by Lance Roberts, Clarity Financial

There has been much debate about the current low levels of interest rates in the economy today. The primary argument is that the “30-year bull market in bonds”, due to consistently falling interest rates, must be near its end.

Of course, this debate has devastated the “bond bears” who have consistently been frustrated by lower interest rates despite their annual predictions to the contrary. However, just because interest rates are currently low, does this necessarily mean that they must rise?

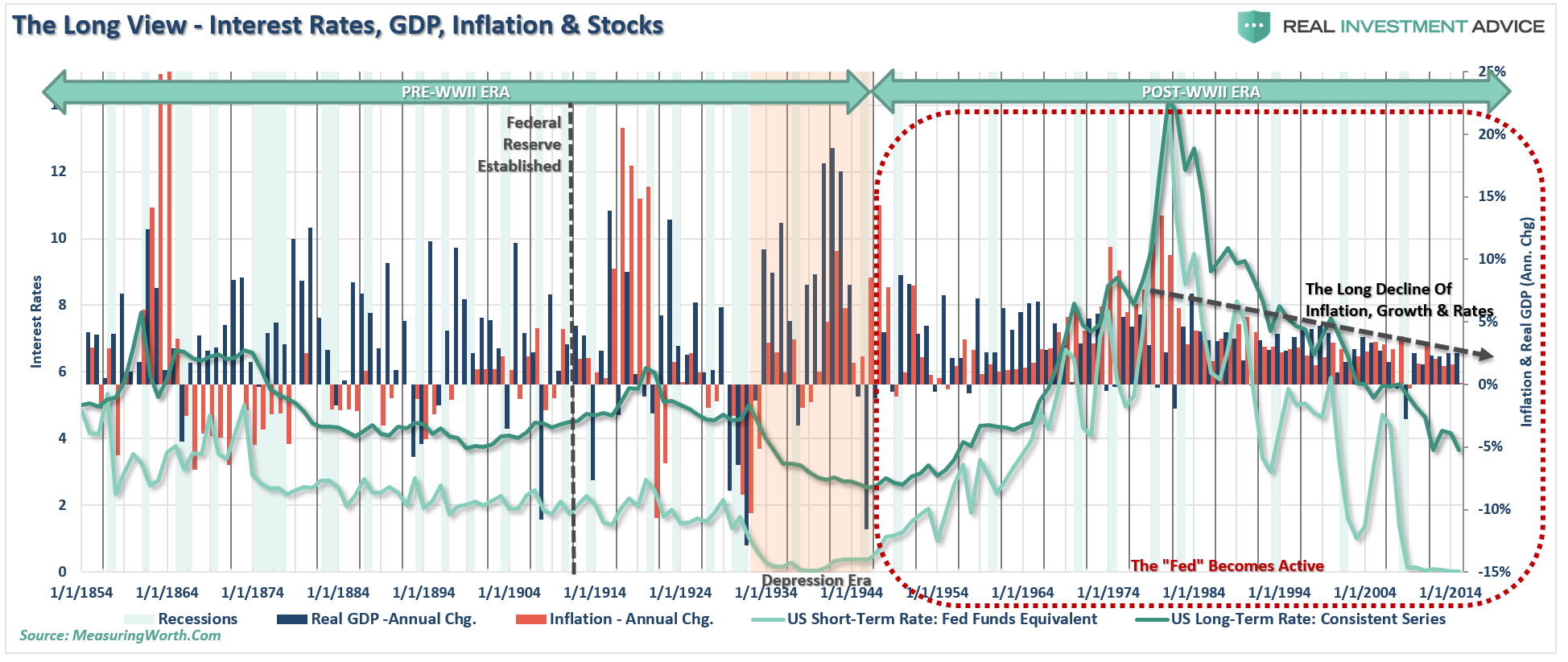

The chart below shows a VERY long view of interest rates (equivalent rates to the Federal Funds Rate and 10-year Treasury) back to 1854.

While there is much data contained in the chart above, there are a couple of important points to consider in this debate. The first is that interest rates are a function of the general trend of economic growth and inflation. Stronger rates of growth and inflation allow for higher borrowing costs to be charged within the economy. As shown, interest rates have risen during three previous periods in history; during the economic/inflationary spike in early 1860’s, again just prior to 1920 and during the prolonged manufacturing cycle in the 1950-60’s following the end of WWII. Secondly, interest rates tend to fall for very extended periods.

However, notice that while interest rates fell during the depression era economic growth and inflationary pressures remained robust. This was due to the very lopsided nature of the economy at that time; the wealthy prospered while the middle class suffered, which did not allow money to flow through the system (monetary velocity).

Currently, the economy is once again bifurcated. The upper 10% of the economy is doing well while the lower 90% remain affected by high levels of joblessness, stagnant wage growth and a low demand for credit. For only the second time in history, short-term rates are at zero and monetary velocity is non-existent.

The difference is that during the “Great Depression” economic growth and inflationary pressures were at some of the highest levels in history, while today the economy struggles along at a 2% growth rate with inflationary pressures that detract from consumptive spending.

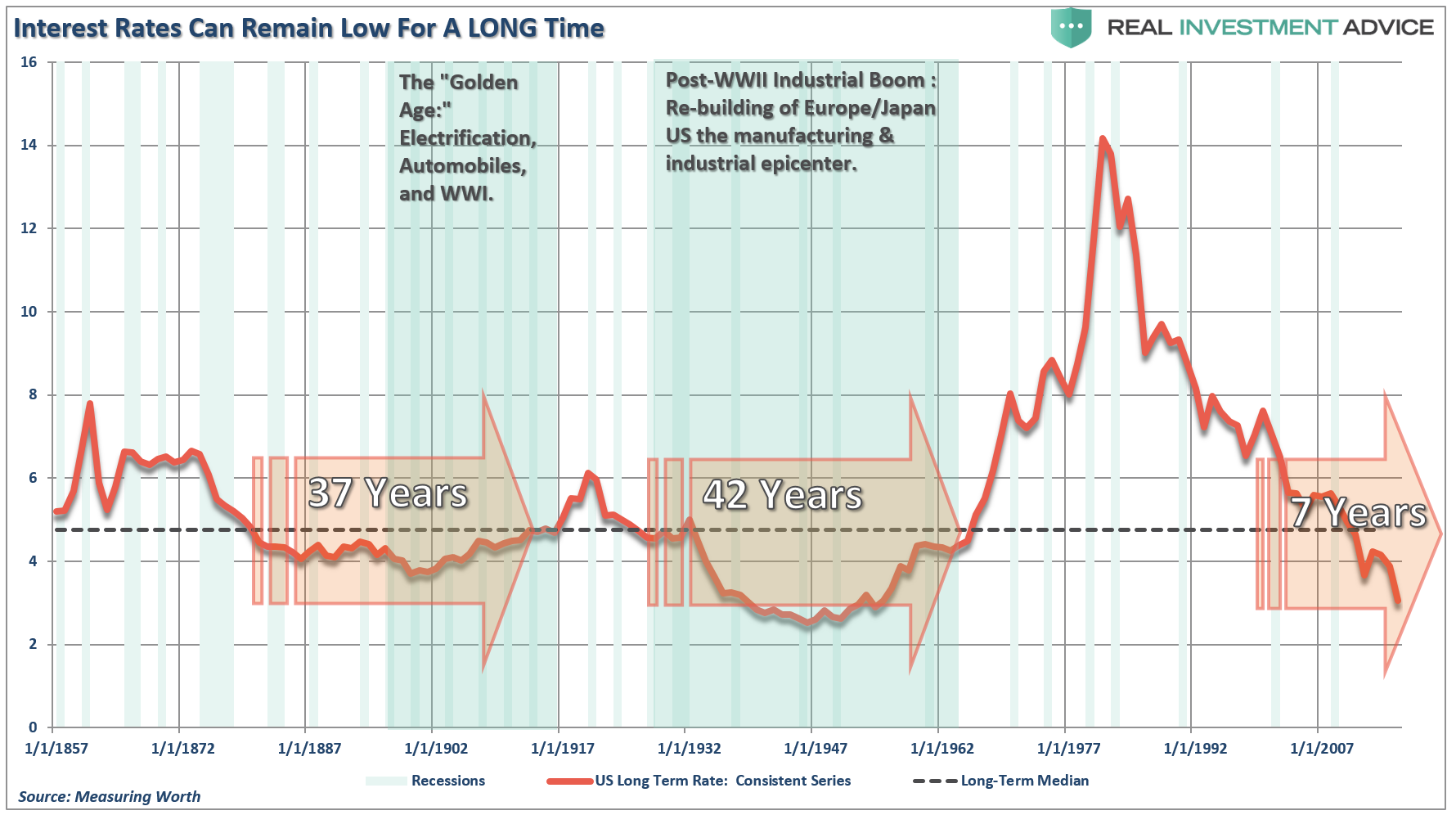

Let’s look at the fall of interest rates since the 1980’s in a slightly different manner.

As stated above, since interest rates are ultimately a reflection of economic growth, inflation, and monetary velocity, the fact that the globe is awash in deflation, caused by weak economic output and exceedingly low levels of monetary velocity, there is no pressure to push rates higher. In fact, interest rates in the U.S. continue to fall as money is fleeing other countries and associated risk for safety. Let’s take a look at the chart of 10-year equivalent treasury rates once again. The dashed black line is the median interest rate during the entire period.

(Note: Notice that a period of sustained low interest rates below the long-term median, as shown in the chart above, averaged roughly 40 years during both previous periods. We are only currently 4-years into the current secular period of sub-median interest rates.)

As shown, there have been two previous periods in history that have had the necessary ingredients to support rising interest rates. The first was during the turn of the previous century as the country became more accessible via railroads and automobiles, production ramped up for World War I and America began the shift from an agricultural to industrial economy.

The second period occurred post-World War II as America became the “last man standing” as France, England, Russia, Germany, Poland, Japan and others were left devastated. It was here that America found its strongest run of economic growth in history as the “boys of war” returned home to start rebuilding the countries that they had just destroyed. But that was just the start of it as innovations leaped forward as all eyes turned toward the moon.

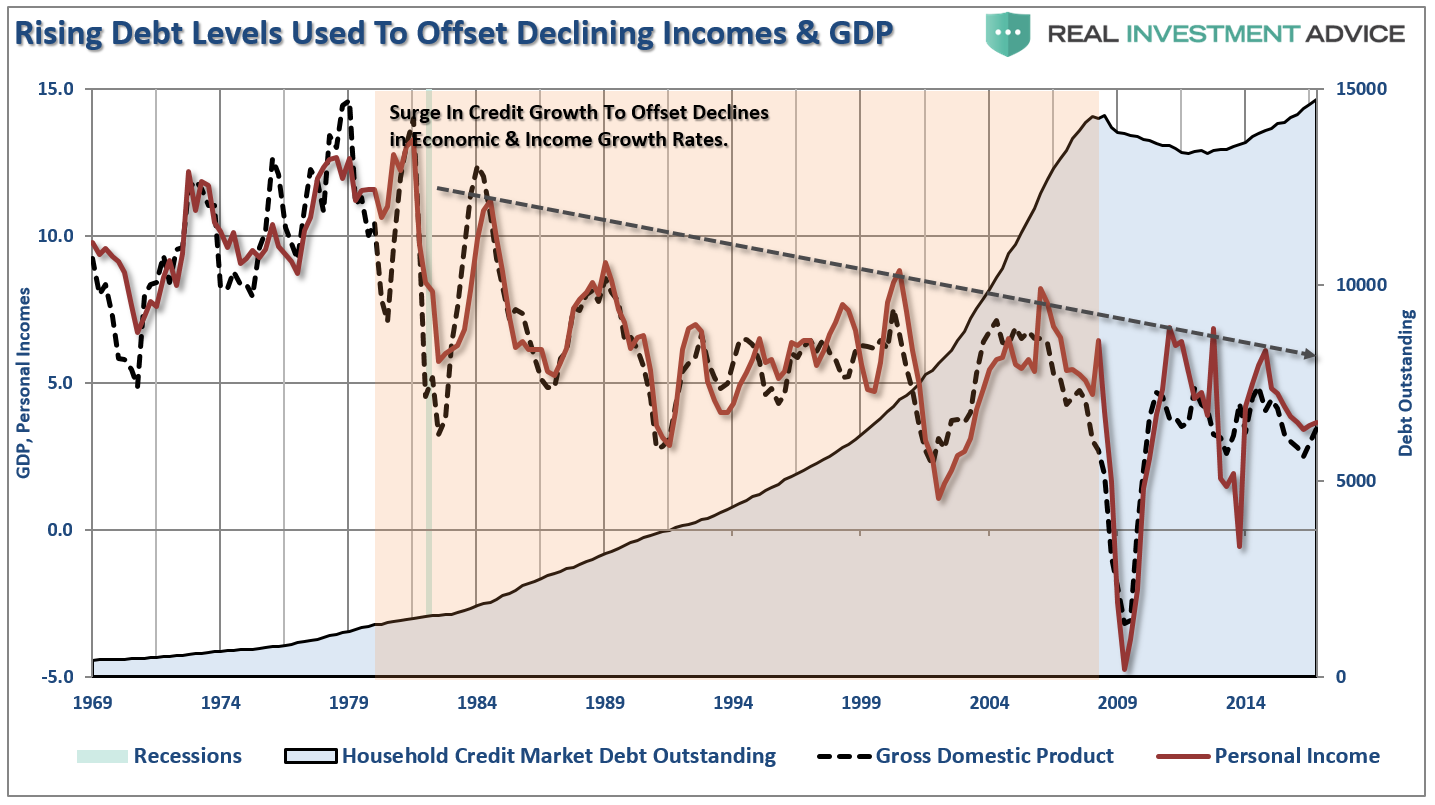

Today, the U.S. is no longer the manufacturing epicenter of the world. Labor and capital flows to the lowest cost providers so that inflation is effectively exported from the U.S. and deflation can be imported. Technology and productivity gains ultimately suppress labor and wage growth rates over time. The chart below shows this dynamic change which begin in 1980. A surge in consumer debt was the offset between lower rates of economic growth and incomes in order to maintain the “American lifestyle.”

The Economic Challenge

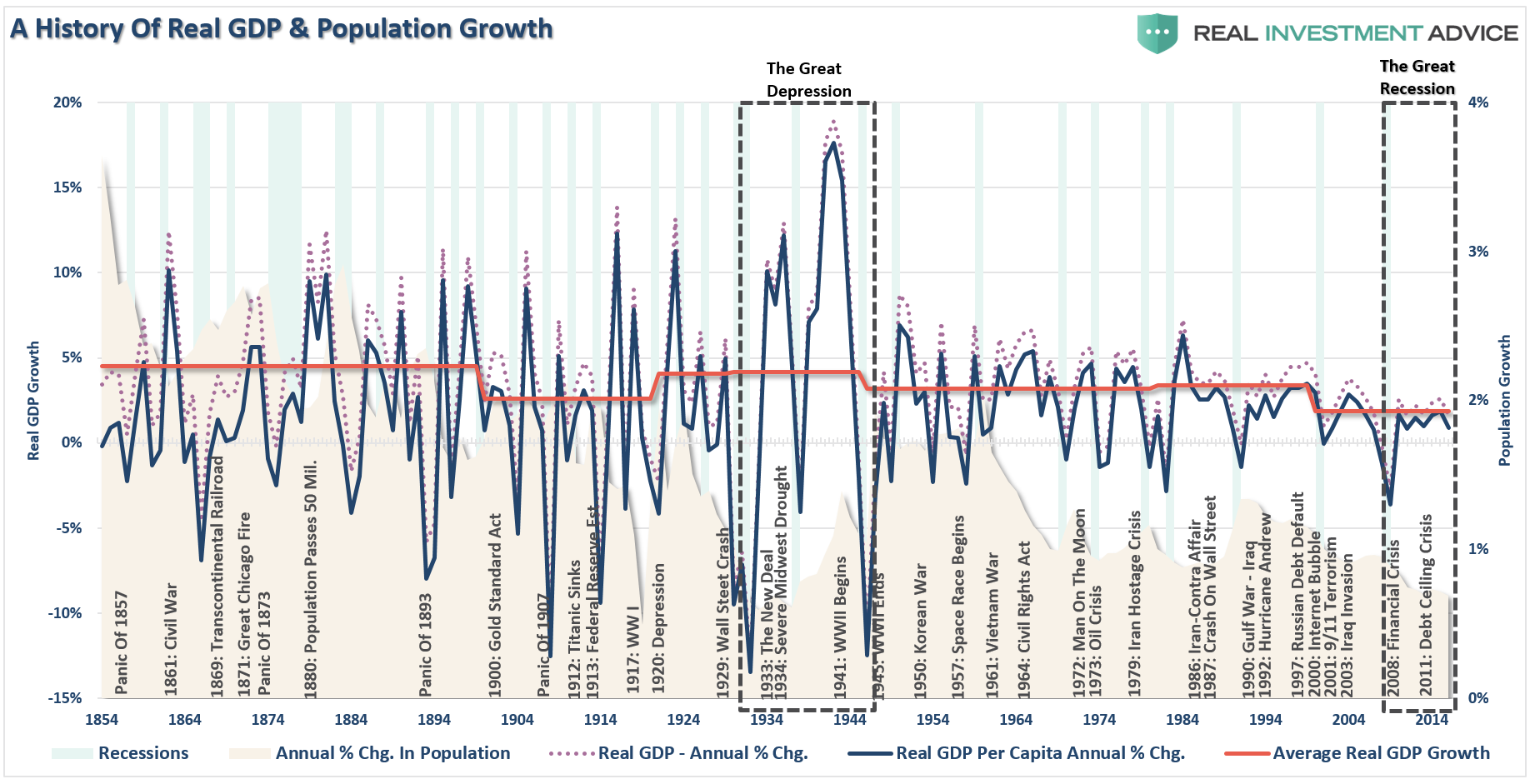

The chart below shows both the long-view of real, inflation-adjusted, annual GDP growth and on a per-capita basis. I have also included the annual growth rates of the U.S. population. I have highlighted significant historical events for some context as well as notating the depression era and the current “Great Recession.” [Data Source: MeasuringWorth.com]

However, there are some interesting differences between the “The Great Depression” and the “Great Recession.” During the depression, the economy experienced extremely strong annual rates of growth reaching peaks of 13% and 18% on an annualized basis as opposed to peaks during the current economic cycle of 2.5% and 2.7%. What plagued the economic system during the depression was the real loss of wealth following the “Crash of 1929” as a rash of banks went bankrupt leaving depositors penniless, unemployment soaring and consumption drained. While the government tried to provide assistance it was too little, too late. The real depression, however, was not a statistical economic event, but rather a real disaster for “Main Street.”

During the current period, real economic growth remains lackluster, real unemployment remains high with millions of individuals simply no longer counted or resorting to part-time work just to make ends meet and roughly 100-million Americans are on some sort of government assistance. The pressure on “Main Street” remains.

One important difference is the rate of population growth which, as opposed to the depression era, has been on a steady and consistent decline since the 1950’s. This decline in population growth and fertility rates will potentially lead to further economic complications as the “baby boomer” generation migrates into retirement and becomes a net drag on financial infrastructure.

I have also noted the average rates of economic growth for various periods throughout history.

- During the “agricultural age,” prior to 1900, the average rate of real economic growth, although very volatile due to weather, disaster and economic events, averaged 4.2% annually.

- As the world entered the 20th century the impact of WWI, the massive inflationary spike that followed which led to a depression, the “Crash of 1929” and the “Great Depression” saw economic growth slip to 2.62% annually.

- From the depths of this turmoil rose an economic powerhouse from 1940-1980 as the U.S. became the epicenter for manufacturing and production worldwide. During this period economic growth surged to 4.51% annually.

- Since 1980, as the U.S. became addicted to credit, leverage, and debt, the economic growth rate has continued to weaken as the U.S. shifted from its production basis to an economy built on finance and services which have lower economic multipliers. Despite the rise of technology, a surging “secular bull market,” and increasing standards of living; the 1980’s and 1990’s saw real economic growth drop to 3.2% annually.

- That rate of growth has continued to decline since the turn of the century as the bursting of the technology bubble and the housing/credit crisis has led to an annual growth rate of just 1.94%.

Despite trillions of dollars of interventions and zero interest rates by the Federal Reserve, combined with numerous bailouts, supports, and assistance from the Federal Government, the economy has yet to gain any real traction particularly on “Main Street.” Are we currently experiencing the second “Great Depression?” That is a question that we can continue to debate currently, however, it will only be answered for certain when future historians judge this period. It will also be that same group of historians who will ultimately determine whether the actions undertaken by the Federal Reserve, and the Government, were ultimately a success or failure.

One thing is for certain. With the lowest rate of annualized economic growth on record, there is a problem currently which is not being adequately recognized. Despite ongoing interventions and hopes for economic recovery, the rate of population growth has now fallen to levels not seen since the early 1930’s. The long term consequences of an aging population, lower incomes and savings rates and a declining rate of population growth is a problem that is likely to continue to hamper the economy going forward. Of course, these are the same problems that currently plague Japan.

The End Of The Bond Bubble

The problem with most of the forecasts for the end of the bond bubble is the assumption that we are only talking about the isolated case of a shifting of asset classes between stocks and bonds.

However, the issue of rising borrowing costs spreads through the entire financial ecosystem like a virus. The rise and fall of stock prices have very little to do with the average American and their participation in the domestic economy. Interest rates, however, are an entirely different matter.

While there is not much downside left for interest rates to fall in the current environment, there is also not a tremendous amount of room for increases. Since interest rates affect “payments,” increases in rates quickly have negative impacts on consumption, housing, and investment.

Will the “bond bull” market eventually come to an end? Yes, eventually. However, the catalysts needed to create the type of economic growth required to drive interest rates substantially higher, as we saw previous to 1980, are simply not available today. This will likely be the case for many years to come as the Fed, and the administration, come to the inevitable conclusion that we are now caught in a “liquidity trap” along with the bulk of developed countries.

I am long bonds and continue to buy more whenever someone claims the “Great Bond Bull Market Is Dead.”

Lance Roberts

Lance Roberts is a Chief Portfolio Strategist/Economist for Clarity Financial. He is also the host of “The Lance Roberts Show” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter and Linked-In

Copyright © Clarity Financial