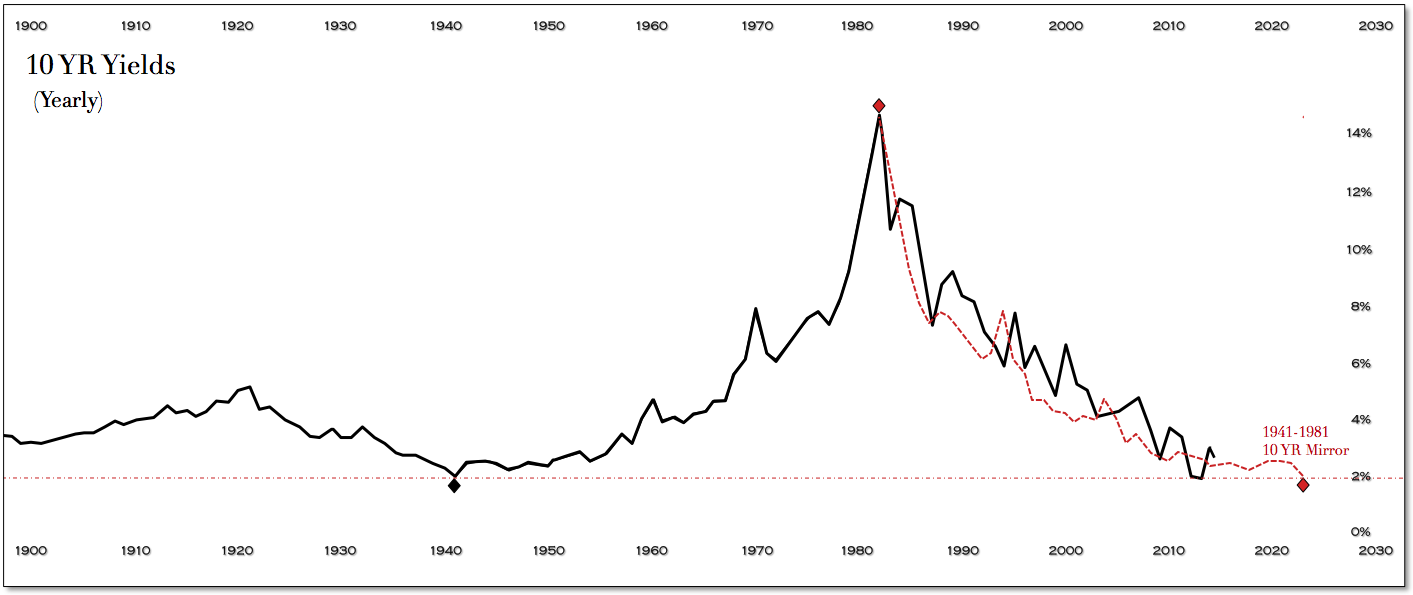

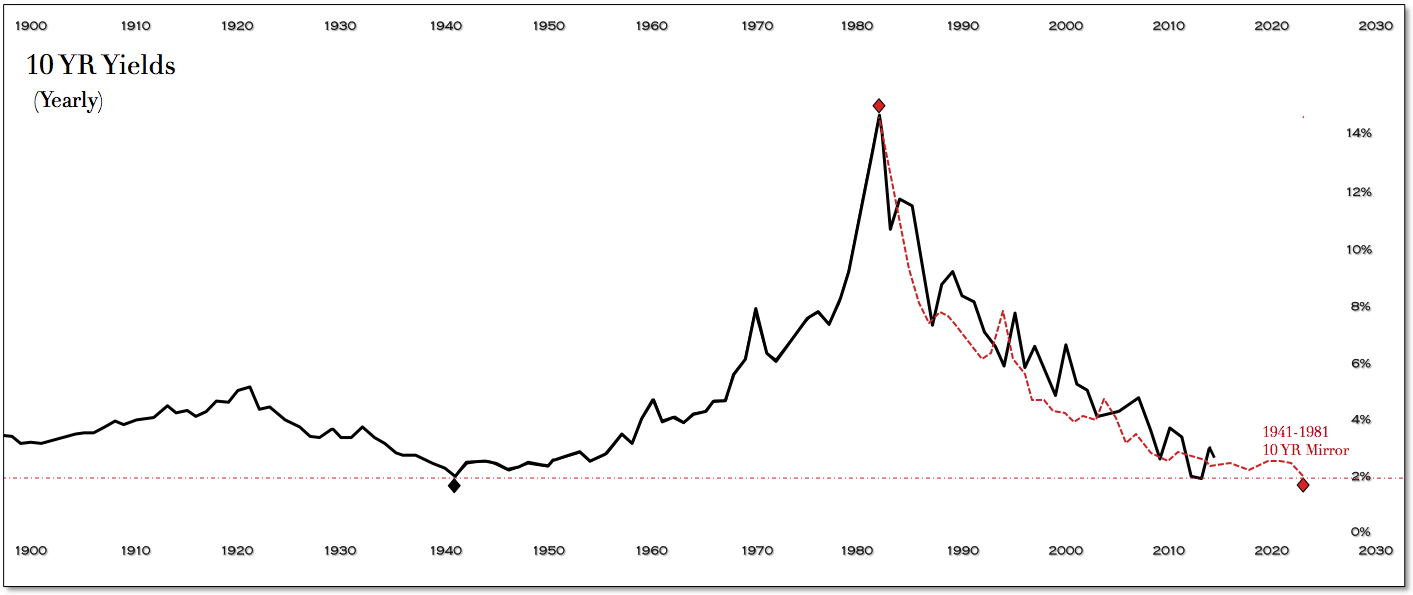

On both sides of the spectrum, whether through bailouts, interventions or rate tightenings - the Fed has looked to shake the tree from time to time when the markets are deemed too complacent, accommodative or risk adverse. Coincidentally - or not, these occasions over the last thirty years have been when yields have fallen back proximate to the mirror of the cycle. Has it been beneficial? We'll save that nuanced argument for the historians, but do believe it demonstrates quite clearly the nature versus nurture aspect of the Treasury market. The Fed may find efficacy with the cattle prod at times, but the herd of the largest security market in the world will still closely follow the inherent migration pattern - one that many analysis, pundits and traders have attempted to call an audible from over the years.