by Jeffrey Saut, Chief Investment Strategist, Raymond James

The absolute price of a stock is unimportant. It is the direction of price movement which counts.

During major sustained advances in stock prices, which usually occupy from five to seven years of each decade, the investor can complacently hold a list of stocks which are currently unpredictable. He doesn’t worry about the top because he knows he is never going to sell at the top. He knows that the chances are overwhelming in favor of the assumption that he will get far better prices by waiting until after the top has passed and a probable reversal in trend can be identified than he will ever get by attempting to anticipate the top, and get out on the nose.

In my own experience the largest profits we have ever taken have come from stocks purchased while they were making a new high in a market which was also momentarily expecting the top. As I have already pointed out the absolute price of a stock is unimportant. It is the direction of the price movement that counts. It is always probable, but never certain, that the direction of the price movement will continue. Soon after it reverses is time enough to sell. You should sell when you wish you had sold sooner, never when you think the top has arrived. That way you will never get the very best price – by hindsight your individual transaction will never look daring. But some of your profits will be large; and your losses should be quite small. That is all that is necessary for a satisfactory, enriching investment performance.

. . . “Stock Market Profits Without Forecasting,” by Edgar S. Genstein

As many of y’all know I have been in New York City seeing accounts and marinating some olives with folks at the Friends of Fermentation Christmas party. As we approach the end of the year I find many of my friends who manage money quite distraught since they have not been able to keep up with the “Joneses”; that would be the Dow Jones. Indeed, not only do they currently have performance risk, but bonus risk and ultimately job risk. Accordingly, Andrew and I wanted to leave you with this end of the year aforementioned quote to ponder. These are two of the most important paragraphs we have ever read. Do not read them just once. Go off to a quiet spot that invites contemplation and read them several times. Then reflect on all of the mistakes you have made in trading and investing. Bells will ring, and curses will be uttered, if you are truly honest with yourself. Our advice is to keep this quote handy, read it over and over, and study it every time you get ready to make an important buy or sell decision; especially if your emotions reign.

With these thoughts in mind, we ask you to think about recent history. Going into the Brexit vote many pros raised cash expecting stock market mayhem if the U.K. voted to leave the EU. If you will recall the odds makers thought it was going to be a “stay in” vote. Oops, because Brexit was a non-event as we chronicled in these missives before the vote. Fast forward to the U.S. presidential election, which everyone thought would be won by Hillary Clinton. Hereto, if you raised cash you felt good for about one hour as the markets “dipped” the morning after the election, but that was the only “dip” you got, and we were bullish. In point of fact, we actually made the case it really didn’t matter who won; the stock market was in a position to rally. We have maintained that bullish bias since our models suggest the indices should grind higher into late-January/early-February. Interestingly, we were at a Blackrock CIO meeting last week and had lunch with Larry Fink (Blackrock’s CEO). He said he has never seen a honeymoon period like the post-election elation the equity markets are currently experiencing, but it is likely to last into the January 20 inauguration and after that reality might just show up. Since our models tend to agree with that view, it certainly makes sense to us.

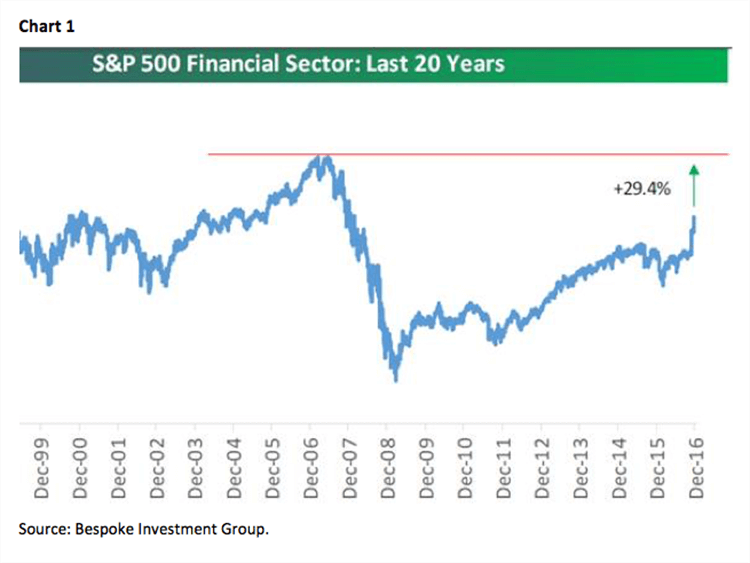

So, what is the underinvested investor to do? Well, while it is true the S&P Financials have had a tremendous rally, they are still some 30% below their price high of 2006 – 2007 (Chart 1). Ditto the S&P 500 Energy sector, which resides ~32% below its 2013 price high (Chart 2). We particularly like many of the midstream/downstream master limited partnership (MLP) stocks that our fundamental energy analysts have tagged with a favorable rating. We believe both of these sectors have upside legs from here as the equity markets grind higher into our late-January/early-February “timing point,” which should mark some kind of temporary trading top, yet still within the construct of a secular bull market that has years left to run!

Another class of assets we find attractive, given their yield characteristics, would be the convertible issues (both preferreds and convertible bonds/notes). In fact, one of the better asset managers of converts I am meeting with in NYC this week is Advent Capital Management. In its recent report titled “Trump Era: Why Investing in Convertibles Makes Sense” with the tagline “Convertibles have historically performed well in a rising interest rate environment,” Advent concludes:

Although often overlooked, convertibles are a separate asset class that have a long track record of delivering equity-like returns with less risk and lower correlation to equity and fixed income securities. Consequently, convertibles add value when included in either a bond or stock portfolio. As the Trump Era unfolds, convertibles offer a unique solution for improving the diversification and positive asymmetry of a portfolio.

Raymond James’ convertible research department has compiled a list of converts that play to stocks our fundamental analysts have favorable ratings on, and we suggest perusing said list and/or contacting the convert department for investment ideas.

The call for this week: Indeed, “The absolute price of a stock is unimportant. It is the direction of price movement which counts.” To be sure, our models telegraphed the stock market’s upside direction since before the election; a direction we continue to favor into late-January/early-February. Could there be some pauses/pullback attempts along the way? You bet there could, but we think they will not be all that impactful. In fact, our sense is there will be some kind of short-term trading peak this week, which will not get very far on the downside. That view is being telegraphed by the D-J Transports (down last week) and the Treasury bond market (higher rates). Of course that will produce cries from many pundits arguing against the upside price path, with “bear boos” of bubbles, overpriced stocks, euphoria, market crashes, etc. You should put earmuffs on to such “noise.” Verily, “The absolute price of a stock is unimportant. It is the direction of price movement which counts.”

P.S. - I am in New York City all of this week . . .

Copyright © Raymond James