by Karen Watkin, AllianceBernstein

by Karen Watkin, AllianceBernstein

Higher-income assets underperformed in the second-quarter rebound. But that also means there’s pent-up potential in income-generating assets that may begin to show in later stages of the recovery.

The sharp rebound of global stocks and investment-grade bonds in the second quarter left higher-income assets behind. But that also means there’s pent-up potential in income-generating assets that may begin to show in later stages of the recovery.

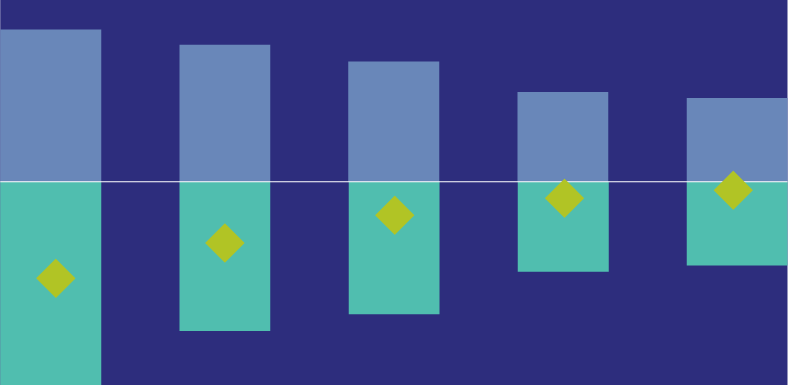

Investors are still deciphering return patterns of the coronavirus markets. In the first quarter, risk assets sold off broadly. Yet the rapid recovery in the second quarter was uneven. Growth stocks led, while income assets such as real estate investment trusts (REITs), high-dividend stocks and high-yield bonds posted much more modest gains (Display). As a result, REITs were still down by 21% in the first half of the year, and high-dividend stocks were down 13% as shown by the black diamonds above. Other equities recovered most of their losses while some even crossed into positive territory for the year to June 30.

Why Have Investors Shunned Income?

Concerns about income assets are understandable. Dividend payments are in question as earnings are squeezed, while high-yield issuers face higher default risks in a recessionary environment.

But history suggests that income assets take time to recover from systemic adversity. After previous crises, recoveries unfolded in stages, with each phase featuring different leadership. For example, after the global financial crisis (GFC), corporate bonds led at first while equities and REITs took a further step down. In later stages, equities were reenergized and a broader recovery developed.

What Could Spark a Stronger Recovery?

Today, we think income assets offer attractive return potential given current depressed valuations. Based on price/trailing earnings, high-dividend equity valuations are at the 35th percentile of monthly ranks over the last 10 years, while global equities trade near record high valuations. Even after credit spreads tightened recently, we believe high-yield issuers are still attractively valued. For example, as of June 30, US high-yield valuations were still in the 15th percentile of their 10-year monthly history.*

What would it take for income assets to recover? Since this isn’t a typical end-of-cycle recession, we believe a reopening of economies and an earnings recovery to support dividends could materialize faster than expected. While REITs suffered as lockdowns hit shopping malls and hotels, many property companies entered this crisis with lower debt and without the supply/demand imbalances seen before the GFC. Other REITs segments such as industrial and data-storage facilities, as well as multifamily residential complexes, were still seeing solid levels of rental payments from April to June.

Meanwhile, high-yield issuers should benefit from continued asset purchases by central banks, which help provide a backstop for credit; large amounts of issuance for refinancing and corporate use will also help companies shore up balance sheets and manage cash flows through tough conditions.

Since interest rates are expected to stay extremely low for an extended period to help combat the pandemic-induced recession, investors need to cast a wider net to find resilient income assets. With a selective approach, implemented in a diversified and flexible multi-asset portfolio, we believe investors can capture resilient sources of income at attractive valuations across an array of assets.

*Source: Bloomberg

Karen Watkin is Portfolio Manager, Multi-Asset Solutions at AllianceBernstein (AB)

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time. AllianceBernstein Limited is authorised and regulated by the Financial Conduct Authority in the United Kingdom.

MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein

This post was first published at the official blog of AllianceBernstein..