by Carl Tannenbaum, Asha Bangalore, Ankit Mital, Northern Trust

As recently as a week and a half ago, we were comfortable with our prediction that the Federal Reserve would wait until the middle of the year to take the next step in normalizing U.S. monetary policy. There seemed to be no immediate prospect of an increase, and the Fed has been exceptionally cautious over the past few years.

But since the beginning of March, a remarkably well-orchestrated string of Fed speakers has made it clear that there will be an interest rate increase on March 15. Because it occurred during a slow period in the economic calendar, this change of tone was not based on new data. So what prompted the increased urgency?

In our view, there are two main reasons. First, asset prices have risen into territory that might cause concerns about financial stability. And secondly, the Fed was deterred from acting several times last year because of international uncertainties. Today, we are in a period of relative calm, but upcoming events in Europe threaten to disrupt the peace. The central bank seems to want to take advantage of this window of opportunity.

Here is our take on the likely content of next week’s conversations.

Much of today’s discussion surrounding business activity centers on “animal spirits.” Economic actors seem to be upbeat about the quarters ahead; if they act on this impression, it can become self-fulfilling.

History suggests, however, that confidence readings do not always presage movements in broad economic trends. And if the sources of optimism are ultimately not realized, spirits might sink. Our forecast for growth of around 2% after adjusting inflation, which matches the Fed’s most recent projections, does not create a sense of urgency for monetary policy.

Progress on the administration’s economic agenda has been slow. For procedural reasons, attention has turned first to reform or repeal of the Affordable Care Act (ACA). This has proven to be far more complicated than some had thought; few Republicans want to sustain much of the current system, but none want to be responsible for dismissing 20 million Americans from the insurance rolls. An alternative to the ACA was finally proposed this week, but has not yet met with broad support.

Getting reforms in place may become even more challenging. Deficit hawks will not want to see the budget deficit expand much, if at all. But paying for proposed tax cuts and infrastructure spending cannot be achieved merely with reductions in discretionary federal spending. (There isn’t much left to cut, see here.) The “border tax” has the potential to raise a lot of revenue, but also create a lot of economic disruption.

Reality may force delays in passing pro-growth legislation and diminish its size. The up-side risk to U.S. economic growth and inflation may not be as large as some might think.

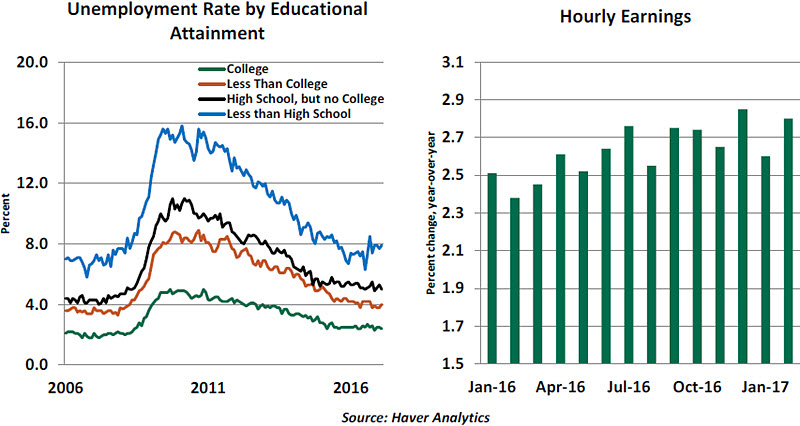

The February employment report showed widespread gains in hiring, with both goods and service sectors accounting for the overall increase. The 3-month average of payrolls at 209,000 is more than adequate to hold the jobless rate steady. Although hourly earnings regained strength, employment compensation is mostly stable and awaiting additional acceleration at the late stage of the expansion.

The unemployment rate dipped to 4.7% despite an increase in the labor force, a noteworthy development. Broadly speaking, the Fed’s full employment mandate has been met.

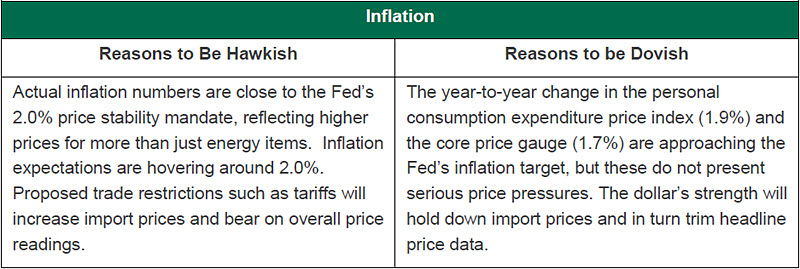

The Fed needs to be forward looking as policy changes affect economic activity and inflation with a lag. The price stability target is within reach. Delaying monetary policy tightening would require more aggressive hikes in the policy rate that will eventually be harmful to economic growth. Given that both the full employment and price stability mandates are nearly satisfied and the implicit financial stability goal is in place, the Fed’s credibility will suffer if it fails to take action against inflation now.

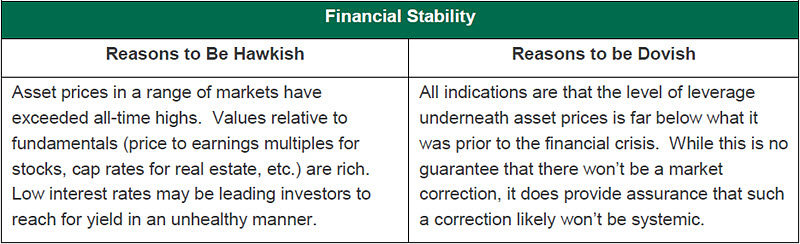

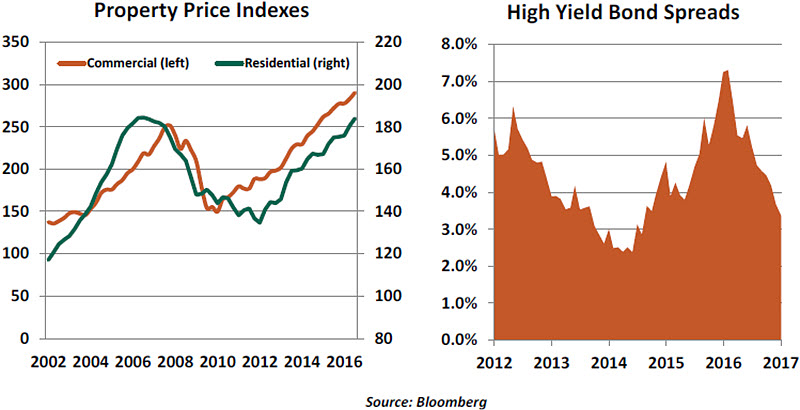

Record equity indices have certainly attracted a lot of attention, but that isn’t where the story ends. Commercial and residential property has also done exceptionally well; perhaps too much so. The Fed has issued a string of warnings about real estate, which it may choose to reinforce by making financing more expensive.

Further, compensation for credit risk in the market has fallen dramatically; spreads on high-yield debt are below their levels of three years ago, just prior to the bust in oil prices. (Many high-yield debt issuers came from the energy sector, which encountered challenges that caused it to correct severely.) Measures of market volatility are low, belying the myriad of risks present in the outlook. The Fed may find value in cooling things off just a bit.

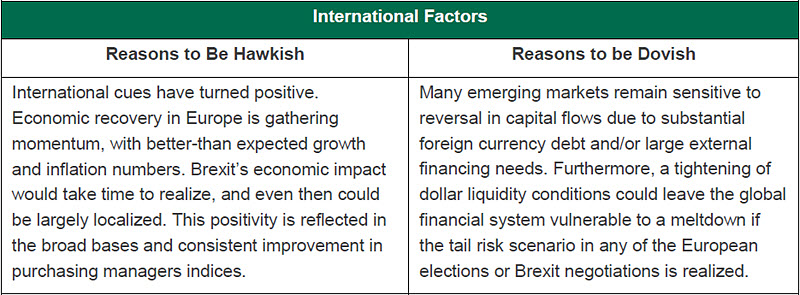

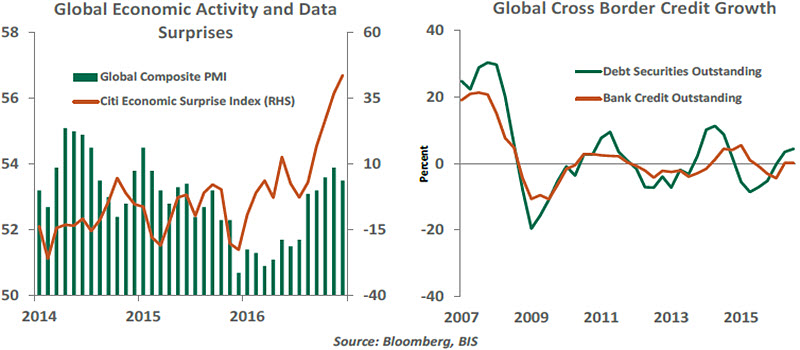

Recent economic data coming out of developed markets gives reason to be optimistic about the future. It could be argued that soft data — such as economic sentiment or consumer confidence — might be getting ahead of the hard data, but the data has been certainly surprising on the upside. The European recovery has even prompted talks of an earlier than expected monetary policy normalization from the European Central Bank. Across the Channel, growth in the U.K. has held surprisingly well in the aftermath of the referendum, forcing upward revisions of forecasts. It is now clear that the economic damage from U.K.’s divorce from the EU would be spread over a long period and even then it would be largely localized.

Of course, some emerging markets remain sensitive to shifts in global capital flows and could see external debt servicing costs rise (via both rising interest rates and stronger dollar). International credit growth is already tepid and higher funding costs could prove to be a headwind to growth. Furthermore, the global financial system is vulnerable to low-probability but high-risk political events in Europe and could do without tighter liquidity conditions. However, it is important not to overstate these vulnerabilities. On balance, the global economy is strong enough to withstand a more hawkish Fed.

Summary

Some have suggested there is urgency within the central bank to move the tightening process along before the White House appoints new governors to the Federal Reserve Board. This suggestion contends that with the federal debt likely to expand in the years ahead, the administration might favor candidates who would hold interest rates down. But we do not give much credence to this view, especially since many Republicans have been arguing for higher interest rates.

Speculation has already turned to what the Fed might do after March. Of the predicted three rate increases in 2017, we tentatively forecast the remaining two to occur in September and December out of consideration for potential mid-year international volatility. Of course, the Fed will provide a glimpse at its future intentions through the summary of economic projections that will follow the upcoming meeting.

We’ll have coverage of the Fed’s decision next Wednesday afternoon.

*****

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2017 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures.