by Martin Atkin, Managing Director, Multi-Asset Solutions Group, AllianceBernstein

Generating consistent returns under uncertain conditions is a challenge. Can multi-asset strategies make the job a little easier? We think so. But a lot depends on how they’re designed.

Institutional investors today are wrestling with strategic allocations in the face of a challenging environment. Expected returns for stocks and bonds are low. Regulatory oversight is increasing. There’s a massive industry shift from active to passive investment strategies. And additional investment objectives such as environmental, social and governance considerations are growing more important.

We think a flexible and well-diversified multi-asset approach can help. But there are a myriad of asset classes and strategies to choose from—traditional and nontraditional, active and passive, liquid and illiquid. There are also many approaches to designing such a solution.

In our view, a multi-asset solution has to do three things:

- Generate excess returns above an optimal mix of stocks and bonds

- Diversify an overall portfolio to ensure more consistent returns

- Limit volatility and protect investors against large drawdowns

But to be truly effective, multi-asset solutions need to be dynamically managed, unconstrained and fully integrated. Simply stitching together a number of single-asset strategies into one portfolio isn’t enough. What truly drives the returns of each building block? In which environments is it expected to be more effective or less effective? How do the pieces fit together and how do they alter the portfolio’s overall characteristics?

Assessing the Building Blocks: Historical Perspective

History is a good starting point in answering these questions—but it’s only a starting point.

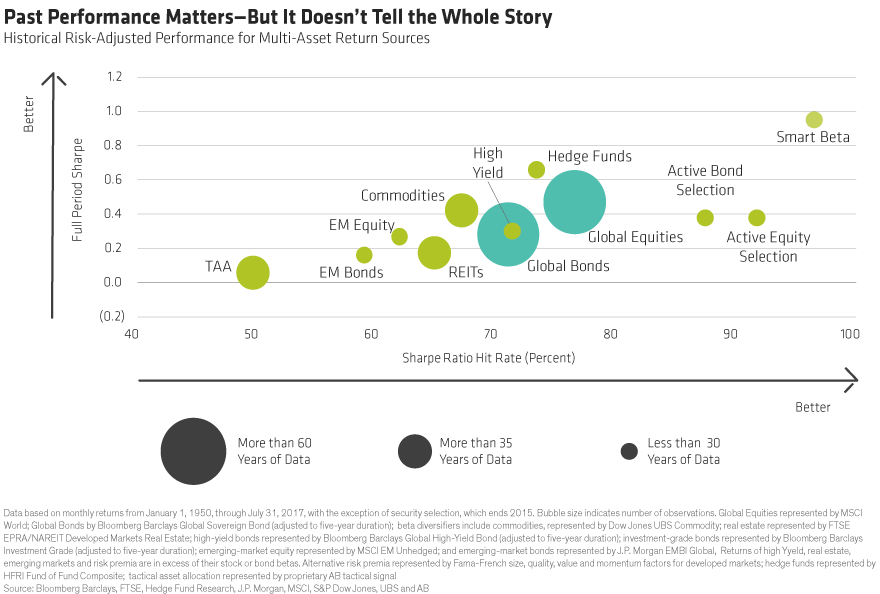

The following Display compares the historical risk-adjusted returns of several building block strategies and asset classes, as measured by their long-term Sharpe ratios, with their consistency of return—in other words, how reliable is that Sharpe ratio over a given time period?

Each bubble represents multiple asset markets and sources of return. Global equities and bonds include all developed-world stock and bond markets. Smart beta includes several alternative strategies, including equity factor strategies that rely on specific quantitative measures, such as momentum or value, to calibrate exposures.

The chart includes both return sources that rely on broad market exposure, or beta, and those that rely heavily on alpha, or manager skill, such as hedge funds and tactical asset allocation (TAA) strategies. Of course, there are also other ways to incorporate alpha into an investment framework. For example, investors might implement actively managed strategies that rely on security selection.

Global stocks and bonds—the traditional pillars of asset allocation—sit comfortably in the middle. The risk-adjusted returns for the other categories are measured by what they deliver above and beyond these crucial building blocks. For example, real estate investment trusts have exposure to equity and bond risk as well as risk that’s unique to real estate.

At first glance, quantitative strategies such as smart beta, which create value by allocating to certain risk premiums, have delivered the best combination of return and consistency. TAA strategies, which temporarily adjust a portfolio’s long-term target weights to take advantage of short-lived market opportunities are at the other extreme, with a poor showing.

Building the Framework Requires Both Science and Art

The Display also helps illustrate why empirical data is only a starting point, not an end point. Building a durable framework isn’t a hard science. Doing it well takes art.

Where does the art come in? To start with, history can be misleading, because few strategies have as long a track record as global equities and bonds, with a rich data set to back it up. That’s why the stock and bond bubbles are bigger—the bigger the bubble, the more available return data.

Smart beta strategies may seem like the most attractive building block based on their full history. But that history isn’t as long as that of stocks and bonds; smart beta hasn’t been through as diverse an array of environments. What’s more, the strategies saw two decade-long periods with very different return experiences: an annualized return of 6.6% from 1997 to 2007, but one of just 1.2% from 2007 to mid-2017.

TAA strategies, on the other hand, may seem like the least compelling investment in the Display, but they’ve actually been extremely helpful during periods of severe market stress. They provided important ballast during the bursting of the dot-com bubble and the global financial crisis. Between 2000 and 2009, TAA strategies produced an annualized return of 3.4%; global stocks were down 3.3% over the same period.

An understanding of the true return drivers of these building blocks and how they behave in different environments is critical in setting forward expectations. Based on recent history, for instance, investors might decide to de-emphasize inflation-sensitive assets, because inflation in the developed world has been unusually low for decades. But that could change, and inflation assets might prove valuable again.

The lesson here is clear: over the long run, investors looking for consistent returns and reliable downside protection would have wanted exposure to all these return sources—even those that at first glance may not seem to bring much to the table. Those building blocks also need to be integrated carefully and managed dynamically as market environments evolve.

Note: Data was developed by Defne Ozaltun and the AB Multi-Asset Solutions research team.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

Copyright © AllianceBernstein