by Russ Koesterich, CFA, JD, Portfolio Manager, BlackRock

In this article, Russ Koesterich discusses the potential impact of seasonal weakness, momentum and the effect these factors could have on earnings in 2H2025.

Key Takeaways

- While not guaranteed, historical data implies that summer and early fall are times of seasonal weakness, often resulting in lower returns for stocks. Momentum tends to impact seasonality, with years of negative momentum further exacerbating negative seasonality.

- Along with concerns around seasonality, extended valuations and a volatile start to 2025 have led investors to question whether earnings estimates may be too high. With economic expectations falling, Russ recommends a focus on names with strong analyst revisions and high cash-flow momentum.

While difficult to explain, seasonal trends have defined markets for a very long time. And while it’s also true that trading stocks based solely on the calendar is not a winning strategy, being aware of seasonal biases offers some advantages. This may be particularly true this year. Four factors conspire to suggest caution in the coming months: the calendar, a poor start to the year, valuations and the potential for further cuts to 2025 earnings.

While the effect can be exaggerated, there is hard data behind the adage, “sell in May and go away”. Historically, the summer and early fall months have produced the lowest returns for stocks. Exact timing does shift over time, recently May has not been a bad month, but over the long-term the patterns have generally held.

One factor that seems to impact the magnitude of seasonal weakness is momentum. Since 1987, the S&P 500 summer returns have been driven in part by how the market did during the first four months of the year. In years such as 2024, when the market was higher going into May, the seasonal impact is muted. However, in years when returns are negative going into May, the average return during the next five months was -1.6%, with markets higher barely 50% of the time. In other words, negative momentum exacerbates negative seasonality.

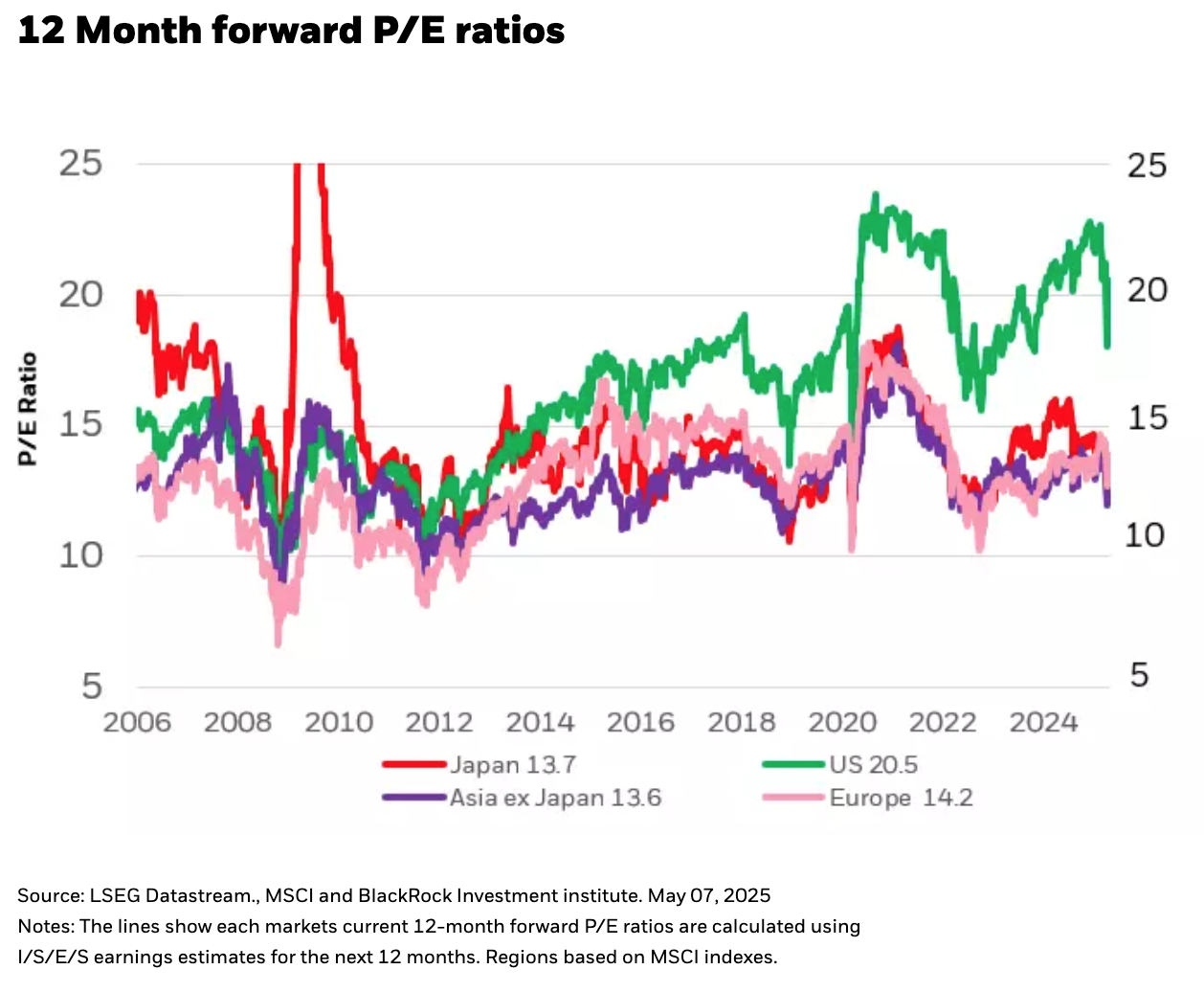

In addition to seasonality and momentum, valuations are once again extended. After dipping in April, the forward-looking P/E for the S&P 500 is back at historically high levels, more than 20x FY1 earnings (see Chart 1). This type of premium was easier to justify last year, when growth was steady and policy uncertainty less of an issue.

To further complicate matters, valuations are based on earnings estimates that may be too high. While estimates for 2025 S&P 500 earnings have ticked lower, they are still aggressive given how fast economic expectations are falling. At the end of February, based on Bloomberg’s consensus estimates, economists expected full year growth of 2.3%; today the number is 1.3%. To the extent we have a softer economy, earnings are more likely to disappoint.

Trade the range and look for resiliency

To be clear, my base case is not a deep recession or prolonged bear market. That said, the S&P 500 has already gained 15% from the May low. Going into the summer, I would recommend two strategies: assume a trading range, maybe 5000 to 5600 on the S&P 500, and emphasize companies with positive analyst revisions and rising cash-flow. We’d also favor companies demonstrating consistent revenue, earnings and margins, i.e. the type of companies that feature in low volatility strategies. The bottom-line: With uncertainty high and earnings vulnerable, it may be prudent to pay a premium for companies able to deliver on results. We also believe that the period we are entering is likely to be conducive to the minimum volatility strategies, particularly if earnings prove somewhat disappointing during a season when, historically speaking, liquidity has been low.

Copyright © BlackRock