by Lance Roberts, Clarity Financial

Listen, I get it.

When markets are rising everyone wants to be bullish.

Why not? As Bob Farrell’s Rule #10 states:

“Bull markets are more fun than bear markets.”

It is also safer to be “always bullish.” No one remembers the guy that called the previous bull market peak as human psychology is designed to “mask pain.” If it wasn’t, women would never have children after their first one.

Despite the fact that many media commentators and pundits yelled “buy” all the way down in 2008, people only remember when the call to “buy” was eventually right. We like to “feel good,” and bull markets “feel good.”

Yes, 80% of the time the markets rise. It’s just the other 20% that’s a real bitch.

But “bear markets” are like “Fight Club” and the first rule of “Fight Club” is:

“Never Talk About Fight Club”

Last week, Eric Nelson, CFA, published an interesting article discussing predicted returns by Vanguard Founder, John Bogle. He starts by quoting Bogle from 2009:

“1) Beware of market forecasts, even by experts. As 2008 began, strategists from Wall Street’s 12 major firms forecast the end-of-the-year closing level and earnings of the Standard and Poor’s 500 Stock Index. On average, the forecast was for a year-end price of 1,640 and earnings of $97. There was remarkably little disparity of opinion among these sages.

Reality: the S&P closed the year at 903, with reported earnings estimated at $50.”

This is a fantastic point and a clear lesson that should be learned by all investors.

It is also Bob Farrell’s Rule #9:

“When all the experts and forecasts agree – something else is going to happen.”

Eric goes on.

“The irony of this advice, however, is that Bogle regularly makes forecasts about what stock returns will be going forward and how those will compare to historical returns. Now, you might find that peculiar, but not particularly upsetting. Except, what would you do if you learned that Bogle was predicting significantly lower-than-average future returns? Would you stick with your stocks or would you be tempted to consider safer bonds instead or even time the market?”

He is right. Given that Bogle is the veritable “Godfather” of “buy and hold” investing, it is a bit ironic he would discuss future rates of return.

But this is where Eric and I disagree a bit.

“How have Bogle’s forecasts held up? About what you’d expect based on Bogle’s prediction about the futility of forecasting! Through August 22nd, the DFA US Large Cap Equity Fund (DUSQX) returned +13.3% a year over the last five years and +15.2% in the previous three years.

Now, we don’t know what the next five to seven years will look like, but unless stocks have zero returns over this timeframe, Bogle’s forecasts will prove to be way off. His actual prediction over the decade beginning in late 2013 was for stocks to earn +97%. In the first five years, they’re already up +86%. His latest forecast, in 2015, was for stocks to make +48% over the coming decade. In the first three years, they’ve already eclipsed his forecast, up +53%!”

Hold on just a minute. Read that bolded part again.

In order to make a bullish case for owning equities, Eric assumes NO bear markets over the next 5-7 years (a year of 0% returns is not a bear market.)

If this happens, Eric will indeed be right.

However, historically speaking “bear markets” do tend to be a problem.

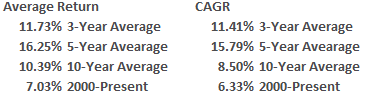

The chart below uses the S&P 500 Total Return Index (not adjusted for inflation.)

The average and CAGR (compound annual growth rates) for 3,5, 10, and 17 years are below. You will note that while post-recession performance has exceeded the 10% annualized growth rate target, once you start capturing “bear market” periods, longer-term returns fall quickly.

But let’s do a little math to see if Bogle himself might actually be proved correct.

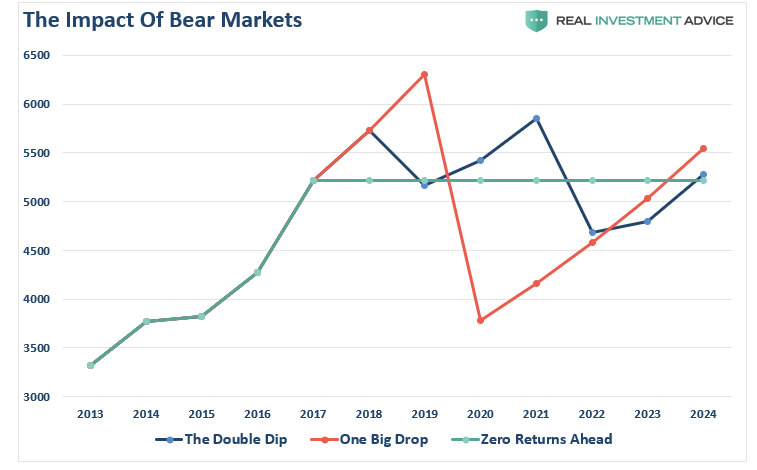

According to Eric the next 5-7 years will likely still provide elevated returns even if the market returns zero. The table and chart below show three different scenarios.

- Zero Returns Ahead: Follows Eric’s example of zero returns ahead.

- One Big Drop: Allows for 10% returns every year going forward with the exception of one 40% decline.

- The Double Dip: Looks at variable rates of return with a 10% and a 20% drawdown along the way.

As you can see, even if Eric is correct and returns are zero over the next 7-years, 3.52% returns are not anything to really write home about. Secondly, once you factor in the very high probability of a negative return year, or two, returns fall far short of the 10% annualized growth rate.

But here is the real kicker.

Once you trim off 2%, or so, for inflation forward returns range between 0% and 3% for the decade following 2015.

Which is just about where Jack Bogle suggested they would be.

This isn’t stock market forecasting.

This is just math.

As Michael Lebowitz noted:

“I struggle to grasp the point of using prior returns and expected future returns to arrive at an investment conclusion. Yes, I agree that if the market average return is 7% and I return 20% in years one through ten but 0% in years ten through twenty, the approximate 10% return was above average. The problem is the 20% returns in my example are in the rearview mirror. All that matters is what are the returns going forward and more importantly, how can I make them as favorable as possible. Relying on gains of years past all but assures that my outperformance of the past ten years will be erased.

Let’s put this into a sports metaphor.

The Washington Redskins coach feels assured he is going to receive a big fat bonus because so far his team is 8-0 and they are halfway through the season. However, over the next 8 games, they lose by 50 points each. Is his bonus intact? He had a commendable 8-8 season, but it won’t feel average when he’s looking for a new job.”

The takeaway?

Eric is correct when he concluded:

“We don’t know what stock returns will be in the near future, you should expect significant uncertainty, and results may not match historical averages.”

I also agree that you should not go making wholesale portfolio changes either.

However, expecting a decade-long bull market to continue uninterrupted for another decade is a dangerous proposition. This is especially the case given current valuations, extreme long-term technical deviations, tightening monetary policy and economic maturity.

As Bob Farrell’s Rule #2 states:

“Excesses in one direction will lead to an opposite excess in the other direction.”

That isn’t a market forecast either.

It is just historical fact.