by ConvergEx's Nicholas Colas

“Sell me this pen.” That is one of the oldest interview questions in the book. I have heard that it goes back to the old International Business Machines hiring process, when that organization was light years ahead in terms of hiring the best and brightest. There are many wrong answers to the question and only one right one, even if it comes in many permutations. Here are some examples:

The “Wolf of Wall Street” smart-alecky answer. Take the pen from the interviewer and quickly say “Write your name”. Your counterpart will start to look around for another pen. You then propose that you have one, and they obviously need it. Cute, but probably not the answer your prospective employer is looking to hear from a potential hire.

The “Rookie” answer. Most untrained salespeople will look at the pen and launch off into a description of its merits. “Let me tell you about this pen, ma’am. It has a lovely feel on the paper, never smears, and my firm guarantees that performance for life!” This may seem like standard used car salesman fare, mostly because it is. Bad answer.

The “Right” answer. You start by asking questions about what the interviewer does with his or her day. If they are a CEO, do they have occasion to sign important documents in the presence of others? You go for the high end pen sale, with a second one to give the other party as a toke of the CEO’s esteem. If they are an accountant, focus on keeping costs low with a bulk order. But in all cases, the right answer involves gathering facts first and selling second.

Just as there are “Right” and “Wrong” ways to sell products and services, the business discipline of marketing has its own rules of the road. Some of the most durable tenets of the profession come from the pen (no sale needed) of E. Jerome McCarthy, a marketing professor at Michigan State after World War II. In 1960 he codified the “Four Ps” of marketing – essentially the critical features behind marketing any product or service. In case it has been a few years since you studied them, here they are:

Product. The item or service that a company wants to sell.

Price. The amount the consumer is willing to pay.

Promotion. How the consumer hears about the product or service.

Place (Distribution). Where the buyers goes to purchase the item.

Now, instead of applying these categories to “Mad Men” style marketing of cars or detergent, think of them as the checklist for a point of view on securities prices. The Internet and social media have made ideas into consumer goods, after all. For any product – tangible or not – to succeed it must adhere to a solid strategy and address the “Four P’s” directly and forcefully.

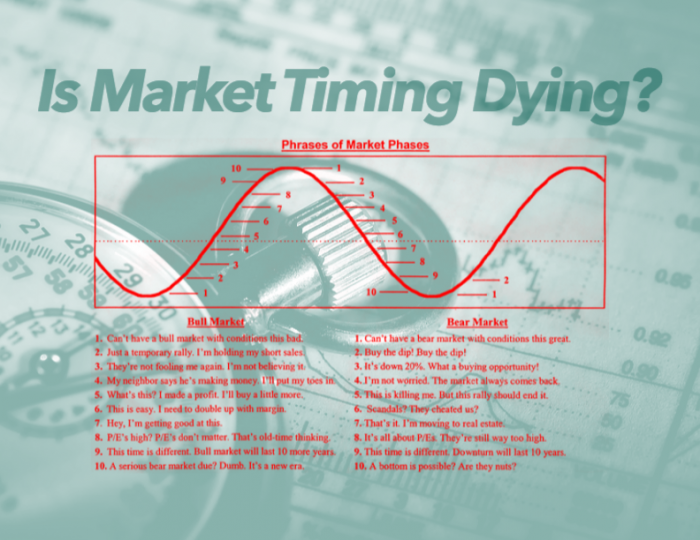

For the last five years, the negative case on risk assets – developed and emerging market equities, corporate debt, even notionally riskless sovereign paper (think Greek or Spanish debt) – has been losing market share to its more sanguine counterpart. Even investors with a positive view of the global economy will freely admit that things are still pretty weak, whether the metric is economic output or labor market growth. So why are equities higher, with the S&P 500 hitting a new record just yesterday? It’s not because things are great. It is because the “Positive story” about risk is trumping the “Negative story”, exactly as Ford might best Chevy or Frosted Flakes win over Shredded Wheat.

Let’s review the two products – positive and negative takes on risk assets – through the lens of the “Four P’s” of marketing.

Product: At first blush, we’re looking at a red car and a green car. Positive and negative investment cases are really the same product, albeit with different attributes. Stocks go up, or stocks go down. Bonds rise in price, or decline. Granted, there are a lot of reasons used to support these views in the world of investment analysis – political, economic, social, etc. But in the end it all comes down to a single call. Buy ‘em or sell ‘em. The menu in the cafeteria of modern finance is still quite short: chicken or beef.

Price: Thanks to the Internet, a lot of investment opinion is now essentially free. “And worth every penny”, you might add. Fair enough, but that obscures a larger truth. The price of investment viewpoints is the opportunity cost of doing something stupid or clever. Making money, or losing it. Follow the right counsel, and you profit. Be led astray, and you lose. The price on the dust jacket of the idea is the least of your worries.

Promotion: Again, thanks to business television and radio, the Internet, old school media, and Web 2.0 social networking, anyone interested in learning more about the capital markets knows where to go. Seeking Alpha for the mainstream, Zerohedge for the edgy stuff that the cool kids like, and hundreds of sites in between. Buy side and sell side businesses have their own pundits and experts, blogs and press pages. No shortage of promotion in this market, including (of course) this note.

Place: Pretty much like promotion, but since research opinions are so widespread and largely without explicit price, you can find them anywhere. It’s sort of like the old Anglican hymn: “You can meet them in school, on the street, in the store, in church, by the sea, in the house next door”. Only that refers to saints, not investment views.

In the end, there isn’t actually much of a difference between the bull and bear case on risk assets – three of the four Ps line up pretty exactly. The one exception is price, as expressed by opportunity cost. Go short a market that rises 10%, and you have lost 20% - half from your ill-considered negative bet, and half from not buying the asset in the first place. And this is where the positive case for risk has it all over the negative arguments in the Four P’s comparison. Nothing succeeds like success, and the market share winner of this two product race is the full-throated roar of the optimist.

That doesn’t mean that this will always be the case – far from it. The positive case for risk hasn’t won the day because of a slew of upside surprises for economic data, corporate earnings, or even benign headlines on geopolitics or energy prices. Corporate earnings are great, no doubt, but reinvestment rates are low as companies buy back stock rather than accelerate the expansions of their businesses. Labor markets are still punk throughout the developed world, oil prices are the straw that sits on the proverbial camel’s back, and no one can argue that the world is a more peaceful place than a decade ago.

There hasn’t been a pullback in U.S. stocks of more than 10% in 30-odd months, and in that fact sits an important reason why the rally has continued. I am not sure that the +5 year bull market for stocks could actually withstand a 10% correction, especially a quick flush lower. Remember – the only real differentiator between the bullish and bearish “Product” is cost. Specifically, opportunity cost. Once the negative case begins to pay off, it could begin to gain the advantage with market participants and cause a deeper selloff. Which will make it even more popular.

Either way, you’ll probably need a pen to write your thoughts. Can I interest you in this one?