Why ETFs Aren’t a Good Fit in European High Yield - Context

by Fixed Income AllianceBernstein

August 01, 2017

The index-tracking trend is firmly entrenched. But do investors recognize the big differences between stock and bond ETFs? And do they appreciate that these can cause European high-yield ETFs to lag?

More investors are choosing to take their exposure to fixed income via passive approaches, especially exchange-traded funds (ETFs). Many seem to assume that what they’ve learned about equity ETFs will also apply to their bond counterparts—unaware that there are vital differences between the two, particularly in high yield. And costly differences can have a big impact on how effectively high-yield ETFs deliver.

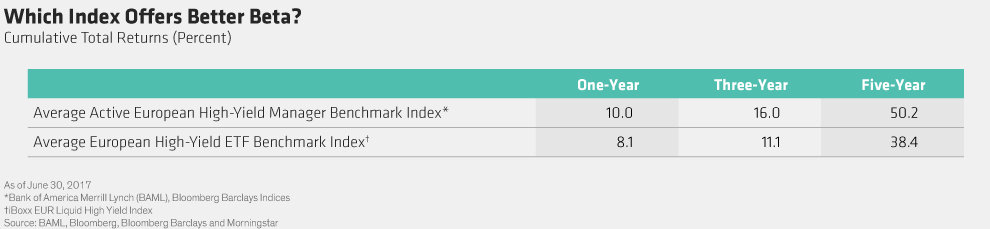

Europe’s actively managed high-yield funds measure their performance against a range of indices, most often various Bank of America Merrill Lynch and Bloomberg Barclays high-yield benchmarks. They set a high performance bar—significantly higher than the iBoxx Liquid High Yield Index which most European high-yield ETFs aim to track (Display).

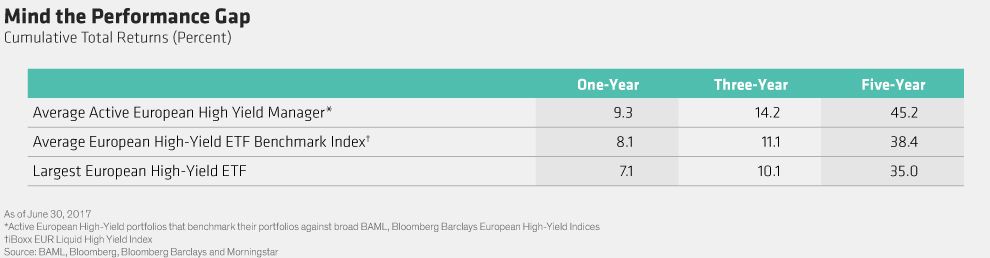

The iBoxx holds many more short-dated, low yielding bonds—which explains why its beta seems significantly worse. Europe’s biggest high-yield ETF has consistently lagged both the active manager indices and the iBoxx itself. Most importantly, the ETF has returned significantly less than Europe’s actively managed high-yield funds over one, three and five years, as shown in the Display below.

What are the reasons for this performance gap? We think the answers lie in failure to recognize that ETF structures and the inherent nature of the high-yield asset class just aren’t a good fit.

The Bigger Bond Opportunity Set

Investors in equity ETFs can hold, more or less, all the equities that make up a given index. But this just isn’t possible in high-yield bonds, which come in far more diverse forms. Borrowers have lots of flexibility to tailor their bonds to fit their specific needs. One company alone may issue bonds that may vary, for example, in their maturity dates, place in the company’s capital structure and legal rights.

This results in many different kinds of high-yield bonds, making Europe’s high-yield bond market highly fragmented. This, in turn, means most bonds don’t trade very often. Some are in very short supply. These liquidity constraints ensure that high-yield ETF managers can’t hold all the bonds in their index like their equity counterparts. Instead, they use sampling techniques and buy a selection of bonds they believe broadly reflect the index they’re trying to track.

This makes high-yield ETFs much less accurate approximations of the indices they’re tracking than market cap–driven equity ETFs, which can hold all the constituents of a given equity index in weightings in line with those market caps. High-yield bond ETFs, therefore, report much higher tracking errors than their equity cousins—something that can be further compounded by the fact that Europe’s high-yield market tends to have more outliers than the European stock market.

High Yield Is Trickier to Trade

Because bonds, unlike equities, have finite maturities, fixed-income indices turn over much more than their equity counterparts as securities mature and are replaced with new issuance. In 2016, for example, 23% of new issues entered the Bloomberg Barclays Euro High Yield Index, while 15% left it. By contrast, the annual turnover rate of the S&P 500 has averaged about 4%–6% in recent years.

High-yield ETF managers are, therefore, obliged to do a lot of buying and selling to stay broadly in line with the bonds included in their designated index. This is expensive—most bond indices must rebalance monthly, whereas equity indices rebalance quarterly at most.

These trading costs can eat considerably into investment returns. Transaction costs in bonds are far higher than in equities. According to Barclays, during the eurozone crisis, the average cost of buying and selling a bond was nearly 2% of the bond price.

In today’s more benign environment, it costs around 0.7% of a bond’s price to buy and sell it. Active high-yield fund managers make great efforts to minimize unnecessary trading that won’t prove performance-enhancing—and to anticipate pockets of liquidity that will help them transact efficiently and keep costs to a minimum.

The costs issue is further exacerbated by the fact that the prices of individual high-yield bonds are often highly opaque. Equities are nearly always traded on exchanges, where their prices are easily available for all to see. But high-yield bonds nearly always trade over the counter, with buyers and sellers privately negotiating deals whose terms are available only patchily and some time after these deals are agreed.

High-yield ETF managers don’t generally buy or sell bonds on value grounds alone. Instead, they’re merely compelled to keep pace with index turnover.

ETFs are efficient tools for some investors in some asset classes in some markets. But in European high yield, their long-term performance suggests there are reasons to be highly skeptical.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. AllianceBernstein Limited is authorised and regulated by the Financial Conduct Authority in the United Kingdom.

Copyright © AllianceBernstein