Are Central Banks at the End of Their Effectiveness?

by Carl Tannenbaum, Asha Bangalore, Northern Trust

My teenage daughter now spends many Saturday evenings with her boyfriend. There is a protracted negotiation that precedes these dates: "Can I take the car?" "Can I have some money?" "Can we 'hang out' in the basement when we get back?" I am OK with the first two, but the last one is pushing things too far.

It's hard to know when you've gotten the best deal you can; when pushing things further is counterproductive to your cause. This is the challenge facing the world's central banks today. There is a growing sentiment that monetary authorities are essentially out of resources to address economic sluggishness and that soldiering on could make things worse and not better. It is always important to calibrate policy carefully, and it is clear that central banks need more assistance from fiscal policy. But it would be a mistake to abandon the cause of reflation now - and a disaster to admit defeat.

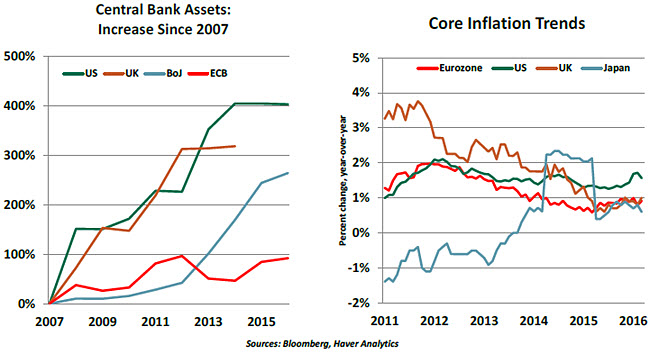

The first quarter of 2016 was not robust from an economic standpoint. Growth in developed markets progressed at an annual rate of less than 1%, and inflation remains well below targeted levels. This performance must be disappointing to central banks, which have employed a range of nontraditional strategies in an effort to spur economic activity.

It certainly appears that the effectiveness of these tactics is diminishing. Studies of the U.S. experience find that early rounds of quantitative easing (QE) had the desired effect, but the incremental influence of QE on interest rates, currency values and market levels has diminished. The Bank of England was early to this realization, closing additions to its QE program at the end of 2012. The Bank of Japan (BoJ) may have tacitly acknowledged this fact when it declined to announce new measures at its policy meeting last month.

Extending QE places central banks in an uncomfortable position. They own commanding shares of government bond markets and face accusations of monetizing sovereign debt. Further, central banks have had to venture into ever-more-exotic asset classes to sustain their QE programs. The European Central Bank (ECB) is now buying corporate bonds, and the Swiss National Bank (SNB) owns equities. These holdings bring unique risks and expose the central bank to claims of favoritism toward the companies or industries represented in their portfolios.

Extending QE places central banks in an uncomfortable position. They own commanding shares of government bond markets and face accusations of monetizing sovereign debt. Further, central banks have had to venture into ever-more-exotic asset classes to sustain their QE programs. The European Central Bank (ECB) is now buying corporate bonds, and the Swiss National Bank (SNB) owns equities. These holdings bring unique risks and expose the central bank to claims of favoritism toward the companies or industries represented in their portfolios.

The scale of global QE operations has also generated a heightened level of political attention, which monetary authorities typically try to avoid. The longer that activist monetary policy is sustained, the greater the risk will be to central bank independence.

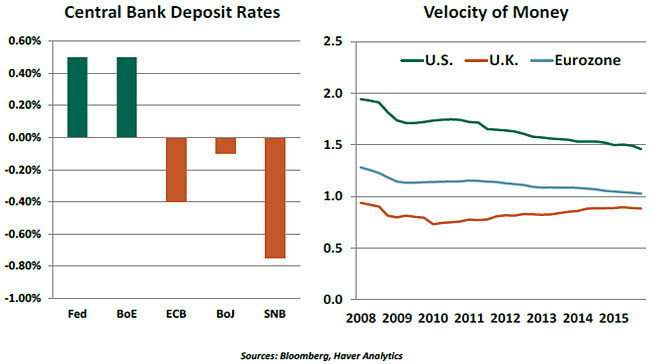

Central banks have tried negative interest rates. It's still early days, and rates aren't that deeply negative. But it already appears that this strategy is not producing the desired effect. Banks in Europe have been reluctant to push their own deposit rates into negative ground for fear of confusing customers or prompting them to flee. This limits the translation to lending rates and thereby limits the benefit to economic activity.

And the problem with credit flow may not be supply but rather demand, leaving central banks "pushing on a string." As shown below, the velocity of money is very low at present, suggesting that the translation of new reserves into new lending has been limited.

If sustained, negative interest rates could have adverse consequences for pension regimes and life insurance companies. These structures have made long-term promises that become more valuable in low interest-rate environments, at exactly the time that asset returns are diminishing. Very low or negative rates disadvantage small savers and those in debt, exacerbating the economic inequality that has driven global politics this year.

Acknowledging the limits of negative interest rates and QE, authorities are considering "helicopter drops" of money to stimulate activity. (Ben Bernanke weighed in favorably on this topic in a recent blog.) But getting funds into the hands of consumers isn't as easy as chartering choppers. It would require legislatures to approve and arrange the distribution; given the current political climate, this may be a tall ask.

Even those within central banks sense that monetary policy may have reached the edge of its effectiveness. Some of the core problems with economic function today are the result of fiscal, labor, education and trade policies that central banks cannot influence. ECB President Mario Draghi pleads at his press conferences for structural reform and deficit spending but has little sway with national legislatures.

All of this has led to calls for central banks to cease and desist. (Or even to admit defeat and begin a retreat.) But this could be a major error.

Firstly, it is difficult to gauge how effective recent monetary policy has been. As tepid as growth has been recently, it could have been a lot worse if not for central bank support. Gauging the difference between what actually happens and a hypothetical is very hard to do.

Firstly, it is difficult to gauge how effective recent monetary policy has been. As tepid as growth has been recently, it could have been a lot worse if not for central bank support. Gauging the difference between what actually happens and a hypothetical is very hard to do.

Secondly, much of what central banks have done since 2008 is intended to steer expectations, so that their actions aren't blunted by fear that they will be retracted in short order. There is a vast body of research that finds committing to a policy for the long-term produces maximal influence; abandoning that commitment could produce an unpleasant market correction.

Finally, it may very well be true that fiscal steps need to take the lead from here in pursuing better economic outcomes. But the likelihood of those passing in this age of austerity is slim. Sensing this, central banks may be justified in pressing ahead, even if it is risky.

At times, my daughter presses to a point that is suboptimal. Last week, she wanted financing to see a movie with her beau. We declined: too risky. Public, well-lit venues with lots of security cameras are what we are after.

Job Growth Slows, Wages Move Up

The April employment report sent mixed signals. Details suggest that data are not weak enough to change our Fed call of a June monetary policy tightening.

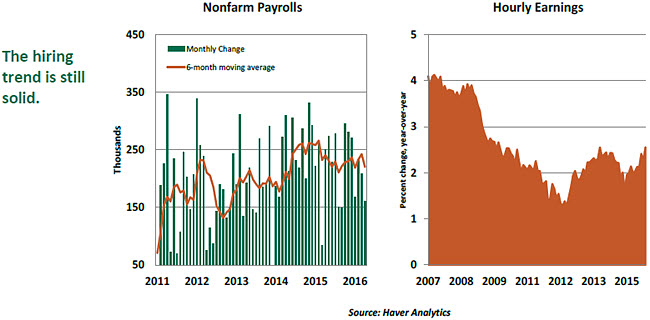

The unemployment rate held steady at 5.0% in April, reflecting a drop in the labor force, which brought down the labor force participation rate two notches to 62.8%. Employment as measured by the household survey recorded a big decline (-316,000) after solid gains in the each of the last six months. The household survey numbers for employment are reputed for volatile movements, so opposite movements may be expected in the months ahead.

On the positive side, part-time employment fell, the share of long-term unemployment slipped (25.7% versus 27.6%), and the broad measure of unemployment dropped one notch to 9.7%. Payroll employment advanced 160,000 in the establishment survey; this headline reading is the smallest since September 2015. Downward revisions to estimates of the past two months reduced the job count by 19,000. The three- and six-month moving averages of new jobs created are 220,000 and 200,000, respectively. These numbers are well above what is required to keep the unemployment rate steady.

Hiring increased in the professional and business (+65,000), health care (+44,000) and financial sectors (+20,000). Declines in employment in the retail, government and oil-related components offset part of the strength.

Hourly earnings rose 0.3% in April and put the year-to-year increase at 2.5%, a break from the muted 2.0% trend seen for several quarters.

Markets and analysts are reducing the probability of a June change in the Fed's policy rate based on today's report and the weakness seen in the first-quarter gross domestic product report. However, the positives are being downplayed. Auto sales recovered in April, and the latest Institute for Supply Management surveys of manufacturing and non-manufacturing sectors sent positive signals. If incoming retail sales, May employment data and inflation are not weak, the data-dependent Fed will have enough evidence to give serious consideration to a policy change at the June meeting.

Shades and Tones of Labor Market Developments

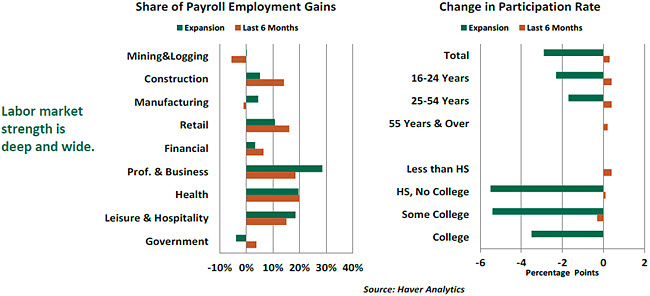

There are about 12.9 million more jobs today than there were in June 2009 when the recovery commenced. This count is useful, but it misses nuances regarding the types of jobs created and which groups of people returned to the labor market. Granular data about the sustained increase in hiring and the labor force participation rate (LFPR) paint a more-informative picture of labor market developments.

Hiring trends across major categories of employment reveal that job growth varied. The professional and business services category recorded the largest share of jobs created during the entire expansion, and it stood in second place during the most recent six-month period.

Health care employment ranked at the top with the highest payroll growth during the six months ended April and comes in second place for the entire recovery. Not only did these two categories account for almost 50% of job growth in the upswing of the current business cycle, but employees in these sectors are relatively highly paid.

The housing sector was the epicenter of the financial crisis, and recovery has been slow on several fronts. Hiring gains in the construction industry are not stellar, as only a little over 5% of new jobs in the past seven years occurred here. The share rose over the last six months and implies that momentum in this industry has turned around.

The LFPR is another aspect of the labor market that we are watching closely. The LFPR is the civilian labor force (number employed and unemployed) as a percent of the civilian non-institutional population. The LFPR peaked at 67.3% in 2000, and it mostly maintained a downward trend until recently.

The aging of the population explains a significant part of the decline in the LFPR. At the same time, the Great Recession intensified the downward trend as people left the labor force. In other words, structural and cyclical factors influence LFPR. Disentangling the influence of these two factors is challenging.

The LFPR moved up to 62.8% from a low of 62.4% in September 2015. People drop out of the labor force if they are unable to find a job or if they are discouraged, which leads to a reduction of LFPR. About 4.7 million were not in the labor force (not counted as unemployed) but were available to work in December 2007 and made up 2.0% of the population. This group expanded to about 7 million by 2012.

Economic growth brought back people into the labor force and reduced the tally to around 6 million by mid-2015, and it declined further to nearly 5.8 million in April. This change nudged the LFPR up across different age groups and educational attainment levels, which is consistent with labor market tightening.

How much the LFPR will improve is unclear, as it depends on a host of factors. The share of people not in the labor force but available for work is 0.3 percentage points higher today compared with the pre-recession reading in 2007, implying there is room for an increase. However, the nation's demography will continue to exert downward pressure.

Given the current political climate, it has become popular to suggest that the labor market data are very misleading. (Some even suggest that they are being manipulated purposely.) While a look beneath the surface certainly reveals some areas progressing more slowly than others, it is also clear that the job market is doing a better job than some suspect of reaching those formerly left behind. Let's certainly hope that continues.

Copyright (c) Northern Trust