by Russ Koesterich, CFA, JD, Portfolio Manager, BlackRock

In this article, Russ Koesterich discusses how momentum and election cycles may shift the impact and timing of seasonal trends.

Key takeaways

- YTD stock returns have been driven by earnings growth, supported by a resilient economy. That said, traditional seasonal factors would indicate caution in the near-term.

- Historically, May through September tends to be the weakest period for stocks. During election years, summer weakness often shifts to the fall.

- Strong market momentum and a resilient economy may keep stocks in positive territory, or at least until the fall when the election gains more focus.

Stocks have recently struggled with higher rates, but year-to-date, 2024 has gotten off to a decent start. While several parts of the market, notably small caps, have been left behind, as of mid-April the S&P 500 is up roughly 6%.

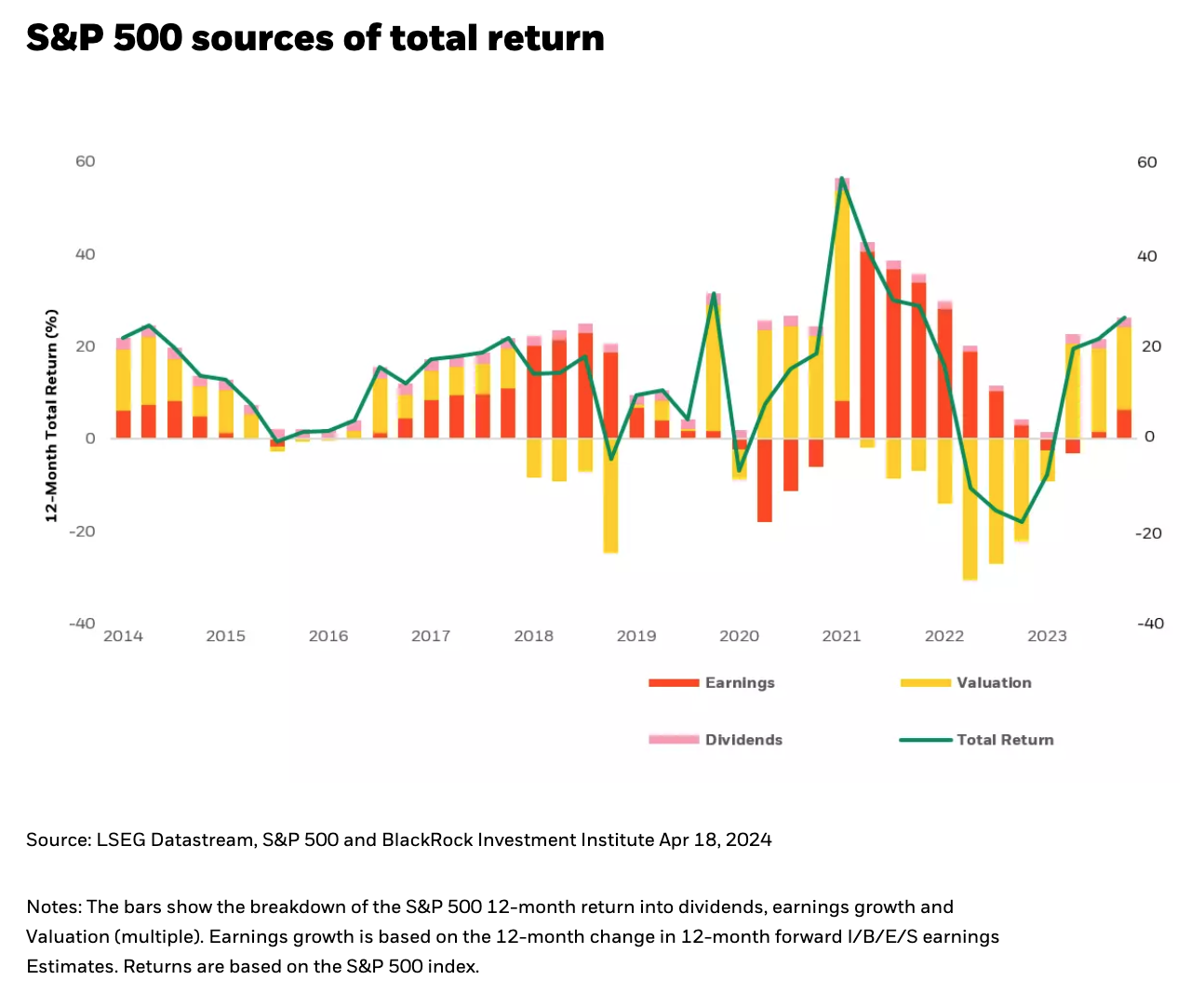

While stocks continue to rise, the driver of returns has shifted. Last year’s gains were powered by higher valuations. This year a solid economy is allowing for stronger earnings, which are increasingly driving returns for US stocks (see Chart 1).

That said, particularly in the near-term sentiment matters. Investors are understandably nervous given rising rates, a change in the Federal Reserve narrative and elevated geopolitical risk. While not rising to the same level of importance, investors may also be worried about the calendar.

As discussed in previous blogs, while the seasonal impact on stocks can be exaggerated, in the past returns have often followed seasonal patterns. Since 1960, the May through September period tends to be the weakest. Average monthly price returns during those months are approximately 0.10%, versus roughly 1% for all other months. In short, the old maxim, ‘Sell in May and Go Away’ has some validity.

Momentum and the election

While seasonal factors can matter, and certainly did in 2023, other forces can shift the impact and timing of seasonal trends. As we move into spring, two other factors are worth watching: momentum and the election. Starting with momentum, seasonal weakness tends to be more muted in month’s when the market has risen strongly in the preceding 12 months. Since 1960 average monthly returns are approximately twice as high in the spring and summer months when 12-month momentum is 10% or more. As of mid-April, S&P 500 12-month returns were still north of 20%, suggesting good momentum going into the late spring and summer.

The other potential mitigating factor may be the election cycle, which has its own internal logic. With the caveat that results should be treated cautiously given fewer observations, in past election cycles summer weakness often shifts to the fall. Said otherwise, historical election year’s have witnessed solid returns in June, July, and August before returns turned negative in September and October.

Intuitively, this makes some sense. While political junkies may be fixated on every primary machination, most people, including most investors, pay far less attention until the party conventions begin and the fall campaign starts. It is at this point polls become more significant, and investors start to pay more attention to the implications of the potential outcomes.

Near-term investment implications

If historical patterns hold near-term, seasonal market weakness may not necessarily be a prelude to a bigger summer correction. Instead, market momentum and a strong economy may keep stocks in positive territory, or at least until the full significance of the election starts to become apparent in the fall.