by Russ Koesterich, Portfolio Manager, Blackrock

Value continues to look cheap, however predicting when it will begin to outperform is challenging. Russ suggests one potential catalyst: an unexpected acceleration in nominal economic growth.

The view that value looks cheap has become axiomatic; when value will actually start outperforming has been much harder to predict. Despite offering historically low valuations, at least relative to growth, value continues to lag. Year-to-date the Russell 1000 Growth Index has outperformed the Russell 1000 Value by over 11%.

Valuation gap

I last discussed this valuation gap in November. Since then it has only widened. Based on price-to-book (P/B), the Russell 1000 Value index has typically traded at around a 57% discount to the Growth Index. In November the discount was approaching 70%; today it is at 72%.

Does this suggest that value is even more of a “screaming buy”? Perhaps, but the timing is not obvious. The valuation gap looks less extreme depending on the exact valuation metric and time-frame. For example, although the current P/B discount looks out-sized relative to the long-term history, it looks less severe compared to the post-global financial crisis norm. Since 2010, value has traded at an average discount of 64%. In this light, current valuations appear less extreme.

You reach a similar conclusion by changing the valuation metric. Historically, based on trailing price-to-earnings (P/E), value has traded at a 25% discount to growth. Recently, stellar earnings growth has kept the P/E ratios for growth companies well below the nose-bleed levels of the late 1990’s. Today, value, based on trailing P/E trades at only a 32% discount to growth; larger than the historical average but not unprecedented.

Still waiting for economic growth to breakout

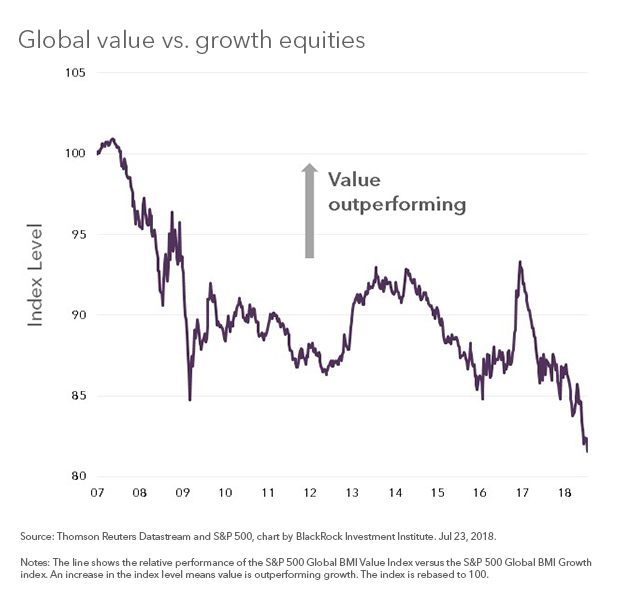

Beyond the question of relative value looms a second challenge: the lack of a catalyst. As I highlighted last November, you would have reached the same conclusion on value looking cheap at any point during the past three years. Yet, with the exception of late 2016 value has consistently under-performed over this period (see Chart 1)

The catalyst most likely to revive value is the same one that drove out-performance during the back-half of 2016: an unexpected acceleration in economic growth, particularly nominal growth. Unfortunately, as everyone now knows, nominal growth has failed to accelerate on schedule.

Despite a late-cycle tax-cut, first quarter growth of 2% was another disappointment. And while inflation has risen, so far it has been a gentle climb. The good news is growth, both real and nominal, should accelerate from here. The challenge is whether or not the acceleration will impress investors. What made the latter part of 2016 so ideal for value was the abrupt change in sentiment: investors went from panic over China to a U.S. tax-cut led euphoria in less than six months. In other words, economic expectations went from dismal to optimistic very quickly.

Bottom line

This time around expectations may be harder to beat. Unlike in early 2016, when China fears led many to expect another recession, expectations for growth have risen of late. According to Bloomberg, since last October consensus growth expectations have risen from 2.3% to 2.9%. For value to really start to outperform, economic growth may need to surge in a way we have not seen for some time.

Russ Koesterich, CFA, is Portfolio Manager for BlackRock’s Global Allocation team and is a regular contributor to The Blog.