Submitted by Lance Roberts of STA Wealth Management,

I have written about in the past the detachment between underlying fundamentals and the artificially elevated markets. (See here, here and here) However, as I specifically stated in the article entitled "The Fed Taper And Market Direction:"

"As a money manager I am currently invested in the markets because the markets are rising and I must participate or suffer career risk. However, it would be completely naive to dismiss the risks that are currently present and rising. Market and economic cycles do not, and cannot, last forever. While it is never expected, as 'this time is always different,' it is the eventual 'reversion to the mean' that leaves investors devastated as the reality of the underlying fundamentals collides with fantasy."

However, it is critically important to understand that market reversions do not occur without a catalyst. Whether it is the onset of an economic recession, a natural disaster or a financial crisis - there is always something that sparks the initial selloff that leads to a full blown market panic. With this idea in mind here are 3 rising risks that investors should be paying attention to.

1) Government Shutdown/Debt Ceiling Debate

The markets were well aware that a Government shutdown was likely to occur. However, the markets believed that it would be a short term event. Unfortunately, that may not be the case. As reported by Bloomberg:

"The President made clear to the Leaders that he is not going to negotiate over the need for Congress to act to reopen the government.

House Republican leaders plan to bring up a measure to raise the U.S. debt-limit as soon as next week as part of a new attempt to force President Barack Obama to negotiate on the budget, according to three people with knowledge of the strategy.

The approach would merge the disputes over ending the government shutdown and raising the debt ceiling into one fiscal fight.

"I'd like to get one agreement and be done," House Majority Whip Kevin McCarthy told reporters today without offering details.

Republican leaders are attempting to pair their party's priorities with a debt-limit increase, a plan they shelved last month to focus on a stopgap measure to fund the government in the new fiscal year. The goal is to have a bill ready in coming days, even without resolving the partial government shutdown, according to a Republican lawmaker and two leadership aides who asked not to be identified to discuss the strategy."

The risk that this poses for the markets are twofold. First, with the economy already growing very weakly the government shutdown acts as a fiscal drag on the economy. The longer the government shutdown lasts the more negative impact there will be to economic growth. Secondly, the markets were prepared, and expected, a short term event with the Republicans quickly "rolling over" and resolving the fiscal crisis. However, the prolonged debate could roil the markets in coming weeks.

2) Revenue Growth Is Non-Existent

As I discussed recently, earnings, as well as valuations, are becoming extremely stretched. Specifically, I wrote that:

"The ongoing deterioration in earnings is something worth watching closely. The recent improvement in the economic reports is likely more ephemeral due to a very sluggish start of the year that has led to a 'restocking" cycle'. The sustainability of the uptick is crucially important if the economy is indeed truly turning a corner toward stronger economic growth. However, with interest rates rising, oil prices surging and the Affordable Care Act about to levy higher taxes on individuals, it is likely that a continuation of a "struggle" through economy is the most likely outcome. This puts overly optimistic earnings estimates in jeopardy of be lowered further in the coming months ahead as stock buybacks slow and corporate cost cutting continues to become less effective."

The 2-Panel chart below shows the S&P 500 versus topline revenue per share.

As you can see in the top chart revenue per share has flatlined in recent quarters even as prices rise due to the artificial interventions from the Federal Reserve. The second chart is the most important of the two. Historically, when the annual change in revenue per share declines the market is generally correcting with it. Currently, the price of the markets have detached from the underlying revenue growth. This is unlikely to be sustained for an extended period of time.

3) "Herding" Into Popular Assets

One of the phenomenon’s that has occurred over the last several years is the proliferation of hedge funds, high frequency trading firms and program trading. The problem with this explosion is that they are more and more dollars chasing a finite set of assets. This "asset chase" leads to price dislocations and increased risk. As reported by Bloomberg (via Zero Hedge)

"Money managers could pose threats to the U.S. financial system when reaching for higher returns, herding into popular asset classes... and can contribute to asset price increases and magnify volatility during sudden shocks, a report by the Treasury said today.

A certain combination of fund- and firm-level activities within a large, complex firm, or engagement by a significant number of asset managers in riskier activities, could pose, amplify or transmit a threat to the financial system," the Treasury's Office of Financial Research said in the report.

Exchange-traded funds 'may transmit or amplify financial shocks originating elsewhere' by pooling assets into illiquid investments.

Herding into more illiquid investments may have a greater potential to create adverse market impacts if financial shocks trigger a reversal of the herding behavior."

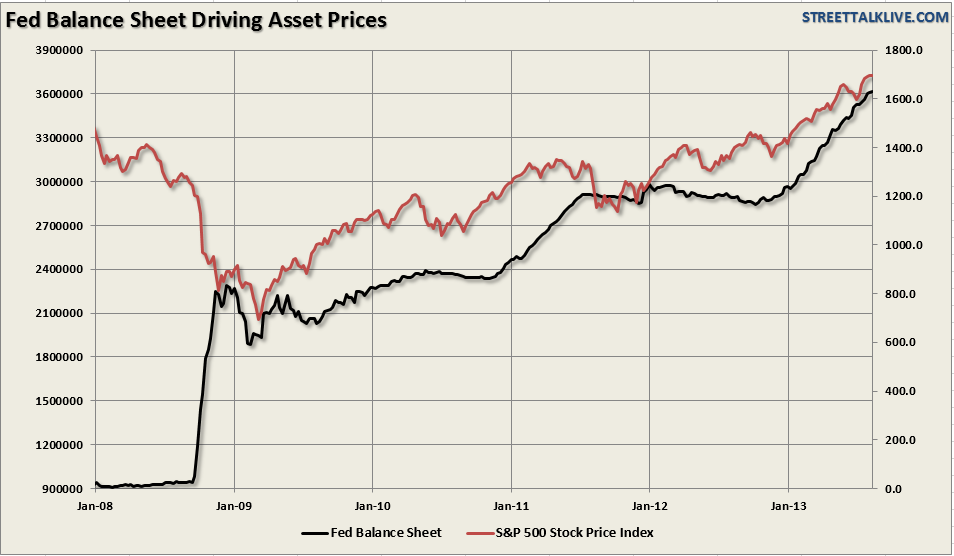

Of course, as we have shown many times in the past much of the rise in the market can be attributed to the Federal Reserve's monetary interventions. The risk is going to be what happens when they actually begin to reduce that support?

Complacency Not An Option

While the recent Federal Reserve inaction is bullish for stocks in the short term there are plenty of reasons to remain somewhat cautious. Stocks are overvalued, rates are rising, earnings are deteriorating and despite signs of short term economic improvements the data trends remain within negative downtrends. Investors, however, have disregarded fundamentals as irrelevant as long as the Federal Reserve remains committed to its accommodative policies. The problem is that no one really knows how this will turn out and the current assumptions are based upon past performance.

Of course, as anyone who has ever invested should already know, past performance is no guarantee of future results.