When US Rates Rise, Stand By Your Credit - Context

by Fixed Income AllianceBernstein

November 15, 2016

The Federal Reserve is likely to raise interest rates in December, and Donald Trump’s US election win has markets worried that it won’t stop there. But credit assets can still help globally minded investors to pilot their bond portfolios through periods of turbulence.

Let’s be clear: there will be some turbulence. Global bond markets have already come under pressure, and longer-term Treasury yields have risen sharply over the past week. A lot of this has to do with Trump’s pledge to ramp up infrastructure spending. With Republicans in control of Congress, investors are betting that expansionary fiscal policy will feed inflation and force the Fed to hike rates more rapidly next year.

And the political risk and uncertainty that have whipsawed markets this year won’t end in 2016. Brexit and the US presidential election are behind us, but elections in France and Germany top a busy calendar in the year ahead. Those results may also have implications for monetary and fiscal policy.

HIGHER YIELDS, HIGHER INCOME

In the US, a Trump administration that manages to open the fiscal floodgates probably would result in more action from the Fed in 2017. But increased spending and higher interest rates will likely come hand in hand with stronger economic growth. That’s not an especially bad scenario for corporate balance sheets or corporate bonds, particularly those issued by investment-grade companies with strong balance sheets.

Credit spreads—the extra yield corporates offer over comparable government bonds—may widen initially. But the resulting rise in yields should attract more buyers, which will eventually cause spreads to tighten. Meanwhile, higher interest rates ultimately work to investors’ advantage. When bonds mature, investors can reinvest the principal in higher-yielding securities.

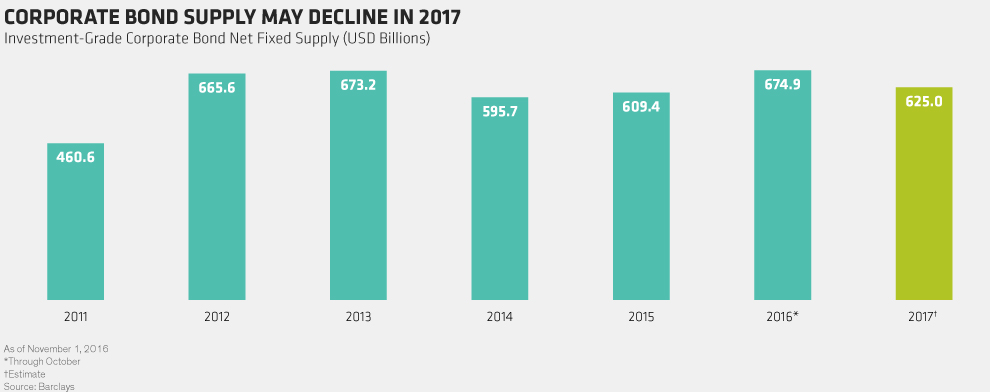

Other potential Trump policies may benefit bonds. For instance, Trump’s call for a repatriation tax holiday for corporations with cash parked oversees could limit the need for companies to borrow. If that reduces new supply in 2017, existing bondholders should benefit (Display 1).

BEYOND CORPORATE BONDS

Even so, those investors who have the flexibility to invest globally across sectors and industries will find that there are attractive credit opportunities beyond corporates.

Consider, for example, floating-rate credit risk transfer securities (CRTs), a type of residential mortgage bond issued by the US federal housing agencies. These securities’ variable coupons mean they may hold up better in a rising-rate environment than some corporate bonds do.

CRT yields are roughly in line with those of high-yield bonds. But when it comes to credit fundamentals, they couldn’t be more different. CRTs are supported by a recovering US real estate market and strong borrower credit metrics; average borrower credit scores and debt-to-income ratios are at or near their best levels in almost a decade.

It’s important to remember that the path to higher official rates in the US and higher bond yields globally is still likely to be a long and winding one. Uncertainties about the global economy abound, suggesting that the Fed will proceed as cautiously as possible.

The keys to success in today’s low-yield environment have been to maintain diversified sources of income and have the flexibility to go anywhere around the globe to tap them. That isn’t going to change soon, no matter what the Fed does in December. Investors who turn their backs on credit will only make it harder for themselves to meet their income needs.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

Copyright © AllianceBernstein