by Lance Roberts, RIA

Risk isn’t about how much money you’ll make. It’s about how much you can lose, and whether the loss is one you can come back from. That distinction is the entire basis for the 15-investing rules framework we use to manage real money for real families, and it’s the reason most investors lose the long game even when the market is going up.

Key Takeaways

- The single biggest predictor of long-term investing success isn’t intelligence or stock picking. It’s discipline under emotional pressure.

- Every investor faces two risks at once. You can defend against losing money, or you can defend against missing an opportunity. You can’t fully defend against both.

- The 15 investing rules below are the control boundaries that govern how we manage capital. They aren’t predictions. They’re guardrails.

- The bull trend that started in 2009 is still alive in 2026, but the cost of keeping it alive has climbed every cycle. Rules matter more, not less, when monetary policy is doing the heavy lifting.

- The goal is not to ever lose money. The goal is to never lose so much that you can’t recover.

After three decades of watching market cycles play out from both sides of the trade, I’ve come to one stubborn conclusion. The investors who win the long game aren’t the smartest in the room. They’re the ones who follow a process when their gut is screaming at them to do the opposite. The 15 investing rules below are the process we follow at RIA Advisors. They’re also the reason we sometimes look “wrong” in the short run and why our clients keep their wealth through full market cycles.

The Two Risks Every Investor Faces

Howard Marks of Oaktree Capital wrote a memo years ago that I keep returning to. Marks made a simple observation that almost no retail investor internalizes. There aren’t one but two risks in investing, and they pull in opposite directions.

The first risk is the obvious one. You can lose money. The second risk is the one no one talks about at cocktail parties. You can miss an opportunity. You can defend yourself against either of those risks, but you can’t fully defend against both at the same time. So every portfolio decision, whether you realize it or not, is a positioning choice on a spectrum between those two failure modes.

Marks framed it as the angel and the devil sitting on each shoulder. The angel whispers, “Be prudent.” The devil whispers, “You’ll get rich.” In bull markets, the devil tends to win, which is how bubbles form. That’s how Bernie Madoff raised the money he raised, and why every cycle ends the same way: retail investors are maximally exposed at the top and maximally afraid at the bottom.

However, here’s where it gets interesting. The “miss out” risk is just as real as the “lose money” risk, and ignoring it produces its own kind of damage. The investor who sat in cash from 2009 to 2024 didn’t lose money in nominal terms. They lost most of a working career’s worth of compounding. Corrections aren’t the same thing as bear markets, and treating every wobble as the end of the world is its own form of risk.

Of course, the inverse is the larger trap. Most people don’t sit in cash. Most people chase. They buy what just went up, and they sell what just went down, because that’s what emotion tells them to do.

Why Discipline Beats Intelligence Every Time

Marks calls the antidote “unemotionalism.” It’s an awkward word, but it captures the idea. The great investors he’s worked with for forty-five years share one trait, and it isn’t IQ. It’s the ability to not feel the pull of the crowd.

If you’re emotional, you’ll buy at the top when everyone is euphoric. However, you will also sell at the bottom when everyone is panicked. Therefore, it is inevitable that you will do the wrong thing at extremes, which is precisely where the biggest money is made and lost. Marks put it bluntly. If you can’t be unemotional, you shouldn’t be managing your own money. Period.

That’s a hard pill to swallow. But the data backs it up. Morningstar’s annual “Mind the Gap” study has tracked the difference between fund returns and the returns actual investors earn in those same funds for years. The gap is consistently negative. Investors underperform the funds they own because they buy in after the run and sell after the drawdown. The fund didn’t fail them. Their behavior did.

That gap is what behavioral finance researchers call the “behavior gap.” It isn’t a tax. It isn’t a fee. It’s the cost of being human in a market that punishes humanness. The 15 investing rules below exist for exactly one reason. They take the human out of the loop at the moments when the human is most likely to cost you money.

Am I bearish? I’m tagged that way constantly. The honest answer is I’m neither bullish nor bearish. I look at economic, fundamental, and price data for what they are, not for what I want them to be. Sometimes, the data says lean in. Sometimes it says “back off.” The rules tell me when, and they don’t ask my permission.

Do I make mistakes? Absolutely. Do emotions seep into my decisions? Of course they do. I’m a human running a portfolio, not a machine. But the rules act as a circuit breaker. They keep small errors from becoming career-ending ones.

The 15 Investing Rules That Anchor Our Process

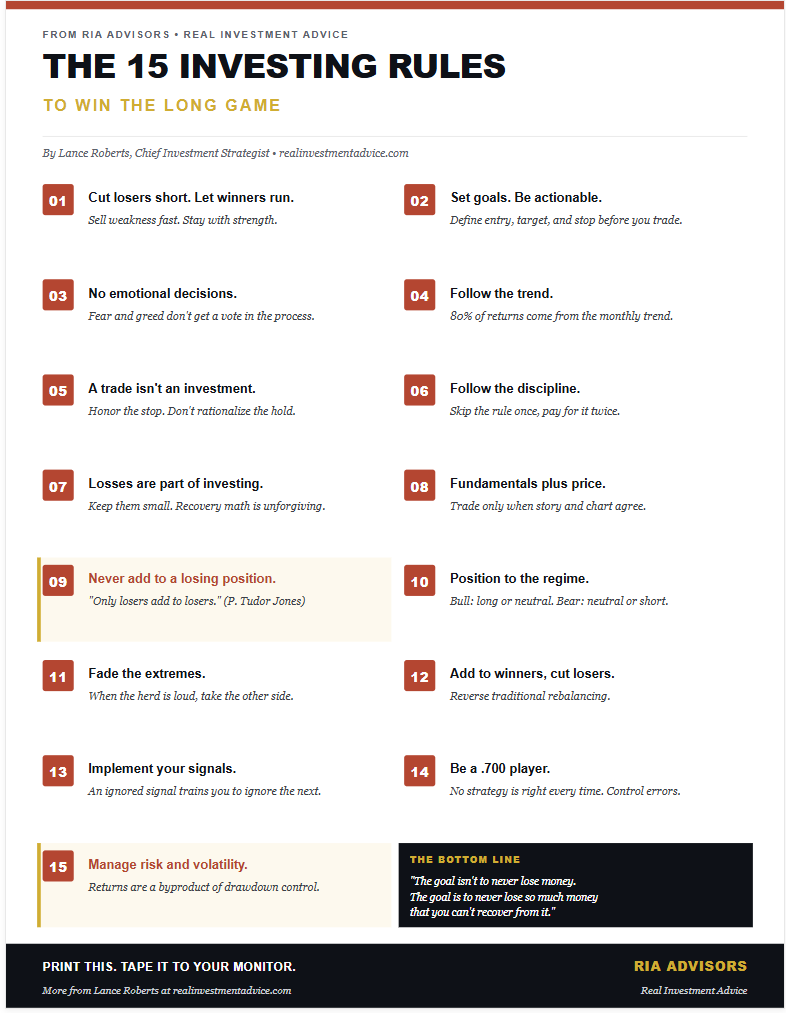

What follows are the rules. (I have included a printable graphic of these 15 investing rules at the end of the article.)They’re the boundaries inside which our portfolio decisions are made. Each one is short. Each one is testable. And each one exists because we’ve seen, in real money on real client accounts, what happens when it gets broken.

1. Cut losers short and let winners run.

Be a scale-up buyer, not a scale-down one. The biggest accounts I’ve ever seen blow up did so because someone fell in love with a losing position and kept adding. Winners get more capital. Losers get cut. That’s the rule, even when, especially when, the gut is screaming at you to do the opposite.

2. Set goals and be actionable.

Every trade needs a defined entry, a defined target, and a defined stop before the order is placed. Without specific goals, decisions become arbitrary. Arbitrary decisions are how portfolios drift, and drift is how losses accumulate quietly.

3. Emotionally driven decisions void the investment process.

If you change a position because you saw something on cable news, you’ve already lost. Emotion buys high and sells low. The whole point of having a process is to keep fear and greed from getting a vote.

4. Follow the trend.

Roughly 80% of portfolio performance is determined by the long-term, monthly trend. A rising tide lifts all boats. The opposite is also true. In a bear trend, the best stocks still get crushed. Trying to outsmart the trend is the most expensive ego trip in investing.

5. Never let a trading opportunity turn into a long-term investment.

Refer to rule one. Every initial purchase is a trade until the thesis is proved correct. The single most common rationalization in investing is “I’ll just hold it until it comes back.” Sometimes it does. Often it doesn’t. Plan for the second case.

6. An investment discipline does not work if it is not followed.

This sounds tautological. It isn’t. The discipline works because it’s followed every time, not most of the time. The one trade you break the rule on is statistically the one that costs you the most.

7. Losing money is part of the investment process.

If you can’t accept losses, you can’t invest. Markets don’t owe you a positive print every day. The job isn’t to avoid every loss. The job is to keep losses small enough that the wins more than cover them.

8. The odds improve when fundamentals are confirmed by price action.

A great company at a bad price is a bad trade. A bad company breaking out is a head fake. When the fundamental story and the chart agree, the odds tilt in your favor. When they disagree, sit on your hands. This applies in both bull and bear markets.

9. Never, under any circumstances, add to a losing position.

Paul Tudor Jones said it best. “Only losers add to losers.” If you bought at a higher price and you’re underwater, the trade is wrong. Adding more capital to a wrong trade doubles the wrong. It doesn’t fix it.

10. Markets are either bullish or bearish. Position accordingly.

In a bull market, be long or neutral. In a bear market, be neutral or short. Trying to be a hero short in a bull market is the fastest way to underperform. Trying to “buy the dip” in a real bear market is the fastest way to blow up. Identify the regime first. Position second.

11. At extremes, do the opposite of the herd.

When the cover of every magazine is bullish, take some off the table. When the same magazines are calling for the end of capitalism, start scaling in. The herd is right in the middle of moves. The herd is wrong at the ends. That’s where the asymmetry lives.

12. Do more of what works and less of what doesn’t.

Traditional rebalancing takes money from your winners and adds it to your losers. We rebalance the other way. We reduce losers and add to winners. The market is telling you what’s working. Listen to it.

13. Buy and sell signals are only useful if implemented.

A signal you ignore is worse than no signal at all, because it trains you to ignore the next one. If your system says sell, sell. If your system says buy, buy. The system isn’t smarter than you. It’s calmer than you. That’s the entire edge.

14. Strive to be a .700 “at bat” player.

No strategy works 100% of the time. The greatest hitters in baseball get on base about four times out of ten. A .700 hitter in investing is borderline mythical. Be consistent, control errors, and capitalize on opportunities when they arise. Win more than you lose, lose small when you lose, and the compounding takes care of itself.

15. Manage risk and volatility.

Control the variables that lead to mistakes, and returns become a byproduct. The investor who manages drawdown wins the compounding war, even with lower headline returns. Math is unforgiving here. A 50% loss requires a 100% gain to break even. A 20% loss requires only 25%. Small losses are recoverable. Large ones are career-defining.

The Bull Trend, Updated For 2026

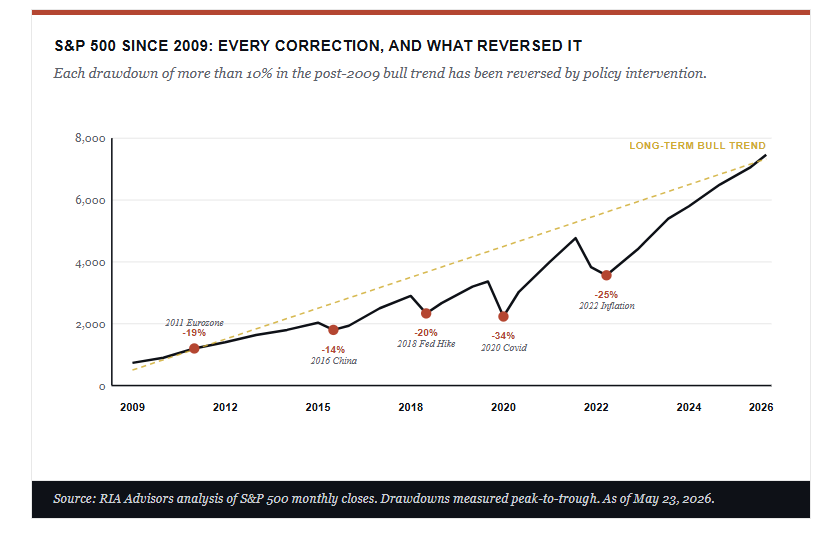

The long-term bullish trend that began in March 2009 remains intact as I write this in late May 2026. That’s a remarkable run by any historical standard. The chart below shows that trend, with every meaningful correction along the way and the catalyst that ended it.

Notice in the chart above what each correction has in common. In 2011, the Eurozone scare prompted the second leg of the Fed’s quantitative easing program. The 2016 China-and-oil panic was reversed by a coordinated central bank response. By late 2018, the sell-off ended when Chairman Powell pivoted to a more dovish stance. The 2020 Covid crash reversed inside a month, on the largest monetary and fiscal stimulus the world had ever seen. And in 2022, the inflation drawdown reversed once the market priced in that the Fed was nearly done hiking.

Each cycle, the policy response has gotten larger. Each cycle, the recovery has come faster. And each cycle, the structural debt and valuation overhang have grown a little heavier. The bottom line is this. The bull trend is still alive, but the dependence on monetary intervention to keep it alive is now obvious to anyone paying attention.

So what does this mean for investors today? Until that long-term trend is violated and fails to recover, portfolios should remain long or neutral. Trying to short the trend has been a losing strategy for the better part of seventeen years. But the moment the trend breaks and doesn’t reclaim, the rules say flip the posture. Neutral or short. No exceptions. That’s the value of having rules. They don’t ask you to predict the top. They tell you what to do when the top has already happened.

Weekly Market Insight

Get the Bull Bear Report in your inbox.

Lance Roberts’ weekly read on markets, positioning, and risk. Free. No fluff. Lands in your inbox every Saturday morning.

Putting These Investing Rules Into Practice

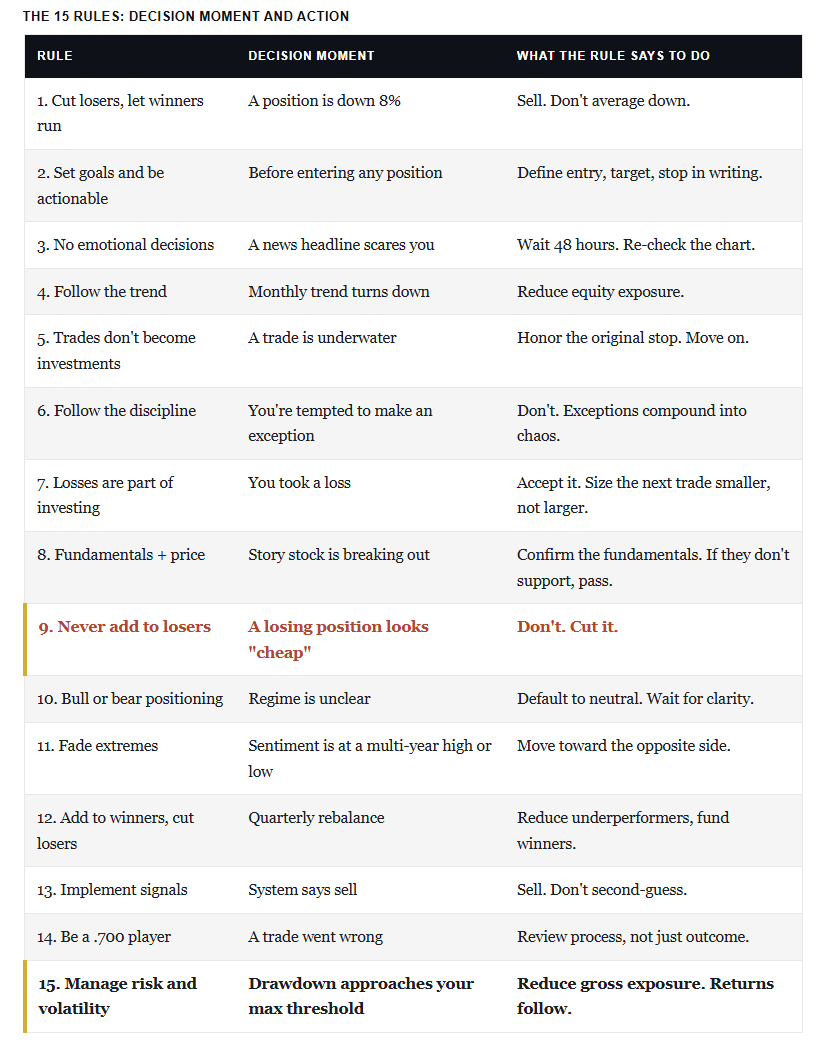

The rules are easier to write than they are to follow. The table below maps each rule to the specific decision moment at which investors most often violate it and to the concrete portfolio action the rule prescribes instead. Print it. Tape it to the side of your monitor. Read it the next time you feel an emotional pull toward a trade.

Two things will jump out to anyone who studies the table for more than a minute. First, the decision moments are predictable. They happen every single market cycle. Second, almost every “right” action is the one that feels worst in the moment. Selling a loser is painful. Sitting in cash while everyone else is making money is excruciating. Cutting back exposure at a top while the tape is still running feels like leaving money on the table. Of course, that’s exactly why the rules work. The rules are doing the hard part for you.

The other piece I want to flag here is that these rules don’t tell you what to buy. That’s intentional. Stock picking is a small part of investing returns over a lifetime. Position sizing, drawdown management, and behavioral discipline are the large parts. We’ve published more on the mechanics of that in our piece on the immutable laws of building wealth, which pairs naturally with the rules here.

Frequently Asked Questions About These Investing Rules

How are these 15 investing rules different from a typical buy-and-hold strategy?

Buy-and-hold assumes you can ride out any drawdown without changing behavior. The math says most investors can’t. Rules like the ones above keep you participating in bull trends and reduce exposure when the trend breaks. The goal is the same as buy-and-hold: to compound capital over decades. But the path is different because it accounts for the fact that real investors don’t sit through a 50% drawdown without selling at the bottom.

Do I need to follow all 15 investing rules, or can I pick the ones I like?

You can pick. But the more you skip, the less the framework protects you. Rules 1, 9, and 15 are the non-negotiable core. Cut losers. Don’t add to losers. Manage total portfolio risk. If you do nothing else, do those three. The other twelve sharpen the framework, but those three keep the wheels on.

How often should I check my portfolio against these rules?

Monthly is plenty for the trend and positioning rules. Weekly is fine for the individual position rules. Daily is too often, and it’s the fastest way to let emotion in. The rules work best when applied at a cadence that gives the data time to be meaningful. Tape watching is not investing.

What’s the biggest mistake investors make with rules like these?

They follow the rules for a while, the rules tell them to do something painful, and they make an exception. The exception works once, so they make another exception. Three exceptions later, they no longer have a process. They have a hobby. The whole value of a rules-based framework is that it doesn’t ask you to be brave at the right moment. It just tells you what to do.

How do these 15 investing rules apply in a market like the one we have in 2026?

The current market is the cleanest possible test case. We’re in year seventeen of a Fed-supported bull trend. Valuations are stretched. Concentration in a handful of AI-related names is historic. Rule 4 says follow the trend, which is still up. Meanwhile, rule 11 says fade extremes, which is starting to flash. And rule 15 says manage volatility, which means trimming gross exposure as the regime gets more fragile. The rules don’t tell you the top is in. They tell you how to be positioned when the top eventually comes.

Where can I learn more about applying these rules to my own portfolio?

The Bull Bear Report applies this framework to live markets every week. The RIA E-Guide Library provides deeper detail on each rule. And if you want a personal conversation about how the rules would apply to your specific portfolio, that’s what we do at RIA Advisors. Details in the closing section.

Free Desk Reference

Below is a one-page version of the rules. Print it, save it, screenshot it, do whatever helps. The whole point of having rules is being able to look at them in the moment your gut is telling you to break them.

Copyright © RIA