access to capital.

One such listing segment is Novo Mercado, part of Brazil's prominent B3 stock exchange. In the years leading up to the launch of Novo Mercado, investors in Brazilian equities faced two major challenges, as identified in a case study by the International Finance Corporation (IFC).3

- First was the prevalence of non-voting shares: Companies were legally permitted to issue up to two-thirds of their capital as non-voting shares. As a result, holders of voting shares could control companies by owning as little as 17% of the listed company.

- Second was a change of control law which enabled transfers of controlling shares to be completed at extraordinarily high premiums. At the same time, minority shareholders were left out in the cold, unable to sell their shares alongside the controlling blocks.

In December 2000, Novo Mercado was launched with the intent to achieve equitable treatment of all shareholders by instituting corporate governance requirements that extended well beyond Brazil's legal and regulatory framework. Companies listed on Novo Mercado can only issue common voting shares, and the same conditions provided to controlling shareholders during a change of control are extended to all shareholders, ensuring what are known as “full tag-along rights” for every shareholder. Companies must also adhere to enhanced transparency and monitoring policies.

Listings on Novo Mercado have grown at an impressive rate and now constitute a significant share of the Brazilian market. Encouragingly, exchanges in other emerging markets are following the lead of Novo Mercado. For example, the chairman of Argentine stock exchange BYMA cited Novo Mercado as inspiration for BMYA's special listing segment for companies with high corporate governance standards.4

The Moscow Exchange (MOEX) has also been taking significant steps towards development of responsible investing. It became a Sustainable Stock Exchange Partner Exchange in 2019 and in the same year launched the daily tracking of Russia's first sustainability indices as well as new MOEX's listing rules providing for the creation of the Sustainability Sector.5 Higher listing standards among exchanges such as the Novo Mercado and Moscow Exchange are a welcome development for long-term investors, but fundamental research remains important in emerging markets.

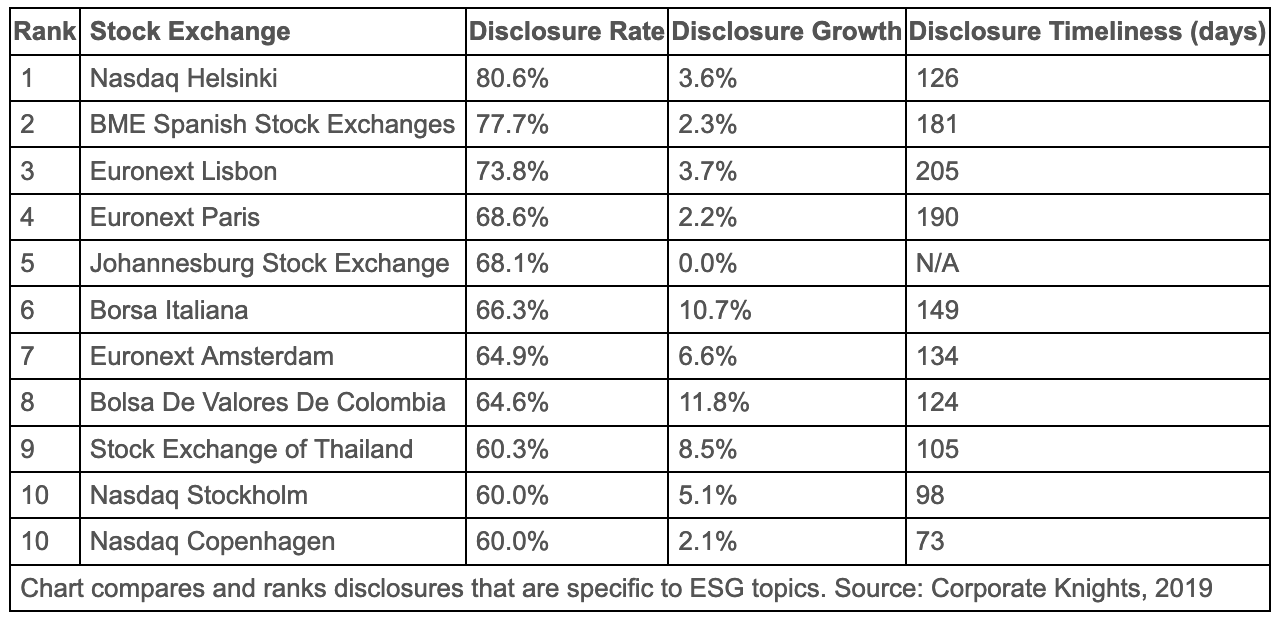

TOP TEN GLOBAL STOCK EXCHANGES IN TERMS OF ESG DISCLOSURE

Three of the world's leading stock exchanges for ESG disclosure are found in emerging markets—South Africa, Colombia and Thailand.

Asia Sets a Strong Example

Research by CFA Institute highlights Thailand as an example of swift progress by an emerging market toward development of a mature ESG disclosure mentality, helped in large part by actions from Stock Exchange of Thailand (SET).6 In 2019, SET placed ninth on the Corporate Knights ranking of stock exchanges worldwide based on ESG disclosure of issuers, earning it the highest ranking in Asia—even above the developed-market Australian Securities Exchange.7 This represents a notably rapid evolution for SET, given its low ranking of 31st out of 35 in 2012. The exchange's successes are attributed to multiple efforts, including ongoing ESG training for listed companies, a new Corporate Governance Code in 2017 and annual publishing of a list of companies that meet ESG performance criteria.

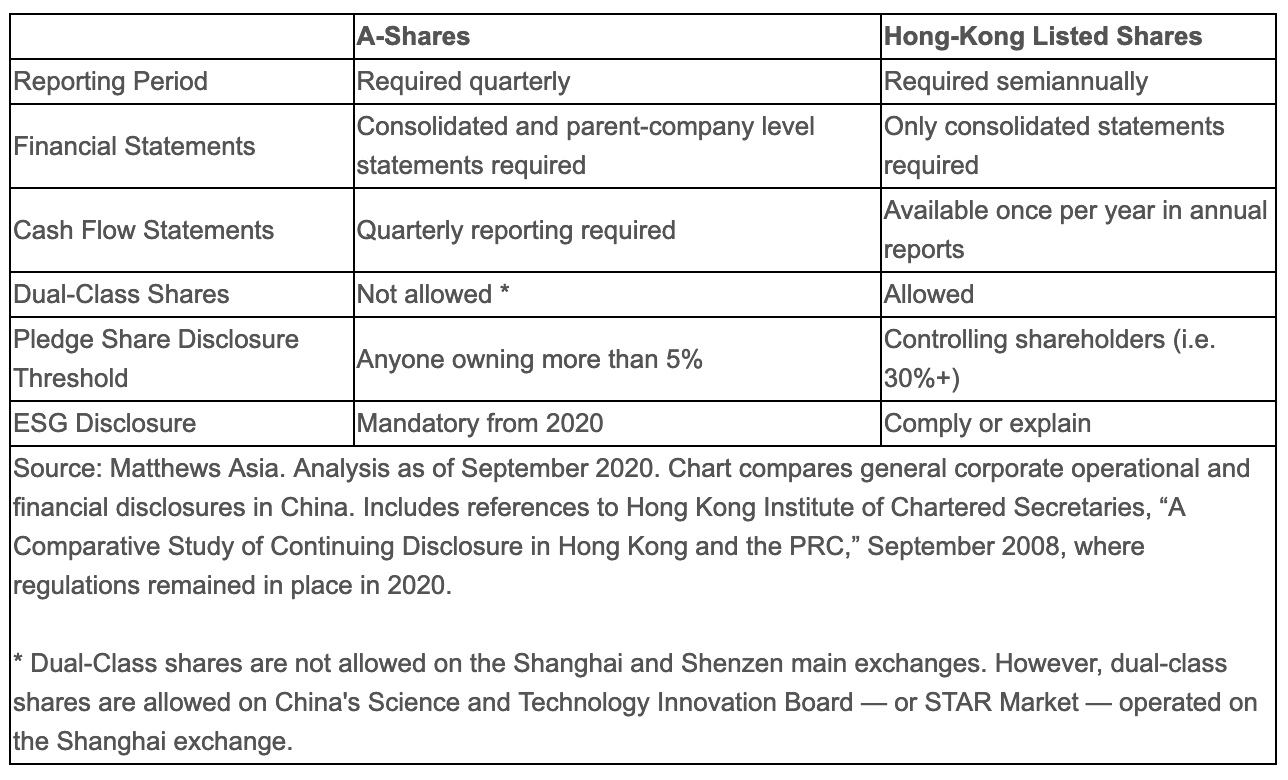

China, the region's largest market, has also made considerable progress on the disclosure and transparency front, encouraged by China's exchanges. China has taken many steps to give investors more confidence to invest in the country's capital markets by focusing policy on corporate governance reforms. Policymakers have amended or issued key rules and guidelines over the past years related to financial reporting, disclosure of substantial ownership stakes and director trading. Fair and relevant disclosure of financial and operational information is an important component of good corporate governance. In some respects, A-share listed companies (those that trade in China's domestic markets) are outdoing Chinese companies listed in offshore markets in areas such as comprehensive disclosure requirements. A-share companies also are subject to stricter regulation on potential conflicts of interest (see table below).

Enforcement and engagement also are on the rise. Bloomberg reported that in the first months of 2019, China's stock exchanges stepped up scrutiny of listed companies to address corporate governance concerns, sending 23% more queries to local firms, which was 62% more than in the same period in 2017. The queries focused on irregularities in the firms' financial results, inadequate information disclosure and relations with controlling shareholders with the goal of improving the credibility of China's capital markets for international investors.8

Integrating ESG into Fundamental Analysis

When investing in emerging markets, ESG considerations may play a key role in fundamental analysis. Helping to identify opportunities and spotlight risks, ESG criteria provides a framework for beginning to evaluating material factors that could create either headwinds or tailwinds for individual companies. For active managers, ESG may play a particularly important function in bottom-up, active stock selection processes.

Investing with a long-term view, we believe ESG factors are highly compatible with the bottom-up, fundamental investment process that we employ at Matthews Asia. In our experience, well run, high-quality companies tend to survive better in times of stress, grow better in times of prosperity, and generate more cash than a company that has a bad character. We adhere to an integrated approach to ESG with an emphasis corporate governance; it is the input we consider most closely. Governance influences social and environmental factors and is near universal in its objective. We seek robust corporate governance that fairly considers the needs of non-control minority investors like ourselves. Companies require strong, ethical management teams and solid board oversight to maximize long-term returns for shareholders. We are also committed to comprehensive risk monitoring, driven by proprietary research and complemented by reputation risk monitoring via multiple research providers. Additionally, our ESG approach includes a consideration of what is material for each industry and sector, and a commitment to communicating concerns directly with company management teams.

Greater ESG adoption with emerging markets economy translates into greater transparency. Qualities that can be measured are qualities that can be improved. For economic growth to be sustainable, it should be inclusive and benefit all stakeholders. We see considerable progress in emerging markets and look forward to continuing to engage with our portfolio companies on key ESG considerations.

Kathlyn Collins, ESG Analyst, Matthews Asia

1 Saa, Lorenzo. “PRI welcomes 500th asset owner signatory.” UN PRI blog, 2020

2 Sustainable Stock Exchanges Initiative, September 2020

3 Alexandru, Petra; Ararat, Melsa; Santana, Maria Helena; Yurtoglu, Besim Burcin. Novo Mercado and its followers: Case studies in corporate governance reform. IFC Corporate Governance FOCUS publication; no. 5. Washington, D.C.: World Bank Group. 2008

4 Sustainable Stock Exchanges, “Argentina’s BYMA joins exchanges committed to sustainability.” December 20, 2017

5 Sustainable Stock Exchanges, “Exchange in Focus: Moscow Exchange Advancing ESG,” May 2020

6 Leung, Mary; Zembrowski, Pitor. ESG disclosures in Asia Pacific: A review of ESG disclosure regimes for listed companies in selected markets. Charlottesville, VA: CFA Institute. 2019

7 Corporate Knights, Measuring sustainability disclosure: ranking the world’s stock exchanges. 2019

8 Bloomberg, “China Steps Ups Vigilance on Company Disclosures as Market Opens.” June 2019

Investments involve risk. Past performance is no guarantee of future results. Investing in international and emerging markets may involve additional risks, such as social and political instability, market illiquidity, exchange-rate fluctuations, a high level of volatility and limited regulation.

The views and information discussed in this report are as of the date of publication, are subject to change and may not reflect current views. The views expressed represent an assessment of market conditions at a specific point in time, are opinions only and should not be relied upon as investment advice regarding a particular investment or markets in general. Such information does not constitute a recommendation to buy or sell specific securities or investment vehicles. Investment involves risk. Investing in international and emerging markets may involve additional risks, such as social and political instability, market illiquidity, exchange-rate fluctuations, a high level of volatility and limited regulation. Past performance is no guarantee of future results. The information contained herein has been derived from sources believed to be reliable and accurate at the time of compilation, but no representation or warranty (express or implied) is made as to the accuracy or completeness of any of this information. Matthews Asia and its affiliates do not accept any liability for losses either direct or consequential caused by the use of this information.

Copyright © Matthews Asia