by Guy Davidson, AllianceBernstein

Over the years, individual investors have flocked to municipal bonds to meet safety, income and after-tax return goals. The recent coronavirus-driven liquidity crunch underscores that investors should also think carefully about how they gain exposure to the asset class.

Municipal Bonds Still Look Compelling

There’s no question that munis continue to play their tried-and-true role of tax-advantaged anchor to windward. Despite recent short-term turmoil, the municipal market’s profile—as measured by historical risk, return, risk-adjusted return (or Sharpe ratio) and diversification against stock-market downturns—remains attractive (Display 1).

Not only have municipal bonds provided a higher historical risk-adjusted return than stocks even before taxes, but they have also zigged when equity markets zagged—serving as a buffer when it’s needed most. And most munis offer preferential tax treatment.

Good financial health coming into the pandemic bodes well for the market’s long-term survival, as does municipals’ characteristic resiliency. Municipal bond defaults have been rare, thanks to factors like reliable revenue streams, the power to raise taxes and cut costs, and provision of essential services. Since 1970, the cumulative default rate for all municipal bonds was just 0.1%.

While yields are likely to remain low for a long time, munis should continue to offer individual investors relative safety and tax-advantaged returns.

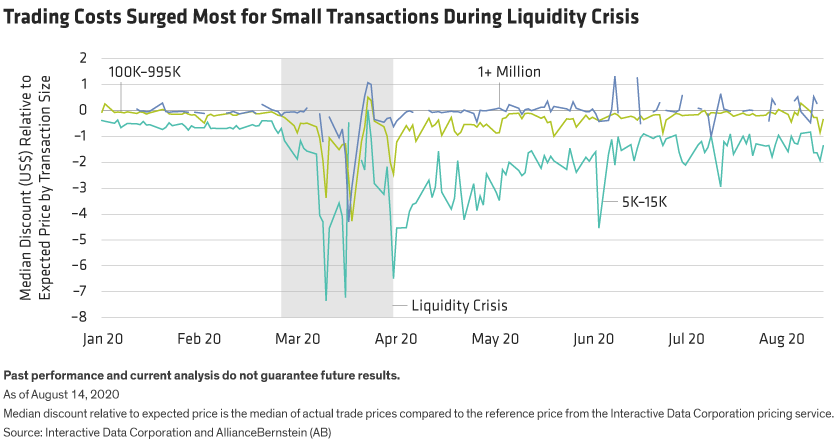

The Ebb and Flow of Liquidity

But what investors need to know about municipal bonds doesn’t begin and end with an attractive risk/return profile. Market liquidity also matters.

Unlike stocks that trade on a national exchange, bonds trade over the counter—directly with a dealer. Dealers commit their own capital to hold inventory or act as an intermediary to facilitate transactions. Instead of charging commissions on trades, dealers mark up the price of bonds when they sell them or offer less than fundamental value when they purchase them. This results in a transaction cost known as the effective spread.

The global financial crisis meaningfully changed liquidity in the municipal market. According to the Municipal Securities Rulemaking Board (MSRB), the number of municipal bond broker/dealers has declined almost 40% in the past 10 years. And the broker/dealers that remain aren’t committing much capital to municipal bonds. As of July 1, municipal bonds accounted for just 2% of broker/dealers’ market exposure.

Normal ebbs and flows in liquidity can become exaggerated when overall liquidity levels are low, and crisis strikes. Over the last few years, effective spreads had been dropping. But in March, when perceived risk ratcheted higher and a wave of selling hit the market, bond sellers received lower-than-expected bids, increasing the pain for those who needed to sell in an already down market (Display 2).

As fearful investors raised cash, the trading volume of municipal bonds climbed to twice the year-to-date average. Under such conditions, bid prices tend to disconnect from—and fall below—the fundamental value of the bonds involved.

Investors who exited their municipal bond positions during the crisis were hit twice, as large transaction costs cut further into already negative returns.

The Role of the Investor in Keeping Trading Costs Low

Municipal bond investors typically weigh their future liquidity needs, among other things, when determining an overall asset allocation. But we think investors should go further by considering their choice of investment vehicle.

As any warehouse store shopper knows, there are bargains to be had when buying in bulk, whether bonds or toilet paper. The cheapest trading costs are usually reserved for the largest trades. Safer trades—of bonds with higher ratings or shorter maturities—and less complex trades also see smaller effective spreads. Vehicles that pool assets to create larger trading blocks, for example, can take advantage of such dynamics.

Investors with sufficient liquidity outside their portfolio may be unlikely to sell portions of their muni holdings in the event of a crisis. These investors might consider a diversified portfolio of individual municipal securities, as market disruptions rarely have lasting return implications over the longer-term.

Unfortunately, individual investors forced to sell during disruptions may not only face higher transaction costs, but also lower-than-expected prices—a double whammy.

For muni investors who may need to raise cash from their bond holdings or who want to respond quickly to market conditions, at least some exposure to pooled investment vehicles—and their lower trading costs—may make sense.

Investors should work with their investment professional to determine the best municipal bond investment vehicle for their situation. When liquidity dries up, investors who took steps to control potential trading costs can be glad of one lesson already learned.

Guy Davidson is Chief Investment Officer of Municipal Business at AB.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

This post was first published at the official blog of AllianceBernstein..