Last week’s market performance proved that investors are having a hard time kicking a certain habit: treating “bad news as good.” Russ explains, suggesting that investors continue to focus on relative value.

While stocks retreated on Friday, following a confrontation on the Ukrainian border, equities pushed ahead last week. Part of the advance can be attributed to a perception, at least until Friday, that geopolitical risks in the Ukraine and Middle East were abating.

However, as I write in my new weekly commentary, “Where There is Value, There Are Investors,” last week’s market performance also proved that investors are having a hard time kicking a certain habit: treating bad news as good.

As the Federal Reserve (Fed) rolled out its easy money policy in the years following the 2008 financial crisis, investors became accustomed to treating weaker-than-expected economic news as a positive sign that the Fed would soon step in with more monetary stimulus.

But while the Fed plans to wind down its quantitative easing program by this October and most market watchers expect a Fed rate increase sometime during the first half of 2015, many investors still appear to be holding out hope for an even longer period of monetary accommodation, and such hopes largely drove last week’s advance.

Investors bid up stocks on the back of generally weak economic data, including another soft U.S. retail sales number, stagnating growth in the eurozone and slowing loan growth in China. For example, U.S. stocks rose sharply on Wednesday as investors interpreted weak U.S. retail sales as reducing the odds of an early Fed hike.

The common theme in all of these instances was optimism for either more aggressive monetary and/or fiscal stimulus, or, at the very least, a continuation of already easy monetary policy.

In my opinion, however, a change in the Fed’s intended monetary policy is unlikely, at least based on recent economic reports. While the U.S. economy does have persistent pockets of softness (such as household spending) and does face significant headwinds (like slow wage growth), it is generally improving. Though the U.S. economic recovery is certainly uneven, when you look at recent economic data overall, it’s evident that the recovery is gaining steam and that the U.S. economy has fully recovered from the first quarter’s economic contraction.

Looking forward, I see the U.S. economy growing at around 2% this year, consistent with the post-crisis average since the United States came out of the recession in the third quarter of 2009, but with a decidedly stronger second half. For the Fed to step in with a longer-than-expected continuation, or even an increase, in monetary stimulus, we’d need to see a clear trend of weaker-than-expected data rather than the mixed, but still generally positive, economic reports dominating headlines today.

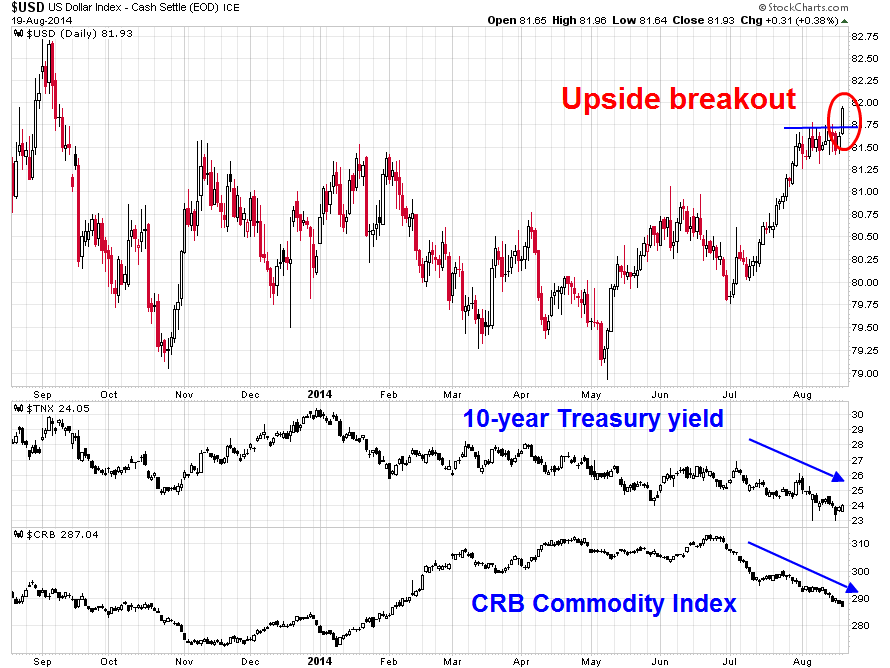

Plus, rates have been grinding lower lately without any help from the Fed, thanks partly to softness in other countries. Persistent economic weakness and the lingering threat of deflation have pushed down European bond yields. German Bund yields traded below 1% last week, an all-time low. To the extent that lower European yields make the United States more attractive by comparison, Europe’s slowdown is contributing to the persistence of low rates in the United States. In turn, low rates are helping to support stocks, as investors have little choice but to search for return, and even income, in other asset classes.

So, rather than continue to hope for an unlikely sea change in Fed policy, investors would do better to focus on relative valuation, which has become a key differentiator of performance lately. Despite lingering economic headwinds, market segments with relatively cheap valuations have been attracting buyers, a trend I expect to continue.

Sources: Bloomberg, BlackRock Research

Russ Koesterich, CFA, is the Chief Investment Strategist for BlackRock and iShares Chief Global Investment Strategist. He is a regular contributor to The Blog and you can find more of his posts here.

©2014 BlackRock, Inc. All rights reserved. BLACKROCK is a registered trademark of BlackRock, Inc. All other marks are the property of their respective owners.