by Lance Roberts, Clarity Financial

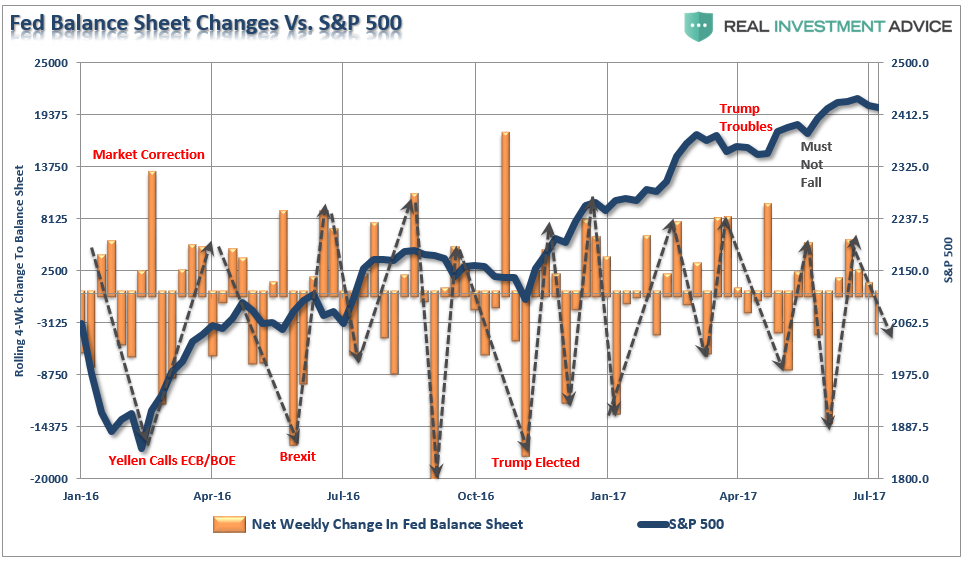

Since the end of the financial crisis, each market decline has been met with support by the Federal Reserve either through “verbal accommodation” or directly through “monetary interventions.”

Not surprisingly, investors have become “trained” each “dip” in the market is a reason to “buy” even in the areas with the least fundamental quality. The perception of “risk” has been entirely eliminated which has once again brought about a sense “this time is different.” Of course, this is not unusual as we have seen it at each major bull market peak throughout history.

“But Lance, the Fed’s balance sheet has been flat since the end of QE-3, but the markets continue to rise. So, that is clearly a sign of a recovering economy and earnings at work.”

Not so fast.

The Fed’s ongoing “reinvestment program” has been very successful at facilitating support precisely when it seems to be needed most.

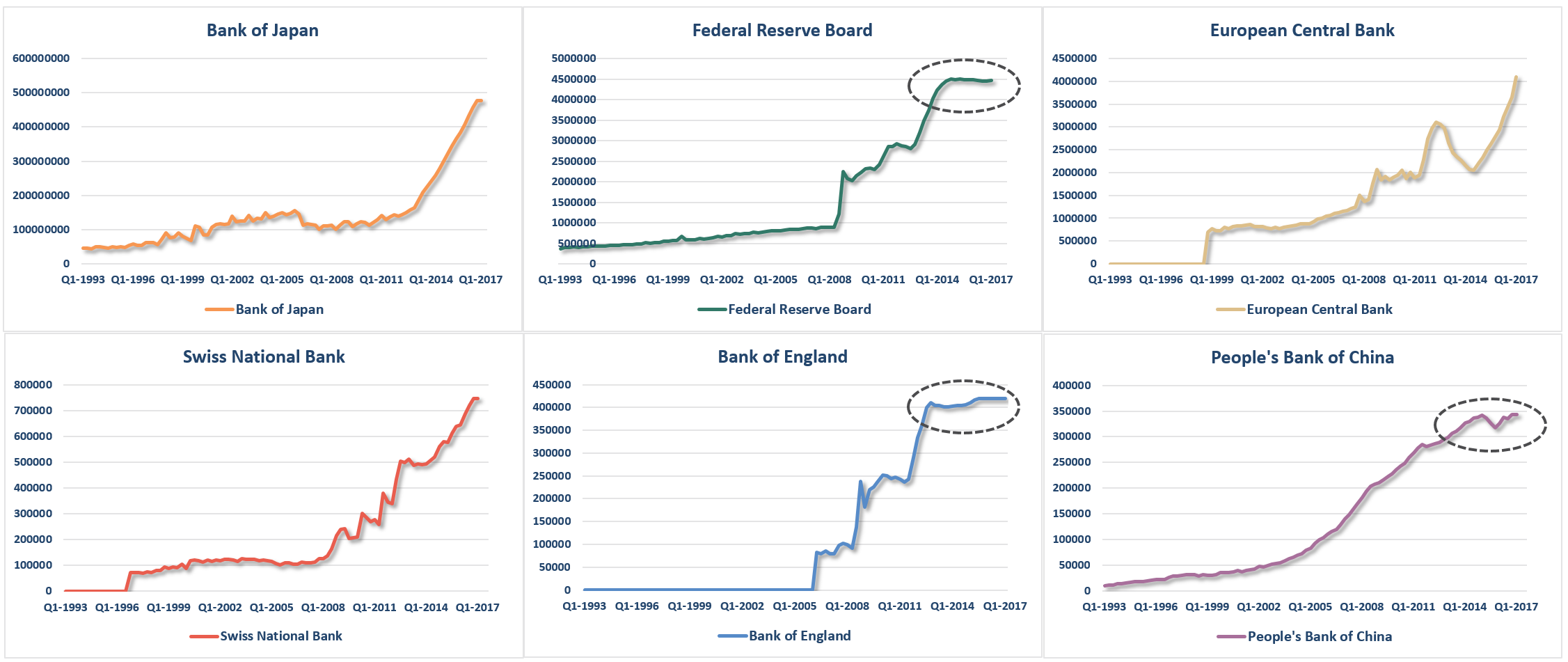

Of course, as noted above, global Central Banks have also been extremely accommodative of support asset markets as well.

This is nothing new, just a reminder this isn’t “your father’s market,” and assuming the market is functioning based on underlying fundamentals is a bit short-sighted, to say the least.

The problem, however, comes when the Fed begins to stop those reinvestment processes. As shown above, where support has been previously provided to offset potential declines, such support will no longer be available. Such will eventually return the view of the markets back to the fundamentals. It is there we find more troubling issues.

The table below from Goldman Sachs shows a variety of measures of current valuation. With the exception of Free Cash Flow, every other measure suggests investors are “over paying for playing” currently.

Economically, the metrics also suggest that we are very near the end of the current bull market cycle. The chart below shows the percentage change in inflation, GDP, employment and interest rates leading up to each of the last two recessionary breaks in the market.

Importantly, note that falling inflationary pressures tend to have an adverse effect on economic growth. This suggests, just as it did both times previously, the recent uptick in economic growth will likely prove to be very transient.

So, Do I “BTFD” Or What?

As I stated two weeks ago:

“My best guess currently is – probably. But not yet.”

I also stated two reasons for why we should wait:

- Bull markets don’t typically end when the mainstream media is “peeing down both legs” over the 1.5% drop on Thursday.

- The bullish uptrend remains intact and “fear” gauges remain confined to a downtrend.

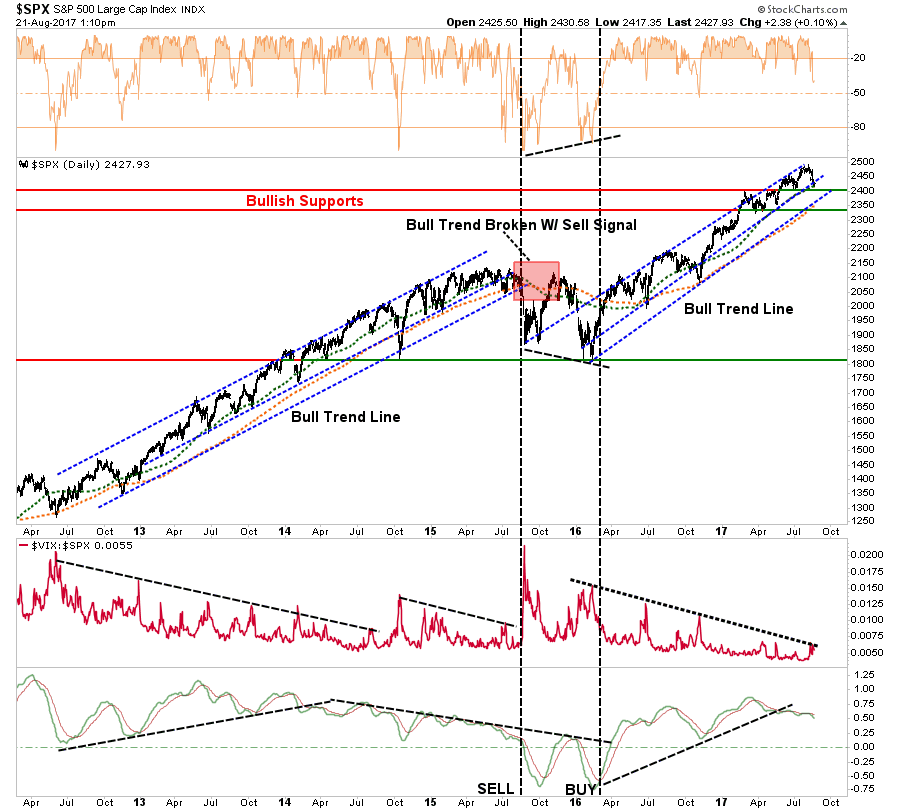

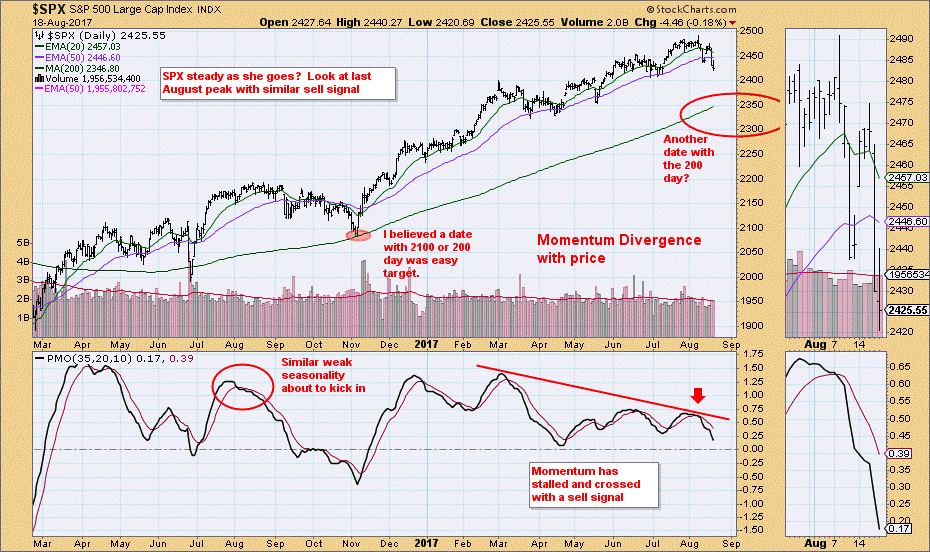

The chart below goes back to the beginning of the bull market advance following the 2012 correction. Notice that while the market remained in the QE backed bullish advance, volatility remained confined to a downtrend with the brief exception the “taper tantrum” in October 2014.

However, notice the bottom part of the chart.

Following the 2011 “debt ceiling debate” correction, the bull market resumed with the help of the Federal Reserve interventions as noted above. However, beginning in 2014, that trend became negative as the “momentum” of the advance began to stall as the Federal Reserve withdrew its direct liquidity interventions into the markets. Eventually, that deterioration in price momentum led to a bigger correction and a break of the “bullish trend” in late 2015 and early 2016.

Currently, the market has triggered a short-term “sell signal,” which suggests the corrective process is not yet completed. Therefore, investors are wise to remain a bit more cautious currently until markets re-establish a more “bullish footing.”

Hedge Fund Telemetry sent out a very interesting note on Monday which supports my suspicions:

“Sentiment has decreased to 40% bulls for the S&P 500 (the lowest since 11/16/16 when it was increasing from a low of 10% the day after the election). It’s now firmly below the midpoint level support. This partial eclipse of the bulls only has seen the S&P drop about 2.50%. Could there be a “catch down scenario” in price? (Price accelerating to the downside) Very possible. I’ve been cautious of late (a little more cautious than usual) due to the weak seasonality, divergent sentiment, and some overbought indicators on major indexes. Today I’m making the case for more downside risk. There are some very basic indicators that are not yet oversold and in some sentiment factors not even close to other bottoms. I would continue to reduce risk across portfolios.

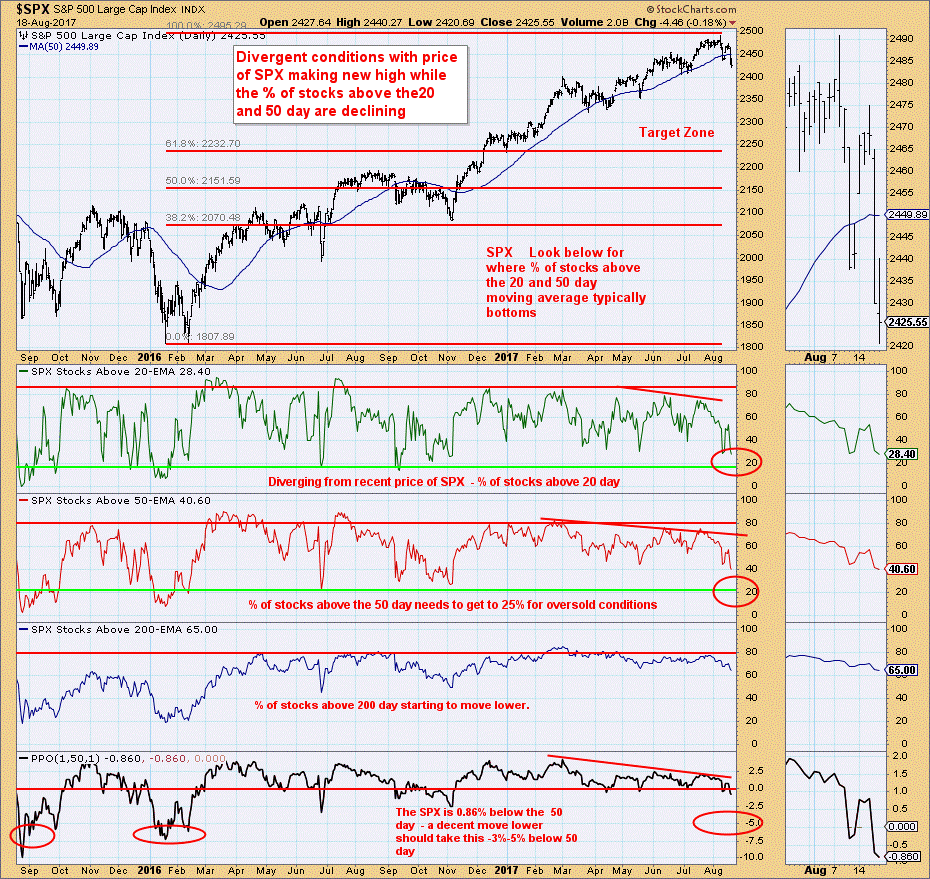

This chart shows the % of stocks within the SPX above the 20, 50, and 200 day moving averages and targets for when the market is oversold. The middle one % above the 50 day is the most important and it’s only at 40% above and a move to 20% is a better place to look for a bottom. Note, I’ve been showing the negative divergences for weeks now.”

“Here’s a simple momentum chart that also has diverged. I think a date with the 200 day is likely again”

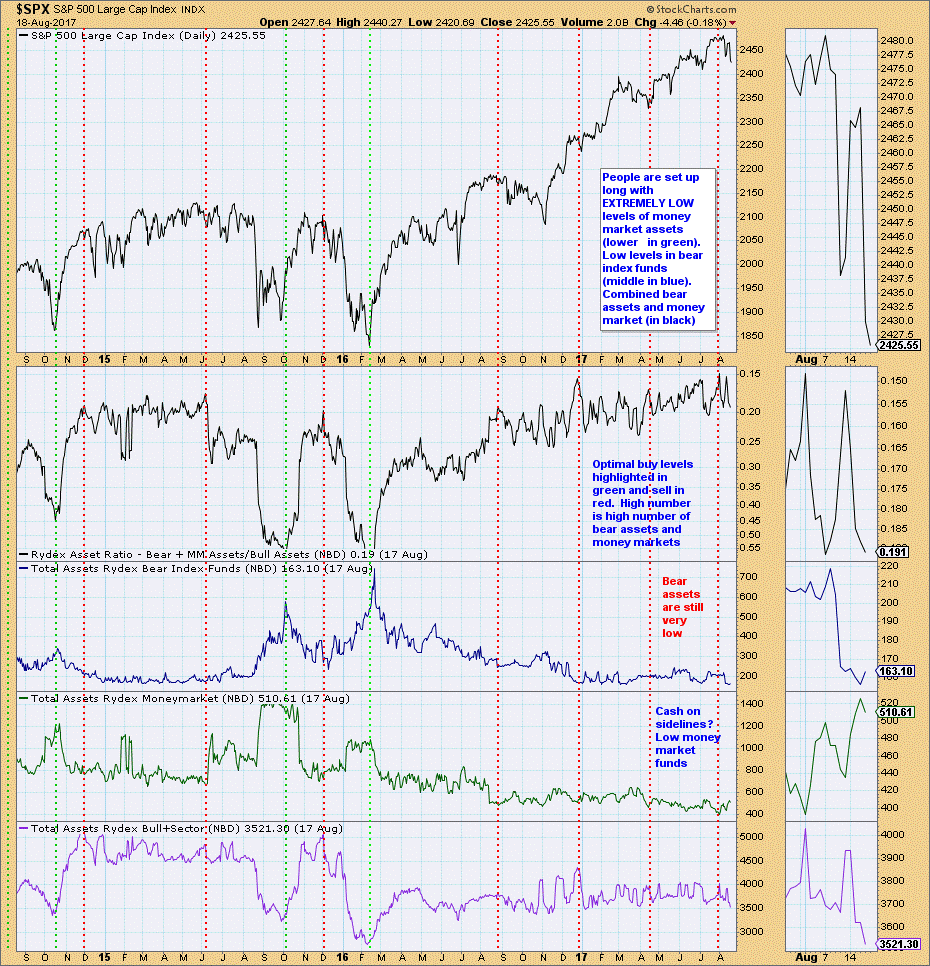

“This chart shows Rydex Mutual Fund data. Historically bottoms have been made with % of bearish assets spiking and cash levels increasing. This hasn’t happened at all yet.”

As stated, it may be prudent to employ some patience before taking any further action on the equity side of the ledger. However, in the short-term, the bullish bias remains “alive and well” which keeps portfolios cautiously allocated to equity risk.

The Biggest Risks

It is not just the same “deterioration” in the underlying technicals giving us caution.

While the market does remain confined within its overall bullish uptrend, the “bulls” should not continue to ignore the mounting risks of valuations, deterioration of reported EPS growth, weak revenue growth, slowing economic growth and fading realities of positive legislative agenda coming to fruition.

It is the last part of that sentence that is most prevalent.

As Ray Dalio noted on Monday:

“Politics will probably play a greater role in affecting markets than we have experienced any time before in our lifetimes but in a manner that is broadly similar to 1937.

History has shown that democracies are healthy when the principles that bind people are stronger than those that divide them, when the rule of law governs disputes, and when compromises are made for the good of the whole — and that democracies are threatened when the principles that divide people are more strongly held than those that bind them and when divided people are more inclined to fight than work to resolve their differences. Conflicts have now intensified to the point that fighting to the death is probably more likely than reconciliation.

In other words, the majority of Americans appear to be strongly and intransigently in disagreement about our leadership and the direction of our country. They appear more inclined to fight for what they believe than to try to figure out how to get beyond their disagreements to work productively based on shared principles.”

Those divides are also weighing on Washington D.C. where the ongoing partisan conflict between the Republicans and Democrats has stalled the ability for progress to be made on any legislative front. As Congress returns to Washington after their summer recess here is the immediate list of work that must be accomplished.

- Debt Ceiling Limit Increase (50% chance of a Government shutdown currently)

- 2018 Budget – (Will most likely be resolved by another “continuing resolution” that increases government spending by 8% annually.)

- Tax Reform – (There is a small possibility tax reform will be passed in the House but will die in the Senate)

- Tax Cuts – (Tax cuts will be proposed at 20-25%, overall plan will fall short of expectations and likely fail passage in the Senate.)

- Infrastructure Spending – (Has the best chance of being passed but will likely face a tough uphill battle.)

- Health Care Repeal / Replace – (DOA)

This is THE problem for the market which has priced in massive earnings growth expectations based on tax cuts and reforms. Without the Affordable Care Act being repealed, any tax cuts or reforms passed by legislative action will have to clear $900 billion just to offset the taxes that weren’t repealed previously. This alone with negate much of the economic benefit from the legislative agenda.

Furthermore, considering that all legislative action has to be passed through “reconciliation,” the Republican controlled Senate faces a tough battle with only has a 52-vote margin currently. With the ability to only lose two votes, and all agenda items required to be “revenue neutral,” this makes the passage of tax cuts/reforms even MORE difficult than the failed attempt at trying to repeal/replace the ACA.

There is a reason there has not be “tax reform” passed since Reagan was in office.

In other words, the risk of disappointment is extremely high.

In recent years, “market tantrums” have been short-lived and have provided opportunistic entry points for increasing equity related exposure. However, EVERY TIME is DIFFERENT, so it is always important to NEVER ASSUME the outcome will be the same as the last.

In our portfolios, we continue to wait for confirmation the current sell-off has abated before adding additional risk exposure to portfolios.

Copyright © Clarity Financial