Via Citi FX Technicals,

Gold looks to have found a base...

Following the multi-year surge in Gold the recent fall took us 14% below the 55 month moving average. That is exactly what happened in 1976 during Gold’s correction after a multi-year move higher.

Once that moving average was regained on a monthly close basis the uptrend re-established itself and Gold rallied for the next 3 years. (included in that period was the “supply shock” driven move higher in crude)

The rally in the Equity market after the 1973-1974 “crash” peaked 4 weeks after that corrective low was placed in Gold.

SO FAR the trend peak in the stock market (DJIA and S&P) has taken place 5 weeks after the corrective low was posted in Gold.

After that peak in late 1976 the Equity market entered into an 18 month long 27% correction.

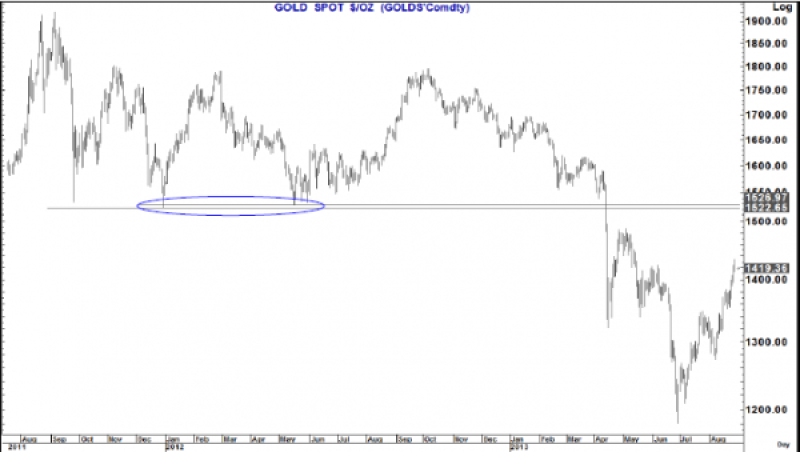

Gold weekly chart- Prior support now good resistance

The pivotal breakdown level on Gold was at $1,522-1,527 and should now be pivotal resistance in this rally.

Gold broke below this level during the week of 08 April 2013. It is unlikely that it is a coincidence that that precipitous fall took place in the same week that the S&P 500 regained its 2007 highs.

So, do not be surprised that IF , as we expect Gold heads higher to re-test this $1,522-1,527 area in the weeks/months ahead that the S&P is re-testing the break out point of 1,576 again...

........

We still retain a view that we can see a “low to high” percentage move in this bull market similar to what we saw in the bull market of 1970-1980.

If we extract the final leg of that move in December 1979-Jan 1980 which was totally driven by the USSR invasion of Afghanistan almost doubling the price of Gold over 5 weeks then we end up with a target of around $3,500 over the next 3 years or so.

The charts below are compelling in that respect, but before we look at them we will indulge in some pontification.

We are at a point of change of leadership at the Fed with two primary candidates being mentioned. (Janet Yellen and Larry Summers). We are NOT going to opine on who it should be but rather make observations about why we think it is going to be one rather than the other.

When President Obama spoke on the Charlie Rose show about Chairman Bernanke’s tenure it was obvious that it was coming to an end. The question to ask was why? If we (He) was happy with the path being followed, why not just ask Ben to stay on. (We also firmly believed that if asked Ben would have stayed). It is therefore not a stretch to believe that the President was less than convinced about the “efficacy” of QE. Reasons for this could well have been (supposition on our part):

- Sub-par economic growth of 1.7-2.0% and very low nominal growth given the low level of inflation

- A falling unemployment rate... yes (7.6% at the time)... but not of the magnitude and quality that we associate with an economic recovery (Lowest participation rate since 1979 flattering the rate; underemployment at the time (U6) at 14.3%; the majority of jobs being created are part time jobs with the 55-69 year old age group the primary demographic beneficiary)

- Housing recovering but very gradually compared to previous cycles and a view in a lot of circles that a significant chunk of demand was private equity buying distressed assets

- An Equity market rallying about 140%+ (The rich get richer, the gap gets wider)

- Banks et all benefiting from never ending cheap money and being encouraged to misallocate capital in financial assets that are being made almost risk free by the Bernanke, ever expanding, “QE to infinity” put

- Provides a benefit to the marginal borrower while “crucifying” the whole savings base

- Continued QE created a back stop to allow congress to push harder on budget cut and debt limit negotiations (Play hardball)

Let us say that some or all of that was true. Would the President really want to appoint somebody who to a very large extent would be likely to follow the same “prescription” (Yellen)? Why? If you wanted to continue that policy then would you not do that with the “guy” who engineered it and took us through the crisis (Bernanke)? Or do you feel that your financial “Churchill”…the man to fight the war is no longer the direction you want to go. We firmly believe that “change is afoot” and that change goes by the name of Larry Summers.

Why is that important?

Nothing suggests that Summers is a “hawk”. However, there are suggestions that he questions the “mix” of policy. It looks like he would be much more likely to try and “draw a line” under this unorthodox monetary policy experiment by bringing QE to a conclusion. This will not be a “shock and awe” change but rather a gradual wind down of purchases and eventually the Fed balance sheet through the maturity schedule.(We believe this could happen irrespective of the economic backdrop)

What would this mean?

If, as we believe, we have some potentially significant headwinds coming in markets and the economy then this is going to “throw the ball” right back into the “arms of Congress”. (Is Larry Summers the 21st century’s Paul Volcker?) If the independent Fed is no longer prepared to expand monetary policy “ad infinitum” to support the economy and the economy is slowing what will Congress have no choice but to do???? Stimulate again through fiscal policy. This will mean deficits once again widening and the debt limit rising. It will be a shift back not to tight but to “less loose” monetary policy and looser fiscal policy (This will also likely benefit the USD)

That is why the chart below remains one of our favourites.

Gold and the US Debt Limit

It is no coincidence in our mind that these two have expanded together over the last 10-12 years

As we continue to spend more than we earn and shift that liability to the next generation Gold has shown itself to be a very effective hedge against that policy. The recent “squeeze in Gold” has sent it significant below this “stairway to hell” chart (Debt limit) which has continued higher. As we said earlier, we do not believe that this fall in Gold will be sustainable and expect new highs in the trend eventually. As we also said above , we have retained a long term target of about $3500 for some time on this Gold price based on a comparison of this period and that seen in the 1970’s

As we headed towards the last Presidential election there was a considered view in the markets that by the end of President Obama’s 2nd term the debt limit could be as high as $22 trillion. Then we got the sequester, a more rosy economic outlook, tapering talk and all this has been forgotten. For how long?

The market dynamics above combined with the change of leadership at the Fed may well be “resurrecting that thought”. If so our 2nd favourite Gold chart comes into play.

Gold and the US debt limit (Again): So what would a debt limit of $22 trillion over the next 2-3 years suggest for the Gold price?

How about $3,500

We firmly believe that the Gold correction has “run its course” and that much higher levels will be seen in the years ahead.

Copyright © Citi FX Technicals