Challenging a Long-Held Assumption about Commodities

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

There’s no denying China’s massive economic growth over the past decade, as the country recorded an average GDP of more than 10 percent per year. In only seven years, China’s economy doubled; in 13 years, it tripled.

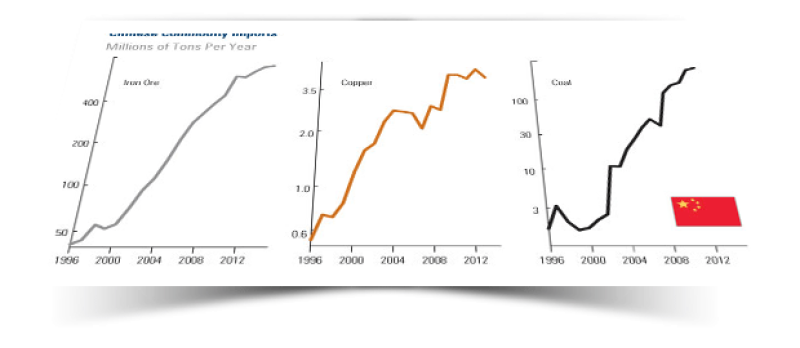

With this incredible expansion, China began to import commodities at an incredible pace. In 2000, the country imported only 70 million tons of iron ore; today, it’s more than 10 times that amount, at 763 million tons. Copper imports increased dramatically too, growing from 1.6 million tons in 2000 to more than 4 million tons per year today, according to BCA Research data.

And when it comes to oil demand, 17 years ago, China was a net exporter. Today, it is the second-largest importer, transporting 5.4 million barrels of oil into the country every day.

That’s why it is widely accepted that the Asian giant spurred higher commodity prices in the past decade.

And if the country was the force behind the boom, then the assumption is that China’s lower, but still healthy growth will be a drag on commodity prices.

But recent research challenges this assumption.

According to BCA Research’s Chen Zhao, what is initially an “outrageous proposition” may not actually be. The analyst says the fact that China’s consumption of industrial commodities significantly increased at the same time prices rose may have only created “the impression that China was the main driving force behind the commodities boom. "

Consider that since the substantial growth early in the last decade, China has continued to import commodities at a remarkable pace. Since 2007, the Asian giant buys 2 times more iron ore, 1.5 times more copper and 6 times more coal from other countries.

“The level of Chinese commodity imports obviously reflects the size of its economy,” says BCA. So even if the growth rate has slowed down, “the absolute level of Chinese commodity demand continues to set new records every year.”

Then what’s really driving commodity prices?

If you can’t entirely blame weak commodity prices on Chinese demand, what is the culprit? Take a look at the chart below. The red line plots the 10-year rolling correlation of annual returns on the Thomson Reuters/Jefferies CRB Commodity Index (CRB) with China’s real GDP growth. The correlation between these two numbers has stayed close to 0.4 since the late 1990s.

Now take a look at the blue line, which shows a negative correlation between the CRB and the trade-weighted U.S. Dollar. The correlation since 2010 has hovered around -0.8, implying that “the dollar has much more explanatory power,” says BCA.

The data confirms BCA’s “long-term suspicion that the bull market in commodities last decade was mainly a reflection of a sustained fall in the U.S. dollar.”

This isn’t the only time we’ve experienced this phenomenon. In the 1990s, when the U.S. economy was booming and the dollar was strong, commodity prices were weak and oil prices fell to an all-time low of $10 per barrel.

Today, many emerging market economies that had no global footprint a few decades ago are now growing at a much faster pace than the developed countries. These emerging nations have young, growing populations who are moving to the cities, becoming wealthier, and consuming more goods and services.

However, like I shared last week, Credit Suisse is of the opinion that prices of commodities may no longer rise and fall together in unison, emphasizing that investors will need to focus on individual commodities depending on the supply and demand factors. This is why we advocate that investors hold a diversified basket of commodities actively managed by professionals who understand these specialized assets and the global trends affecting them.