Authored by Charles Gave of Gavekal.com,

France is engulfed by a political, economic and moral paralysis. The president has record low popularity, unemployment is making new highs and the tax czar of a supposedly left wing government just quit after repeatedly lying about a pile of cash he had stashed in a Swiss bank account. From such a sorry state of affairs, you might think that things could only get only get better. Unfortunately, economic cycles do not work this way and it is my contention that France is about to enter what was known during the gold standard era as a “secondary depression.” The rigid design of the euro system means the whole eurozone is prone to the kind of brutal cyclical adjustments seen in that hard money era of the 19th and early 20th centuries. But having reached the logical limits of its decades long experiment in state-run welfare-capitalism France is far more exposed than even its struggling neighbors.

By way of refresher the typical economic cycle during the gold standard era ran something like this:

- The first phase of the cycle sees investors respond to strongly positive returns on capital by bidding up the value of assets and boosting leverage. Banks loosen their lending standards, genuine entrepreneurs and charlatans become indistinguishable and commentators declare that some new innovation means this time is “different”. The scarcest commodity during this period of plenty is memory of past cycles.

- The first signal that the cycle has turned is a market "panic". The trigger is the realization among market participants that the return on invested capital has fallen below the cost of capital. This shock adjustment phase usually lasts a few months at most, and is associated with collapsing asset markets together with a number of bankruptcies in the financial system.

- An end to the acute phase of the crisis is usually accompanied by a collapse in interest rates, causing market participants to conclude that normal business conditions have resumed. A massive relief rally usually ensues.

- What follows is the far more serious secondary depression which unfolds like a creeping hangover after an indulgent night on the town. This capitulation materializes as investors come to realize that the prevailing ROIC has remained below the cost of capital. Back in the gold standard era, such secondary depressions usually lasted three to five years and accounted for most investment losses.

It is increasingly clear that both Italy and Spain are caught in a debt trap and have now entered the debilitating phase of the adjustment cycle. Devaluation—their one viable escape option—is ruled out by the strictures of euro membership.

Last year, I argued that France was primed to follow the same ruinous trajectory as its immediate southern neighbors (see The Coming French Depression). The policies followed by the French government over the last nine months mean this outcome has become a near certainty. The latest awful French economic data has removed any doubt that I reserved.

The case for the French depression

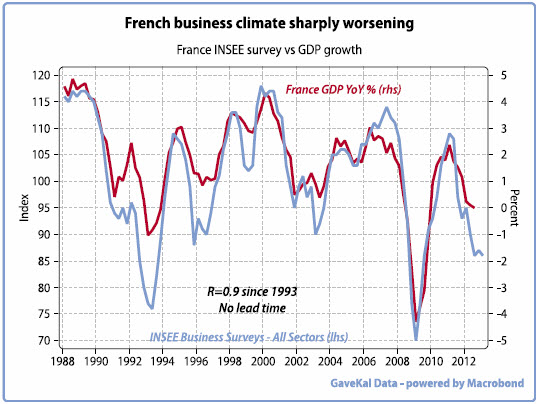

My analysis starts with an assessment of business conditions as illustrated by the INSEE survey. This survey is published monthly and has a long and reliable history. The lead time between the survey release and different economic variables varies from three to nine months.

A simple regression between the survey results and France’s GDP indicates that within six months the economy will be contracting at an annualized rate of about 1%.

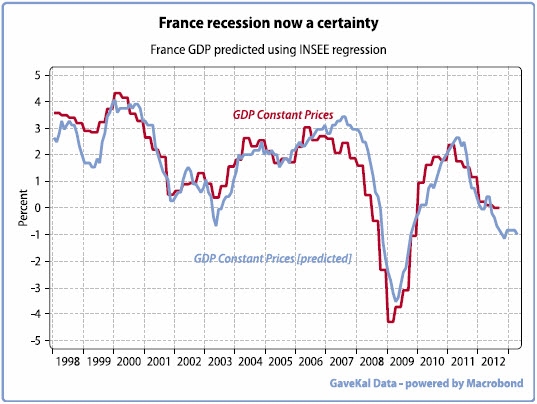

I have long used industrial production as the best available proxy for private sector activity and the latest readings are to say the least, ominous. France is extremely unusual in that government spending accounts for a full 57% of national output (only Denmark has a higher ratio). Since the public spending share of GDP is not likely to contract, the burden of adjustment will be borne by the private sector—a 3% cratering of this part of the economy is likely to eventuate.

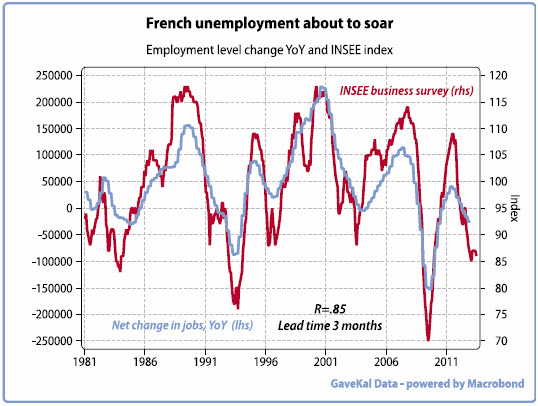

As a result of this collapse in private sector activity, employment levels are going to implode.

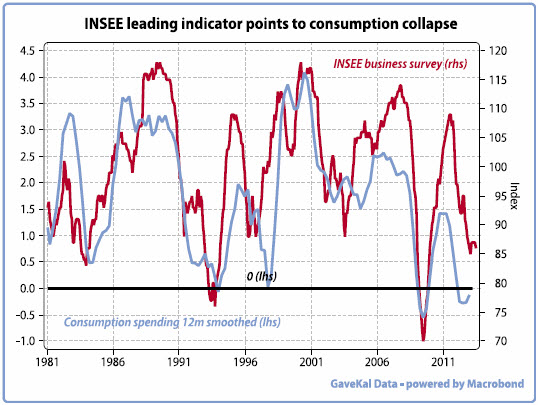

And with French employment collapsing, it is to be feared that French consumption follows suit. The vicious spiral of decline will ensure that France enters a secondary depression of the type outlined at the outset of this piece.

Wider economic consequences

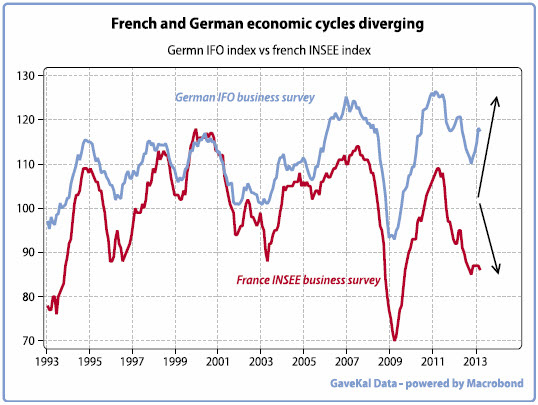

A divergence in the French and German business cycles is starting to open up for the first time in recent history which will lead to escalating risk within the eurozone system.

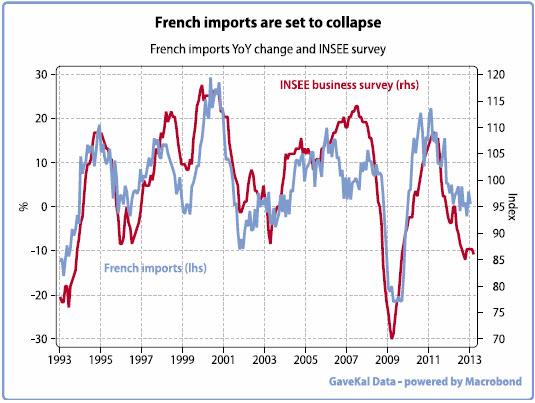

The severe squeeze on household income will ensure a collapse in French imports which can only have negative consequences for producers in Spain and Italy—for most eurozone countries France is their second largest export market.

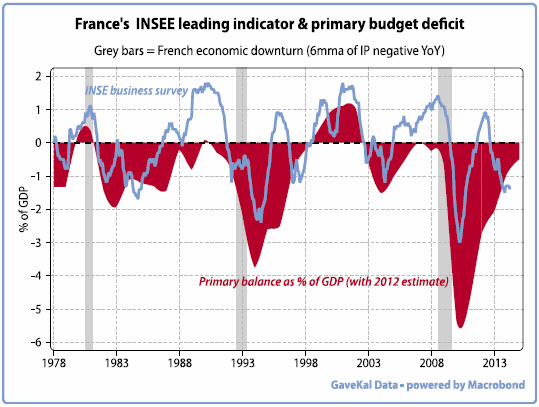

France’s budget deficit is going to explode. Higher unemployment will push up government spending, while reduced consumption causes a collapse in VAT receipts. And lower economic activity reduces all forms of tax income that a voracious government machine so depends upon.

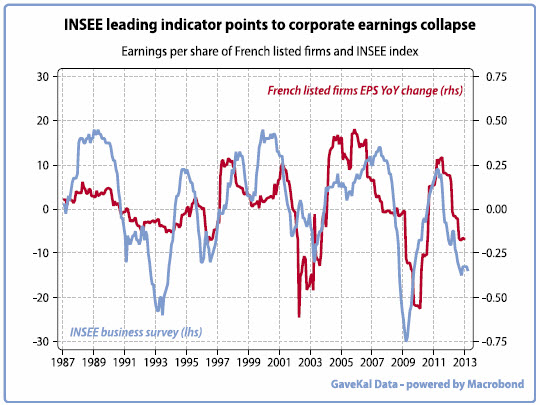

As a result, the primary budget deficit will deteriorate massively in 2013 - it is worth noting that this outcome has materialized each time that our business survey leading indicator has fallen so precipitously. French long rates will quickly come under pressure as was the case for Spain and Italy once their budgetary situation deteriorated—the French government is hugely complacent about its entitlement to low cost funding even though any spike in rates will quickly make the budget situation untenable. And as goes the economy, so goes the corporate sector. Profits for those companies exposed to both the domestic economy and the battered southern European markets are also likely to face a severe squeeze.

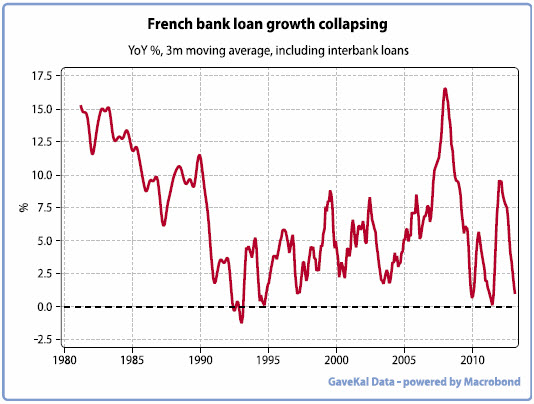

But what especially scares me about the French situation is that the economy is already suffering a huge credit crunch which can only get worse.

Conclusion

France has economic problems that are particular to its political culture. While speculative excesses in Spain and Ireland were concentrated in an over-built, over-geared real estate sector, French exuberance was a civil service affair. (Remember the adage: too many houses in Spain, too many factories in Germany, too many civil servants in France). This out-of-control public sector machine used easy funding conditions through the 2000s to bolster the ranks of an already bloated bureaucracy - the assumption was that such captive groups would vote for their ultimate pay -masters come election time. (This is what I called social clientelism). As a result France is the only country that we follow which has seen the public sector grow faster than the private sector in every year since 1987!

The interesting thing is that the government share of GDP in France has relentlessly risen regardless of whether a right or a left leaning party was in power. Such has been the complete capture of the French economy by the bureaucracy that the public spending trend has remained unbroken. In simple terms the fellows managing France’s economy have organized a system such that the public sector can continually pillage the private sector. This institutionalized method of stealth robbery has created a self-reinforcing cycle of economic decay such that lower corporate profits feed into reduced private investment, and so on to lower economic growth, resulting in rising unemployment levels.

At its core, France’s economic malaise is a failure of public morality. The public sector elites not only detest the private sector, but they also believe that it is a higher calling to steal money from entrepreneurs and give it to civil servants. Suffice to say this moral bankruptcy of the body politic means the situation is intractable—when the population is bombarded with propaganda that wealth creation is somehow dirty, while it is morally permissible for the state to expropriate all private gains, it will be hard to build an environment for economic growth.

The fact is that elites in France are convinced that communist technocracy is a superior system to capitalism, and this belief has been accepted by a large part of the population. So the solution for France is not incremental reforms to labor markets, but a complete overhaul which would bring to power sensible people with a different set of values. In the short term, radical change is mitigated by the fact that France last year voted for more pillaging and enhanced communist technocracy (the government is now in overdrive seeking to oblige them). Of course, the event that will cause the music to finally stop is when foreign investors stop lending. That moment will likely coincide with the last French entrepreneur exiting for London, New York or Shanghai—he or she should turn off the lights before bidding a sad farewell.

Until quite recently, my working assumption was that a full-blown French debt crisis would occur between 2014 and 2017. In light of the extraordinary malfeasance of the current government I have changed my mind and believe that France is now extremely near to that abyss. Fasten your seat belt in Europe—the world’s last truly Communist country is about to implode.