How Much, How Far, How Fast, Not When?

by John Canally, Chief Economic Strategist, LPL Financial

KEY TAKEAWAYS

· Although there is a chance the Fed will raise rates this week, our view remains that the Fed will hike later this year, most likely at the December 2015 meeting.

· While much of the focus has been on “when,” market participants may start asking “how much” and “how fast” rates may increase once the Fed begins to raise the rates.

· The current disconnect on the “how much” and “how fast” between the FOMC and the financial markets could be a major issue for financial market participants in the months ahead.

The policymaking arm of the Federal Reserve (Fed), the Federal Open Market Committee (FOMC), will hold its sixth of eight meetings of the year this week. On Thursday, September 17, 2015, at the conclusion of the two-day meeting, the FOMC will release a statement and a new economic and interest rate forecast. In addition, Fed Chair Janet Yellen will conduct her third post-FOMC meeting press conference of the year. The FOMC will also provide markets with a new set of targets at this meeting, as it does four times a year. The FOMC will release its new forecast for gross domestic product (GDP), the unemployment rate, inflation, the appropriate timing of the first rate hike, and the so-called “dot plot,” where each member identifies the appropriate level for the fed funds rate at year-end in 2015, 2016, 2017, and in the “longer run.” These data points will be scoured by market participants looking for clues regarding how the FOMC’s internal economic forecast has evolved since the last release in June 2015, for clues to future policy, regardless of any decision made this week. The dot plot, in particular the level of the fed funds rate the FOMC sees in the “longer run,” may play an important role in this week’s meeting if the committee does not raise rates.

GENERAL DISAGREEMENT

As of Friday, September 11, 2015, most market participants expect the Fed to make no changes to policy this week, although the market — per the fed funds futures contracts — is pricing in about a 1 in 4 chance of a hike this week. However, about half of the 100 or so economists surveyed by Bloomberg News expect the Fed to raise rates this week, but also point out that the yield on the 2-year Treasury note (often a good leading indicator of Fed action) has hovered near 70 basis points (0.70%) since mid-June 2015, an indication that the bond market doesn’t expect a move this week. Fed officials have largely been noncommittal on the issue, with the usual FOMC “hawks” (those who usually lean toward the low inflation side of the Fed’s dual mandate) eager to raise rates, while the “doves” (those who usually favor the full employment side of the dual mandate) have been saying more time is needed.

Our view remains that the Fed will hike later this year, most likely at the December 2015 meeting. However, the data — especially the inflation data — do not yet support a Fed hike. Why? Since the March 2015 FOMC meeting, the Fed has said:

“it will be appropriate to raise the target range for the federal funds rate when it has seen some further improvement in the labor market and is reasonably confident that inflation will move back to its 2 percent objective over the medium term.”

While the labor market data do support a hike, inflation has been moving in the wrong direction — lower — in recent months, thanks to another 30% drop in oil prices. In addition, Fed officials have made it clear that they want to be sure the market is fully aware of a rate hike when it comes. With financial markets and Fed watchers conflicted about the outcome of this week’s meeting (see above), the timing doesn’t seem right, either. Had the data — especially the inflation data — supported a rate hike this week, the Fed likely would not have let the recent turmoil in global financial markets around the Chinese equity markets and economy stand in the way.

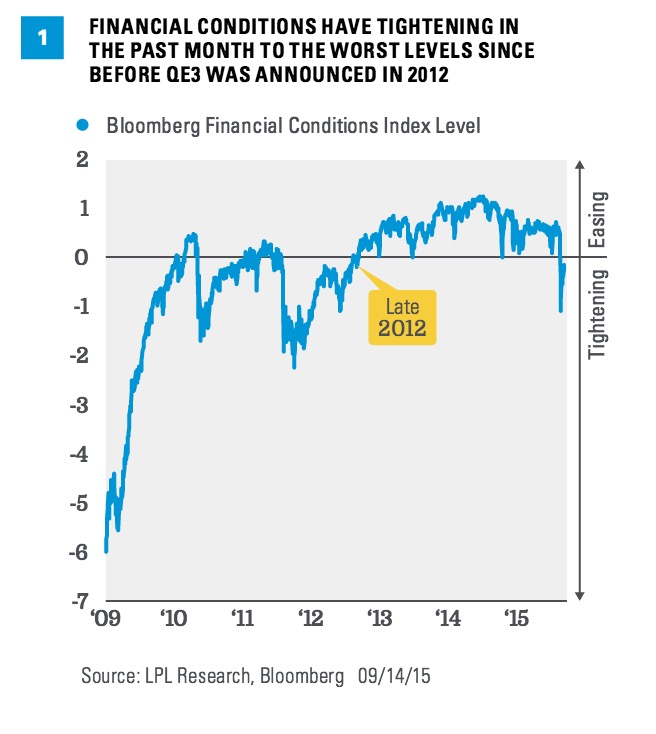

Also arguing against a hike this week are financial conditions, as measured by the Bloomberg Financial Conditions Index [Figure 1], which have tightened considerably in the past month. Even after recovering in the past two weeks, financial conditions remain at their worst levels since before the Fed announced quantitative easing 3 (QE3) in September 2012. In effect, the market has tightened on behalf of the Fed in the past four weeks.

IT’S HOW MUCH, HOW FAR, AND HOW FAST, NOT WHEN, THAT MATTERS

While many continue to obsess over the when the Fed’s first rate hike will occur, our long-held view is that “how much,” “how far,” and “how fast” the Fed hikes rates after it starts raising rates will be far more important than “when.” Right now, the Fed and the market disagree on nearly everything: when, how much, how far, and how fast, and ironically, the “when” is where there is the most agreement between the Fed and financial markets. As noted above, the market and the Fed are fairly closely aligned on the “when,” at most differing by a few months or so. The latest forecast (June 2015) by the FOMC of the timing of its first rate hike says that 15 of the 17 members of the FOMC expect the first hike to occur in 2015, and this timing is largely in line with what economists and financial markets are saying.

But there is still a large discrepancy on the “how much,” “how far,” and “how fast,” and the financial market and, in our view, the U.S. and global economy’s reaction to the Fed is much more dependent on the “how much,” “how far” and “how fast” than on “the when.” On the “how much” and “how far,” the Fed’s latest “dot plots” (a new set of dot plots will be released this week) put the endpoint of the Fed funds rate at 3.75%. The fed funds futures contract for mid-2018 puts the Fed funds rate at just 1.75%. This gap has widened since the last time the dot plots were released in June 2015. There is also disagreement on the “how fast.” The Fed’s dot plots published in June 2015 put the Fed funds rate at 1.625% by the end of 2016, implying that the Fed would raise rates by 150 basis points (1.5%) over the course of late 2015 and early 2016. The Fed funds futures market puts the Fed funds at just 0.80% by the end of 2016, suggesting less than 75 basis points (0.75%) of hikes over the next 15 months.

How — pun intended — the gap between the market’s view of the Fed and the Fed’s view of its own policy closes remains crucial to market (and economic) behavior over the next several years. If, as has been the case over the first five FOMC meetings of the year, the Fed lowers its view of the economy, inflation, the dot plots, etc. and pushes out the timing of the first Fed hike, risk assets (equities, high-yield bonds, etc.) may benefit. The opposite is likely to occur if the market — perhaps driven by a sudden, unanticipated uptick in inflation, wages, economic activity, or oil prices — has to move up its view of “how much,” “how far,” and “how fast” in a short period. The data received to date, along with the international backdrop and the recent tightening of financial conditions, continue to suggest the Fed will come back to the market at this week’s meeting, although it remains committed to achieving “the when” by the end of this year.

CLARITY NEEDED

Markets have been focused on when the first rate hike will be, and because the Fed has not started a rate hike cycle in 11 years, the “when” is certainly important. The current disconnect on the “how much” and “how fast” between the FOMC and the financial markets — and how it ultimately gets resolved — could be a major issue for financial market participants in the months ahead. We’ll be watching it closely.

Copyright © LPL Financial