by Susan Hutman, AllianceBernstein

US investment-grade corporate issuance has topped US$1 trillion year to date, putting it on track to plow through previous annual records. What are the real long-term effects of this explosive balance sheet growth? A closer look at net borrowing levels and why issuers borrow creates a roadmap of potential industry potholes to avoid.

Bonds, Bonds Everywhere

A trillion dollars in bond issuance in a matter of months is remarkable. The borrowing binge stemmed from a confluence of events, including coronavirus uncertainties, low interest rates, and the Federal Reserve’s expanded support of the corporate bond market. Issuance in and of itself isn’t good or bad, but sectors and industries that took on too much debt for their circumstances may face a tougher road post-COVID-19.

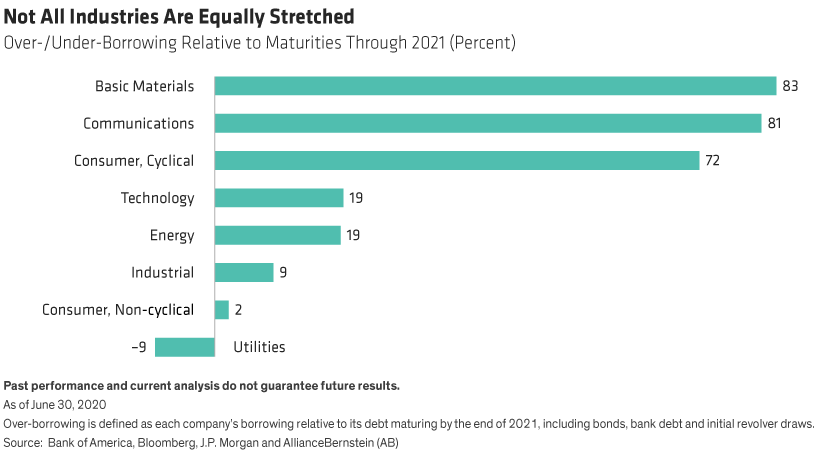

What do we mean by overborrowing? We compared how much a company has borrowed to the amount of its debt that matures by the end of 2021. The goal was to identify which companies may be opportunistically borrowing more than they need today to cover debts maturing in the next two years.

Rolling these numbers up gives us a look at which sectors may have overdone it with borrowing. In the basic materials sector, for example, companies borrowed over 80% more than they needed to retire upcoming debt (Display). Consumer noncyclicals, on the other hand, were much more judicious in tapping debt markets.

For companies that have overborrowed, it’s important to look at why they did so. Some companies were merely taking advantage of low interest rates to build a liquidity buffer, for example. Others used the debt to ramp up leverage or to act as a bridge to cover a period of negative free cash flow (FCF).

“Recapture Rate” Is Key to Post-COVID-19 Recovery

But knowing why a company overborrowed isn’t enough. The coronavirus lockdown significantly disrupted the economy, and to judge where this additional borrowing might cause problems, we need to understand each company’s ability to pay off this added debt over time. To do this, we created the recapture rate: a proprietary metric that measures the extent we expect sales to recover by the end of 2022 versus fiscal-year 2019 sales levels.

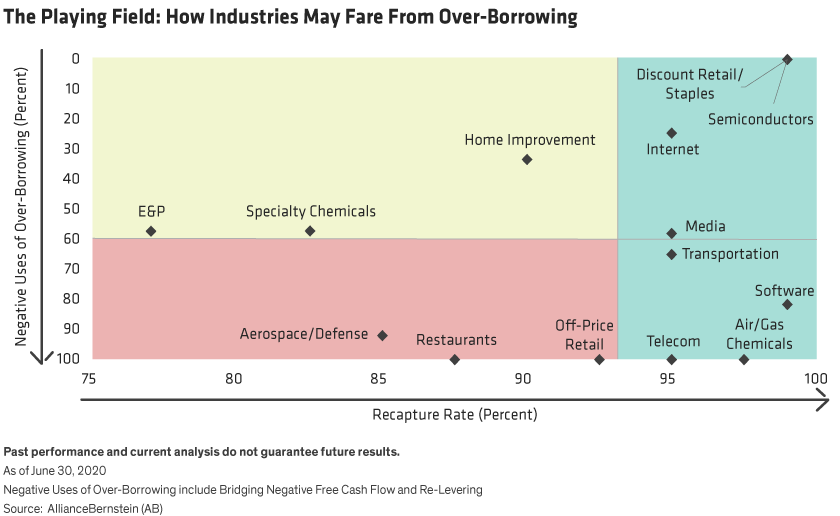

By combining the recapture rate and the reasons for companies overborrowing, we can identify which industries may be most at risk for trouble down the road (Display).

We believe that the greater a company’s need to borrow as a bridge to navigate a period of negative FCF, the harder it will be for them to recover to pre-COVID-19 levels. Even more critically, industries with low recapture rates—those likely to rebound the least from 2019 sales levels, and where demand is more flexible, may feel even more pain from overborrowing.

Strong Industries Likely to Stay Strong

In our analysis, over borrowers that didn’t need the money to fund operations and that have a high recapture rate are in the strongest positions, appearing in the upper right quadrant of the display. Not surprisingly, these include industries that either directly benefited from or are unaffected by the coronavirus crisis.

For example, both semiconductors and retail discounters/staples are strong industries with robust demand that aren’t hindered by the COVID-19 pandemic. In fact, new home offices, pantry stocking and toilet-paper hoarding created demand. These industries are also expected to bounce back well, with recapture rates of 95% to 100% or more. Most internet companies also fit into this category.

Finally, media companies, with their spotlight on advertising and entertainment, have high expected recapture rates, and we continue to view the industry favorably, for the most part.

For industries in the lower right quadrant, motivation for borrowing doesn’t appear to matter much. High expected recapture rates for all these industries suggest that they should be able to work down the incremental debt over our forecast horizon. Still, overborrowing in this quadrant was mostly done to re-lever or increase liquidity.

Industries on the Bubble

Overborrowing industries in the upper left quadrant, however, may require a closer look. If sales rebound faster than expected, they’ll have a shot at repairing their balance sheets as they work down the new incremental debt.

The home-improvement sector was classified as an essential business during the downturn, so as honey-do lists met stay-at-home boredom, sales were better than expected, leading us to believe the moderately high recapture rate of 90% may be a low bar. This industry did some practical re-levering and built up liquidity buffers.

For energy’s exploration and production (E&P) industry, the majority of new issuance is a liquidity buffer for large integrated oil companies. We’re much less constructive on independent oil producers. But while their issuance is mostly to cover negative FCF, the incremental liquidity should help the group weather current oil-price volatility.

Specialty chemicals rounds out this group, and while covering negative FCF accounts for only about one-third of issuance, the low expected recapture rate gives us pause.

Thar Be Dragons: Where the Risks Are Greater

We’re most concerned about industries that overborrowed primarily to subsidize negative FCF or to re-lever and that have lower recapture rates. These sectors fall in the bottom left quadrant of our display. We believe that balance sheet damage from incremental debt may be more lasting for these industries and may make it hard for them to dig out of the resulting hole.

The poor showing of the aerospace/defense industry largely reflects the troubles of one large airplane manufacturer experiencing extreme negative cash flow and cancelled orders. Travel shutdowns just made matters worse.

Off-price retailers who sell an ever-changing variety of branded merchandise at low prices, often bought at a deep discount from department stores, borrowed heavily to cover negative FCF. We expect this industry to struggle while the coronavirus-induced end to shopping-as-a-sport continues—and from a lack of e-commerce to bridge the missing brick-and-mortar sales. However, bargain-hungry shoppers should boost recapture rates once shopping eventually gets the all-clear signal.

Unfortunately for restaurants who overborrowed, recouping lost sales will be difficult, as few consumers will opt to eat two dinners per night in August to make up for those restaurant meals they couldn’t enjoy in April.

Follow the Map—but Look Company by Company

Record bond issuance creates outsized investment opportunity, but investors need to perform in-depth fundamental credit research to avoid potential potholes on their investing journey.

Industries that have overborrowed to take advantage of low rates and Fed purchase programs generally have an edge over those that borrowed to bridge negative FCF. A few industries may struggle, as overborrowing creates lasting damage to balance sheets.

Of course, it doesn’t make sense to paint every company with the same brush. In a post-COVID-19 world, investment-grade bond investors should study firms for potential overborrowing, examine why they took on more debt than maturities suggest they needed, and carefully consider their paths to recovery to pre-coronavirus sales.

Susan Hutman is Director of Investment-Grade Corporate and Municipal Credit Research at AB.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

This post was first published at the official blog of AllianceBernstein..