by Eric Bush, CFA, Gavekal Capital

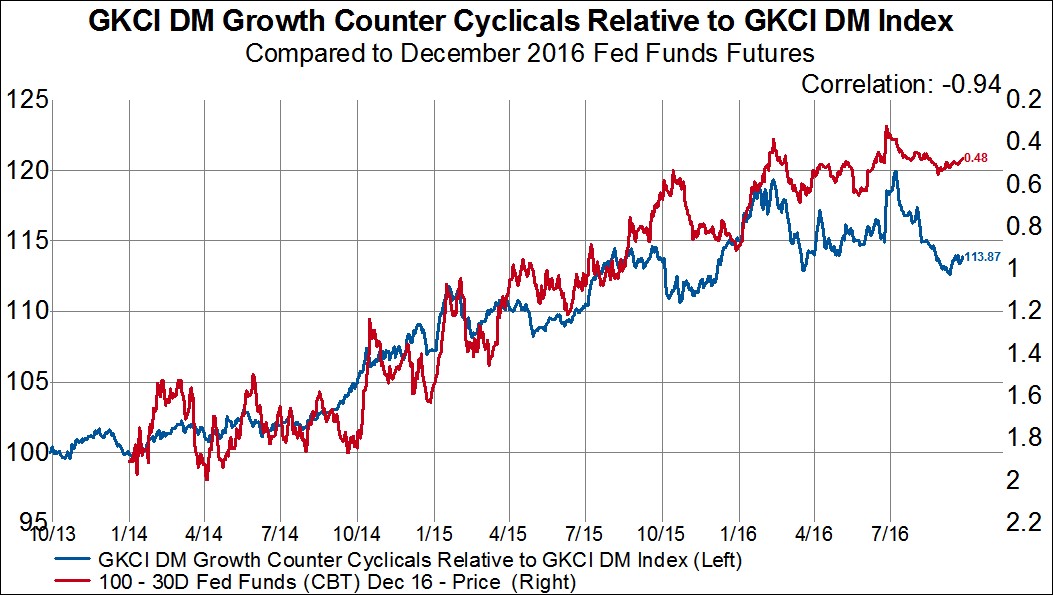

It has been less than a week since the latest FOMC meeting and the market is already losing conviction that the Fed will raise rates in 2016. According to Bloomberg’s WIRP function, the probability of a hike in December has already fallen to 49% from 58% a week ago and from 65% a month ago. Another way to visualize this is to look at the price of Fed Fund Futures that expire in December. The current price is suggesting a Fed Funds Rate of only 48 bps (i.e. within the current 25-50 bps target). At the end of August, the market was suggesting that the Fed Funds rate would be at 55 bps and before Brexit the market was pricing in a 63 bps Fed Funds Rate in December. If the Fed does decide to hold steady in December (and no one actually believes the Fed would hike a week before the election, do they? The market certainly doesn’t as the current probability of a hike on 11/2 is just 18%), then this will have some serious equity sector repercussions. Mainly, investors will want to remain in the sectors that have been working over the past three years, consumer staples and health (i.e. growth counter-cyclicals), even though these sectors have underperformed since July. Additionally, investors will want to stay away from late cyclicals (energy, materials, and industrials) as these stocks have underperformed in lock-step with expectations for the Fed Funds Rate over the past three years. Finally, consumer discretionary stocks could be back in favor for the first time since late 2015. This sector has already started to perform better post-Brexit and it benefited from more dovish interest rate expectations from October 2014-October 2015.

Copyright © Gavekal Capital