Hints of a return to normal activity are encouraging, but the economy remains impaired.

by Carl R. Tannenbaum, Ryan James Boyle and Vaibhav Tandon, Northern Trust

After a traumatic spring, this summer gave glimpses of a return to normal life: Restaurants reopened, outdoor parties were thrown, and many families even took vacations. But with unemployment elevated and many sectors unable to return to their pre-COVID business models, the U.S. remains a recovering economy, not a recovered one.

Growth in the third quarter is shaping up to be strong, and rehiring is continuing at an encouraging pace, setting the stage for above-trend growth in the year ahead. Even so, until the virus is contained, we will continue to hold lower expectations for economic activity. The key risk to the outlook is a resurgence in infections that leads to renewed lockdowns or renewed fear that keeps consumers at home.

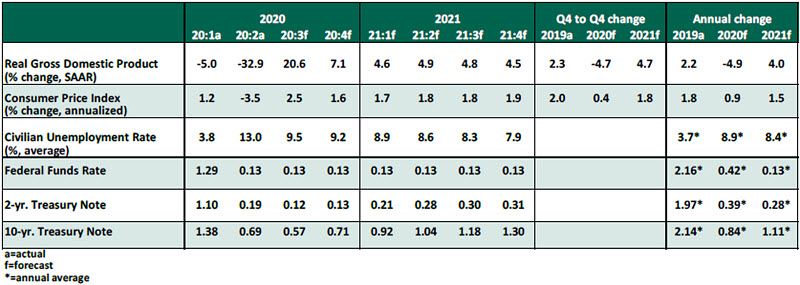

Key Economic Indicators

Influences on the Forecast

- The Bureau of Labor Statistics’ Employment Situation Summary report yielded an unexpected surprise, with the unemployment rate improving from 10.2% in July to 8.4% in August. The results raised questions, though, as the two main contributing surveys yielded very different results. Gains came from employees returning to work from COVID-19 layoffs as well as temporary census hiring; both flows will soon taper. As the number of workers reporting permanent job losses continues to rise, we expect a more tepid labor market recovery going forward.

- The path of the economic recovery depends on the path of COVID-19. Case counts in the U.S. remain elevated relative to the spread in other developed markets, though most countries have faced renewed bouts of infections as they reopen. The broad wave of new cases seen over the summer has abated, but the return of students to college campuses has driven new localized surges. As long as outbreaks persist, the economy will continue to function below its 2019 level of output.

- Inflation has recovered from its crisis lows but remains depressed. The Consumer Price Index (CPI) grew by 1.0% year-over-year in July. The deflator on personal consumption expenditures (PCE) grew by 1.0%, and by 1.3% on a core basis (excluding food and energy). We expect prices to recover some ground as demand returns, but the economy does not have a foundation in place for rapid inflation.

- At the annual Economic Policy Symposium at Jackson Hole, Federal Reserve Chair Jerome Powell revealed a reconsideration of the Fed’s inflation targeting framework. By allowing inflation to run above target and giving priority to a recovery in employment, any rate increases by the Fed are far in the future. The full impact of the policy change will not be felt until the economy is on a well-established growth path; the Fed will offer more detail at its meeting on September 15-16.

- Negotiations on further support for U.S. consumers and businesses appear to be at a stalemate, putting the recovery at risk. The end of the $600 weekly supplement to unemployment insurance payments presented a sizeable income loss; more than 29 million people are still receiving unemployment support, and initial claims remain elevated. Small businesses that received Paycheck Protection Program loans are still facing diminished demand. Larger businesses, notably airlines, are warning of mass layoffs. Further support is likely to come from Congress only as part of a 2021 budget agreement at the end of September, which may be too late to prevent some negative outcomes.

- Fiscal stimulus came at a cost. The Congressional Budget Office projected a federal budget deficit of $3.3 trillion in 2020, with total debt forecast to exceed 100% of GDP in 2021. While the U.S. remains creditworthy, and the intervention prevented worse outcomes, the high debt level will receive more attention for years to come.

- The housing market has been resilient in this crisis. Demand for houses is elevated by low interest rates and demand for larger spaces from families working and schooling from home. The CARES Act’s mortgage forbearance requirement remains in place through next March, and the Centers for Disease Control and Prevention have stopped tenant evictions as a public health measure; both of these are holding off a shake-up in the residential real estate market.

- Speculation about the November election is growing. However, the outcome will not change our forecast. The recovery from COVID-19 will continue to be the top driver of the economy, regardless of who wins the presidency or which party takes power in Congress.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2020 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures.